Buy Allied Digital Corp.Ltd for the Target Rs.180 by Choice Institutional Equities

Execution Stabilising; Growth Visibility Improves; Maintain BUY

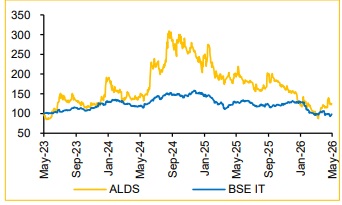

We believe ALDS is entering a more stable execution phase, supported by improving demand visibility, a structurally stronger services mix, and increasing operating discipline. While near-term volatility in public-sector execution and pricing pressure may persist, improving order visibility and rising contribution from higher-margin services should support earnings quality over the medium term. We maintain our BUY rating and continue to value the stock at 15x on FY28 EPS, resulting in a TP of INR 180 (unchanged), as improving execution, margin normalisation, and stronger deal conversions support the medium-term growth outlook.

Revenue Beats; Margin Disappoints due to Auditor Adjustments

* Revenue for Q4FY26 came at INR 2,678 Mn, up 8.2% QoQ & 31.0% YoY (vs CIE est. at INR 2,582 Mn)

* EBITDA for Q4FY26 came at INR -101.2 Mn, down 138.7% QoQ and 8.8% YoY (vs CIE est. at INR 271 Mn). EBITDAM stood at -3.8% vs 10.6% in Q3FY26, down 1435 bps QoQ (vs CIE est. at 10.5%).

* PAT for Q4FY26 stood at INR -34.0 Mn, down 124.4% QoQ and 55.5% YoY (vs CIE est. at INR 160.8 Mn).

Healthy FY26 Performance; Pipeline Supports FY27 Outlook

ALDS reported resilient FY26 revenue growth of 19.9% YoY despite a challenging environment. Management targets sustainable long-term growth of 20–25%, supported by a higher services mix to improve consistency and visibility. Over the longer term, the company aspires to achieve up to 10x growth over the next decade. The pipeline remains strong, with INR 20,000 Mn of potential orders from projects in Maharashtra and government contracts. Domestic and international markets, particularly the US, Latin America, and Africa, continued to show healthy momentum. Although Iran-Israel tensions temporarily delayed some Indian government tenders, demand for AI-led transformation remains robust, especially in the US BFSI segment. We expect FY27E growth of 20.2%, with estimates revised upward by 4.1%, supported by an expected Mumbai order win worth INR 1,500–2,000 Mn and rising enterprise outsourcing for AI integration and managed services.

Margin Poised for Recovery on Operational Improvements

ALDS reported Q4FY26 EBITDAM of -3.8%, declining 1,435 bps QoQ but improving 44 bps YoY, due to elevated other expenses and a one-time INR 357 Mn provision following the revised ECL policy for assets. Adjusted EBITDAM came in at 9.6% vs 10.6% in Q3FY26. Management expects margin to rebound to 11–12% in FY27E and expand to 13–15% over the longer term, supported by streamlining and completed exceptional adjustments. We conservatively forecast FY27E EBITDAM at 8.9%, aided by AI-led automation and ramp-ups of recent contract wins.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131