Buy Metro Brands Ltd for the Target Rs 1,250 by Motilal Oswal Financial Services Ltd

Strong end to FY26; remains confident of delivering ~15% revenue CAGR

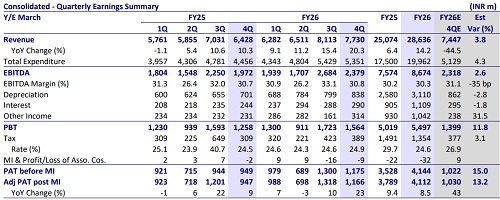

* Metro Brands’ (MBL) revenue growth further improved to ~20% YoY in 4QFY26 (vs. ~15% YoY in 3Q), driven by acceleration in store additions, recovery in in-store sales (~16% YoY vs. ~11% YoY in 3Q), and rising traction in e-commerce (+53% YoY).

* Profitability (4Q EBITDA up 21% YoY) remains intact despite increased marketing spends to boost in-store footfalls.

* For FY26, MBL met its guidance on revenue growth (~14% YoY) as well as profitability (30%+ EBITDA margin and mid-teen PAT margin).

* MBL's revenue growth has experienced a steady pick-up since 2HFY25, driven by rising traction in e-commerce, acceleration in store additions, and likely replacement demand kicking in after a three-year hiatus.

* While BIS-related challenges persist for the S&A category (Foot Locker and FILA), we believe there are enough triggers for MBL to sustain double-digit growth over the medium term.

* We raise our FY27/28E EBITDA by 2%/5%, driven largely by higher revenue growth on the back of acceleration in store expansion. Given the strong runway for growth in the Metro, Mochi, and Walkway formats, along with significant growth opportunities in FILA/Foot Locker/Clarks, we model a revenue/EBITDA/adj. PAT CAGR of 17-18% over FY26-28E.

* We reiterate our BUY rating on MBL with a revised TP of INR1,250 (earlier INR1,215), premised on an unchanged ~40x FY28 Pre-IND AS EV/EBITDA multiple (implied ~60x FY28 P/E).

Key takeaways from the management commentary

* Input cost pressures: Raw material inflation of nearly 10% was seen across categories. However, forward buying of raw materials and front-loading of inventory were undertaken to reduce cost pressures. Existing inventory visibility and sourcing arrangements are expected to make the impact gradual rather than immediate. No major price hikes are planned apart from normal inflationary increases.

* Inflation effect on demand: Management believes that footwear remains a lowfrequency and low-ticket purchasing category, which limits the inflationary impact on demand. Further, MBL’s premium customer base and product proposition cushion it from the demand volatility typically seen during an inflationary period in mid-premium and mass categories.

* Growth outlook: Marketing initiatives, improved product designs, and customer acquisition efforts drove higher in-store footfalls and improved business momentum. Long-term growth expectations continue to remain over 15%. However, periodic fluctuations caused by factors such as wedding dates and festival timings can create quarterly volatility.

* Walkway: Walkway continues to benefit from the large opportunity available across tier 2+ towns. The shift from unorganized to organized footwear retail remains a significant long-term growth driver for the banner. Given the relatively low market share and large market opportunity, management expects a long runway for growth, with an improvement in profitability and RoCE trends

Valuation and view

* MBL's revenue growth has experienced a steady pick-up since 2HFY25, driven by rising traction in e-commerce, acceleration in store additions, and likely replacement demand kicking in after a three-year hiatus.

* While BIS-related challenges persist for the S&A category (Foot Locker and FILA), MBL has intensified its focus on the value category (Walkway), signed strategic partnerships (New Era and Clarks), and launched a new sports performance format (MetroActiv). These initiatives should help sustain double-digit growth over the medium term.

* We remain positive on MBL's long-term outlook, given:

1) its superior store economics, with industry-leading store productivity and strong cost controls

2) the strategic tie-ups with leading brands

3) a long runway for growth in its core formats, primarily funded through internal accruals.

* We raise our FY27/28E EBITDA by 2%/5%, driven largely by higher revenue growth on the back of acceleration in store expansion. Given the strong runway for growth in the Metro, Mochi, and Walkway formats, along with significant growth opportunities in FILA/Foot Locker/Clarks, we model a revenue/EBITDA/adj. PAT CAGR of 17-18% over FY26-28E.

* We reiterate our BUY rating on MBL with a revised TP of INR1,250 (earlier INR1,215), premised on an unchanged ~40x FY28 Pre-IND AS EV/EBITDA multiple (implied ~60x FY28 P/E). Consistent double-digit revenue growth and ramp-up of newer formats, such as FILA, Foot Locker, and Clarks, remain the key re-rating triggers

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)

Ltd.jpg)