Buy Page Industries Ltd for the Target Rs 45,000 by Motilal Oswal Financial Services Ltd

Strong exit to FY26; positive commentary for volume-driven FY27

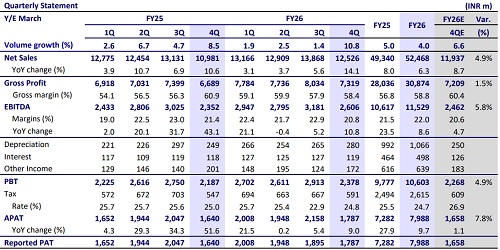

* Page Industries (PAGE) posted strong 4QFY26 performance, with revenue growth of 14% YoY (est. 9%) and volume growth of 11% (vs. est. 6.6%; 1.4% in 3QFY26). There was a sharp growth recovery in 4Q after 4% revenue growth in 9MFY26. The recovery in consumer demand was encouraging and provided confidence that the trend can sustain, at least in the near term. Athleisure demand recovered as channel inventory normalized. JKY Groove witnessed strong traction and expanded across 500 EBOs, select MBOs, and e-commerce channels.

* GM contracted 250bp YoY to 58.4% (est. 60.4%, 57.9% in 3QFY26) due to inflation in cotton and other RM. The company implemented ~2% price hikes in Jan’26, linked to product upgrades. Additional hikes are likely in 1QFY27 to offset input cost pressures. FG/RM inventory days increased to 73 from 64 at the start of FY26, driven by strategic stocking amid RM inflation and ahead of seasonally strong 1Q demand.

* EBITDA margin contracted 60bp YoY to 20.8%. Management maintained its FY27 EBITDA margin guidance of 19-21% (vs. 22% in FY26). Investments focused on marketing and business will remain elevated in FY27.

* PAGE exited FY26 on a strong note after muted growth during most of the year (6% revenue, 4% volume in FY26). The company aims to achieve double-digit volume growth in FY27 (we model 8%) despite price hikes. According to the company, competitive pressure has been easing out compared to a year ago, as the industry is experiencing consolidation (particularly for D2C). Improving macro conditions and the company’s own initiatives are expected to drive volume growth. Initiatives for product innovation, marketing (particularly on social media platforms), and new channel expansion are encouraging. We model an 11% revenue and 11% EBITDA CAGR over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR45,000, premised on 50x FY28E EPS.

Highlights from the management commentary

* Demand recovery was particularly visible in March, while January and February also witnessed better traction versus the first three quarters of FY26.

* Management stated that the gap between value growth and volume growth was largely driven by premiumization and favorable product mix rather than price hikes.

* Management indicated that competitive intensity has reduced meaningfully compared to 1–2 years ago. Several D2C and emerging brands have either reduced offline expansion, consolidated operations, or lowered discounting and marketing intensity.

* Inventory days increased to 73 days at the end of FY26 versus 64 days at the beginning of the year. Net working capital days increased marginally to 56 days from 54 days.

Valuation and view

* We raise our EPS estimates by 3-4% for FY27 and FY28 on better delivery of revenue growth in 4QFY26.

* PAGE exited FY26 on a strong note after muted growth during most of the year (6% revenue, 4% volume in FY26). The company aims to achieve double-digit volume growth in FY27 (we model 8%) despite price hikes. According to the company, competitive pressure has been easing out compared to a year ago, as the industry is experiencing consolidation (particularly for D2C). Improving macro conditions and the company’s own initiatives are expected to drive volume growth. Initiatives for product innovation, marketing (particularly on social media platforms), and new channel expansion are encouraging. We model an 11% revenue and 11% EBITDA CAGR over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR45,000, premised on 50x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)