Neutral Repco Home Finance Ltd for the Target Rs 435 by Motilal Oswal Financial Services Ltd

Healthy disbursements; high runoff weighs on growth Elevated opex continues to drag down profitability; asset quality improves

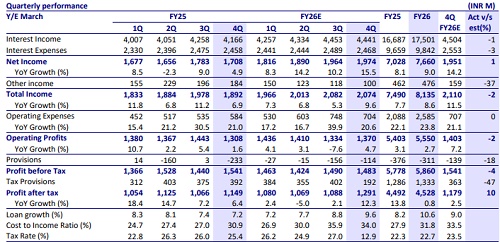

* Repco Home Finance’s (Repco) 4QFY26 PAT grew 12% YoY to INR1.3b (~10% beat). FY26 PAT remained flat YoY at ~INR4.5b.

* 4Q NII grew ~16% YoY to ~INR2b (in line). Other income declined ~45% YoY to INR100m (vs. est. of INR159m).

* Opex rose ~21% YoY to INR704m (in line). 4Q PPOP grew ~5% YoY to INR1.4b (in line). FY26 PPoP grew ~3% YoY to ~INR5.6b.

* Provision write-backs stood at ~INR114m, translating into annualized credit costs of -29bp (PY: -65bp and PQ: -41bp).

* Repco expects growth momentum to strengthen in FY27, supported by improving disbursement traction across non-Tamil Nadu markets such as Maharashtra, Karnataka, Andhra Pradesh, MP and Rajasthan. The company is expanding its on-ground sourcing network through additional feet-onstreet hires while maintaining a largely internal sourcing model.

* With Karnataka’s e-khata issue resolved and team restructuring completed in AP, incremental growth from these regions is expected to improve. Additionally, Repco is also recalibrating lending rates to retain quality customers, while remaining disciplined on underwriting standards. The company targets disbursements of ~INR50b and AUM of ~INR180b in FY27.

* Prepayments and BT-outs for Repco remained high, largely driven by public sector banks offering lower interest rates and attracting vintage customers. Structurally, prepayments also stay higher due to the self-employed borrower base, where borrowers tend to prepay when surplus business cash flows are generated or upon asset sale proceeds, leading to early loan closures. While BT-ins continue from HFCs, Repco is focusing on accelerating disbursements to support growth and partially offset portfolio runoff.

* We believe stable AUM growth in line with management guidance, supported by disciplined runoff management, will be key to rebuilding investor confidence and driving a meaningful re-rating over the medium term. While Repco has taken steps to contain BT-outs and improve growth through higher disbursements, the benefits are yet to meaningfully flow through. Continued improvement in asset quality remains a key positive, reinforcing underwriting strength and portfolio resilience.

* Our earnings estimates are largely unchanged and we model a loan/PAT CAGR of ~12%/5% over FY26-FY28E with RoA/RoE of 2.6%/11% in FY28E. We reiterate our Neutral rating on the stock with a revised TP of INR435 (based on 0.6x FY28E BVPS).

Steady improvement in asset quality; benign credit cost outlook

* GS3 declined ~35bp QoQ to ~2.6%, while NS3 declined ~20bp QoQ to ~1.2%. PCR on S3 loans improved ~2.2pp QoQ to ~55%.

* For the book originated from Apr’22 onward, GS2 stood at 3.9% (vs. 7% for the overall book) and GS3 stood at 1% (vs. 2.6% for the overall book).

* Management shared that it is seeing a continued improvement in delinquency trends, supported by strengthened recovery and we expect Repco’s credit costs to remain benign at ~7bp/15bp in FY27E/FY28E.

Valuation and view

* Repco’s near-term outlook depends on sustaining disbursement-led growth while managing structural runoff from prepayments and BT-outs. Improvement in asset quality, led by lower Stage 2 levels, supports a stable credit profile. Growth may remain moderated due to competitive pricing and self-employed borrower behavior, though expansion in non-Tamil Nadu markets and calibrated rate actions are key levers. Overall, execution on growth and portfolio quality will drive FY27 performance.

* The company currently trades at ~0.6x FY27E P/B. We model a loan/PAT CAGR of ~12%/5% over FY26-FY28E with RoA/RoE of 2.6%/11% in FY28E. We reiterate our Neutral rating on the stock with a revised TP of INR435 (based on 0.6x FY28E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412