Neutral Bosch Ltd for the Target Rs 37,499 by Motilal Oswal Financial Services Ltd

A steady quarter Announces JV with the TSF Group for e-enabled air systems in CVs

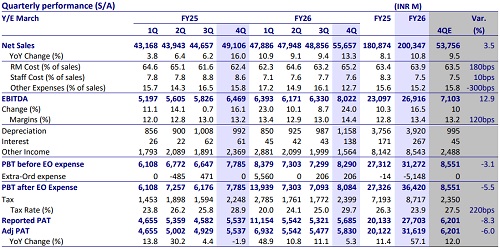

* Bosch (BOS)’s 4QFY26 PAT wasINR5.7b, below our estimate of INR6.2b, despite the EBITDA margin exceeding our estimates. This beat was fueled by lower other expenses. Earnings missed our estimates due to lower-thanexpected other income and higher depreciation.

* Management provided a cautious outlook across all auto segments for 2026, given the ongoing geopolitical uncertainty. Further, while BOS continues to work toward localization of new technologies, given the long gestation of projects, its margin remains under pressure with no visibility of material improvement in the near term. We project BOS to clock a 22%/27%/14% CAGR in revenue/EBITDA/PAT over FY26-28. The stock at 39.3x/33.7x FY27E/FY28E appears fairly valued. We reiterate our Neutral rating with a TP of INR37,499 (based on ~36x FY28E EPS)

Margins beat our expectations, while PAT misses

* Net revenue in 4QFY26 came broadly in line, growing ~13.3% YoY to INR55.7b (est. ~INR54b), led by strong performance in the automotive segment, particularly in Power Solutions and 2Ws.

* The mobility business grew 23.3% YoY, driven by 27.4% growth in Power Solutions and a strong 63.4% YoY growth in the 2W segment. The Consumer Goods segment underperformed and grew 14.3% YoY.

* Gross margin contracted ~280bp YoY (down 200bp QoQ) to 34.8%, below our estimate of 36.5%.

* EBITDA margin came in at 14.4% (+80bp YoY and +100bp QoQ), ahead of our estimate of 13.2%. Margin beat was driven by much lower other expenses, which was a surprise. Other expenses declined 10% QoQ, while revenue rose 14% QoQ.

* As a result, EBITDA beat our estimates, rising ~21% YoY to INR7.8b.

* However, due to higher-than-expected depreciation and lower other income, PAT missed our estimates and was up 2.7% YoY at ~INR5.7b (est. INR6.2b).

* For FY26, revenue/EBITDA/adj. PAT grew by 10.8%/14.8%/16.5% to INR200.3b/INR26.5b/INR23.4b.

* The CFO for the year stood at INR21.8b, with FCF of INR18.6b.

* The Board announced a final dividend of INR270/equity share, compared to INR512/equity share last year.

Valuation and view

Management provided a cautious outlook across all auto segments for 2026, given the ongoing geopolitical uncertainty. Further, while BOS continues to work toward localization of new technologies, given the long gestation of projects, its margin remains under pressure with no visibility of material improvement in the near term. We project BOS to clock a 22%/27%/14% CAGR in revenue/EBITDA/PAT over FY26-28. The stock at 39.3x/33.7x FY27E/FY28E appears fairly valued. We reiterate our Neutral rating with a TP of INR37,499 (based on ~36x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412