Neutral FSN E-commerce Ventures Ltd for the Target Rs 300 by Motilal Oswal Financial Services Ltd

Top-notch execution Beauty steady; Fashion gaining ground

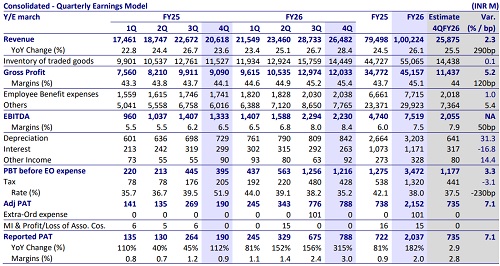

* FSN E-commerce Ventures (NYKAA) reported 4QFY26 net revenue of INR26.48b, rising 28% YoY vs. our estimate of 25.2% YoY growth.

* The BPC vertical’s NSV grew 29% YoY to INR22.69b, supported by acceleration in both growth and profitability vs. our estimate of 24% YoY growth in 4QFY26. Its EBITDA margin came in at 10.3% in 4QFY26 vs. our estimate of 9.7%. * The Fashion vertical’s NSV grew 42% YoY to INR3.97b vs. our estimate of 33% YoY growth in 4QFY26. The vertical reported a contribution margin of 12.1% vs. our estimate of 9.5% in 4QFY26. EBITDA margin for the Fashion business stood at 0.3%.

* Consolidated adj. PAT came in at INR788m (up 315% YoY) vs. our estimate of INR735m. For FY26, its revenue/EBITDA/adj. PAT grew 26.1%/58.7%/191.7% YoY. For 1QFY27, we expect its revenue/EBITDA/adj. PAT to grow 33.6%/78.4%/319.5% YoY. RoE came in at 14.4% in FY26 (vs. 5.6% in FY25).

* We value NYKAA on an SoTP basis with a TP of INR300. We believe much of the growth is now priced in; following the strong share price performance over the past year, near-term risk-reward appears balanced. Reiterate Neutral.

Valuation and changes to our estimates

* We have increased our estimates by ~3.7%/4.8% for FY27/FY28, largely reflecting steady execution across segments. We believe BPC continues to deliver mid-to-high 20% growth with improving margins (~10%+), supported by premiumization and owned brands, though reinvestment remains ongoing. Meanwhile, the Fashion vertical is showing signs of recovery, with growth improving and the business reaching EBITDA breakeven in this quarter. NYKAA is expected to report a PAT margin of 3.4%/4.4% in FY27/28E.

* For the BPC business, we assign a 50x EV/EBITDA multiple, reflecting category leadership, relatively better margins versus horizontal platforms, and improving earnings visibility, implying a per-share value of INR275. For the Fashion business, we use a DCF-based approach, implying a per-share value of INR27. Adjusting for net debt, we arrive at our TP of INR300.

* We believe much of the growth is now reflected in valuations, and following the strong share price performance over the past year, the near-term risk-reward appears balanced. We reiterate our Neutral rating on the stock.

Valuation and view

* We have increased our estimates by ~3.7%/4.8% for FY27/FY28, largely reflecting steady execution across segments. We believe BPC continues to deliver mid-to-high 20% growth with improving margins (~10%+), supported by premiumization and owned brands, though reinvestment remains ongoing. Meanwhile, Fashion is showing signs of recovery, with growth improving and the business reaching EBITDA breakeven in this quarter. NYKAA should report a PAT margin of 3.4%/4.4% in FY27/28E.

* For the BPC business, we assign a 50x EV/EBITDA multiple, reflecting category leadership, relatively better margins versus horizontal platforms, and improving earnings visibility, implying a per-share value of INR275. For the Fashion business, we use a DCF-based approach, implying a per-share value of INR27. Adjusting for net debt, we arrive at our TP of INR300.

* We believe much of growth is now reflected in valuations, and following the strong share price performance over the past year, we believe the near-term risk-reward appears balanced. We reiterate our Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412