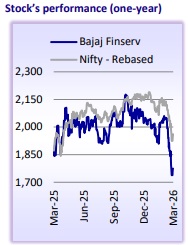

Buy Bajaj Finserv Ltd for the Target Rs.1,900 by Motilal Oswal Financial Services Ltd

Building a one-stop financial shop!

Spreading wings across the financial ecosystem

* Bajaj Finserv (BJFIN) is the holding company of India’s largest NBFC – BAF (51.3% stake), third largest general insurer – BGen (77.3% stake) and sixth largest private life insurer – BLife (77.3% stake). The group aims to build a comprehensive, technology-led financial services ecosystem that spans lending, insurance, investments, healthcare etc. ? In lending, Bajaj Finance (BAF) provides the scale, profitability and ~110m customer base (54% of revenue in 9MFY26). The AUM has grown at FY20-25 CAGR of ~23% and reached ~INR4.8t at the end of 9MFY26. BAF remains the core value contributor, providing predictable earnings, strong ROE and sustained compounding.

* The general insurance subsidiary, Bajaj General (BGen – 24% of 9MFY26 revenue), is India’s third largest general insurer with YTDFY26 market share of 7.1% and one of the most profitable general insurers (9MFY26 CoR – 100.8%). BGen is the third largest private player in motor segment, the largest private multi-line insurer in health segment and the second largest private player in the fire segment. With its diversified exposure in retail and higher-margin commercial and group health segments, along with continued tech-led efficiency gains, the business is positioned to clock a GWP CAGR of 12% during FY26-28 while sustaining the best-in-class combined ratios.

* The life insurance subsidiary, Bajaj Life (BLife – 22% of 9MFY26 revenue), has transitioned from a ULIP-heavy, low-margin insurer to a more balanced franchise with FY20-25 APE CAGR of 28% and VNB margin expansion from 9.9% in FY20 to 16.4% in 9MFY26. With continued product mix shift toward traditional, scale-up of protection business, and growth across channels, the next phase is expected to deliver VNB growth (19% FY26-28 CAGR) ahead of APE growth (15% FY26-28 CAGR) and steady EV compounding, strengthening its position among leading private life insurers.

* New-age platforms across broking, asset management, financial product distribution, healthcare and technology services extend BJFIN’s presence across the full financial lifecycle of the customer. These businesses are designed to be assetlight, scalable and synergistic, creating multiple growth options without materially increasing balance-sheet risk. While currently contributing only ~1% to revenue and investing in scale to achieve breakeven, these emerging subsidiaries provide the opportunity for the brand to be involved in all financial decisions of customers.

* We expect the PAT from the established businesses - BAF and BGen and VNB of BLife to steadily grow at a FY26-28 CAGR of 28%/16%/19%, while emerging businesses to gradually move toward breakeven as they scale up. BJFIN’s revenue/PAT is expected to clock a CAGR of 15%/17% in FY26-28, with RoE in the range of 13-14%. Based on SoTP, we arrive at a TP of INR1,900, implying FY28E P/E of 22x. Initiate with NEUTRAL Rating

Bajaj Finance – India’s lending powerhouse

* BAF is India’s largest NBFC with a diversified retail and SME lending franchise, with AUM and PAT growing at 10-year CAGR of ~34%.

* Despite its scale, BAF’s retail credit market share remains at ~2.8%, with leadership in only two of its 27 products. The next phase of growth is anchored to wallet share expansion within its ~90mn cross-sellable customers, supporting sustainable high-teens compounding.

* BAF is aiming to lower acquisition costs, improve credit outcomes, and enable scale without proportional balance sheet risks through deep integration of AI across underwriting, operations, and risk management.

* With improving asset quality, declining credit costs, and a focus on becoming a low-risk financial institution, BAF remains well positioned to compound profitably through cycles. We have a TP of INR900 (based on 3.6x Dec’27E BVPS).

Bajaj General Insurance – Scaling with discipline

* India’s third largest insurer, BGen, has steadily gained market share from 6.8% in FY20 to 7.1% in YTDFY26 while maintaining superior underwriting discipline and consistent profitability.

* BGen has been among the top private players across each segment – motor OD at 7.6% in YTDFY26 (third largest private player), motor TP at 6.1% (fourth largest private player), fire at 10.1% (second largest private player), retail health at 2.2%, group health at 5.3% and 35% market share in government health. ? With non-life penetration at ~1% of GDP, long-term growth for the industry is supported by rising automobile sales, improving awareness, healthcare inflation, and infrastructure expansion. BGen is well positioned to benefit from these trends with exposure across all segments and a balanced portfolio approach.

* BGen has consistently prioritized pricing discipline and selective underwriting, enabling industry-leading combined ratios (102.9% in 1HFY26 vs. ~119.2% for industry) even during periods of heightened competition. This is also supported by excess capital (300%+ solvency) with a stable retention ratio (~42%), ensuring protection against catastrophic losses and health loss ratios.

* BGen has a wide multi-channel network with 10%/7%/28%/48% contribution from agents/banks/brokers/direct during 9MFY26. Continued investments in digital and AI platforms have delivered steady cost efficiencies and enabled further opex ratio improvement to 22.7% by FY28 from 23.5% in FY25.

* Despite operating in segments that are inherently volatile, e.g., group health, crop and commercial lines, the company has maintained better combined ratios in the industry, supported by granular pricing and loss control. We expect the combined ratio to trend near 99% by FY28, with FY26-28 PAT CAGR of 16%, supported by steady GWP expansion and stable cost efficiency trends.

Bajaj Life Insurance – Building a turnaround in life insurance industry

* BLife has transformed from a loss-making, ULIP-heavy franchise in FY17 into the second-largest non-bank life insurer, with FY20-25 APE/VNB CAGR of 28%/38% and VNB margin expansion to 16.4% in 9MFY26 (11.1% in 9MFY25).

* It is operating in a structurally underpenetrated market, providing a long growth runway, supported by rising incomes, improving financial awareness, regulatory reforms and GST removal on life insurance.

* APE market share (within private) expanded from 4.8% in FY20 to 7.4% in YTDFY26, supported by multi-channel distribution, product innovation and persistency improvement initiatives. A balanced presence across agency, bancassurance and direct channels with strong institutional partnerships (notably Axis Bank) provides scalability, stability and sourcing quality.

* A deliberate shift toward traditional and protection products, along with disciplined ULIP pricing and rising rider attachment, is structurally improving VNB margins despite near-term product mix volatility.

* BLife is entering the next phase of growth, targeting ~2x industry growth, higher protection contribution and operating RoEV of 14-15%, translating into sustained EV compounding from INR238b in FY25 to INR362b by FY28.

* BLife also operates at a strong solvency ratio of 300%+. The common parentage of BLife and BGen enables selective distribution and product-level synergies. The group is exploring coordinated outreach in segments such as MSMEs and potential bundled offerings across protection and health/PA, leveraging its shared distribution relationships. If a composite license were to come into play, BJFIN as a group would be one of the biggest beneficiaries owing to existing synergies between the two insurers

Emerging subsidiaries – covering all financial needs

* Bajaj Finserv Health (BFH) has evolved into a full-stack, payer-led health platform, integrating OPD, IPD and wellness services. Following the acquisition of Vidal Healthcare, the platform now services a network of 133,000+ doctors, ~16,000 hospitals and ~6,300 diagnostics centers, with a breakeven expected in a few years as scale-driven operating leverage plays out.

* Bajaj Finserv Direct (BFD) operates as an open-architecture digital marketplace for loans, insurance and investment products (Bajaj Markets) and also delivers domain led enterprise solutions to BFSI industry (Bajaj Technology Services). A continued scale-up should drive a breakeven. The business has already turned cash-positive, reflecting improving operating leverage and capital efficiency.

* Bajaj Finserv AMC (BFAMC), a recent entrant, has scaled up rapidly, with AUM reaching ~INR300b as of Dec’25, supported by strong traction in new fund launches and distributor onboarding. With ~680,000 investors and a growing distribution base, the AMC is building a differentiated investment franchise.

* While these businesses are currently modest contributors to consolidated profits, they represent scalable, asset-light platforms aligned with the group’s long-term strategy of building a comprehensive financial services ecosystem. As scale improves and profitability is achieved, emerging subsidiaries are likely to become more meaningful contributors to BJFIN’s growth and valuation.

Valuation and View

* BJFIN is entering a phase where growth is increasingly broad-based, with BAF providing earnings stability, insurance businesses transitioning into margin-led, value-accretive growth, and new digital platforms moving closer to scale and breakeven. Improved execution across life and general insurance, alongside disciplined capital allocation in emerging subsidiaries, enhances visibility on consolidated value creation over the medium term. Given the diversified earnings profile, a strong balance sheet and improving contributions from nonlending businesses, BJFIN merits a premium holding-company valuation.

* We expect the PAT from the established businesses, BAF and BGen and VNB of BLife to steadily grow at a FY26-28 CAGR of 28%/16%/19%, while emerging businesses gradually move toward breakeven as they scale up. BJFIN’s revenue/PAT is expected to clock a CAGR of 15%/17% in FY26-28, with RoE in the range of 13-14%. Based on SoTP, we arrive at a TP of INR1,900, implying FY28E P/E of 22x. Initiate with NEUTRAL Rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

-96767.jpg)