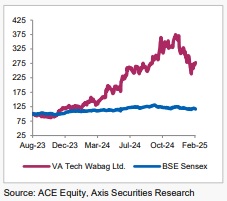

Buy VA Tech Wabag Ltd For the Target og Rs. 1,970 By the Axis Securites

Recommendation Rationale

Order Pipeline Strengthening: The company has secured new orders totalling over Rs. 2,781 Cr this quarter, increasing its total order book to around Rs 14,200 Cr (including framework contracts). It also recently won a consortium order worth Rs 3,251 Cr ($371 Mn) for the Al Haer Independent Sewage Treatment Plant in Riyadh, Saudi Arabia. With this, the company is now likely to surpass the order book target of over Rs 16,000 Cr by the end of this fiscal year.

Margins to improve with revenue growth acceleration: The recent orders are expected to accelerate revenue growth starting FY26. Management has guided a 15- 20% revenue CAGR over the next three to five years. The sustained revenue growth and improving product mix are also expected to drive profit margins higher in the medium term.

Improving Cash Cycle: The company has now been net cash positive for the eighth consecutive quarter, with a net cash position of Rs 263 Cr as of Q3FY25. It continues to focus on reducing working capital requirements and expects further improvement in the coming quarter

Sector Outlook: Optimistic

Company Outlook & Guidance: The management anticipates strong revenue growth driven by India and MEA, projecting a CAGR of 15%-20% over the next 3-5 years. EBITDA/PAT growth is expected to outpace revenue growth, with EBITDA margins ranging between 13%- 15% and potentially exceeding the upper end of this guidance. The company currently holds a robust order book of approximately Rs 14,200 Cr, aims to surpass Rs 16,000 Cr by FY25, and targets order book 3X of revenue in the medium term. The targeted revenue mix, which includes over 50% from international projects, 30% from industrial customers, 20% from O&M, and one-third of EPC being EP projects, is expected to contribute to margin improvement.

Current Valuation: 21x FY27E (unchanged)

Current TP: 1970/share (unchanged)

Recommendation: We maintain our BUY rating on the stock

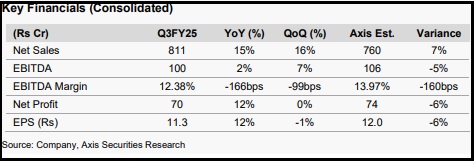

Financial Performance: The company reported revenue of Rs 811 Cr, reflecting a substantial 15% YoY growth and a 16% QoQ increase, surpassing our estimate of Rs 760 Cr. EBITDA margin came in at 12.38%, below our estimate of 13.97%. EBITDA stood at Rs 100 Cr, up 2% YoY and 7% QoQ, below our estimate of Rs 106 Cr. This performance resulted in a PAT of Rs 70 Cr, marking a 12% YoY growth, missing our estimate of Rs 74 Cr by 6%. The company reported an EPS of Rs 11.29/share. The order intake for the period stood at Rs 2,781 Cr, with the order book at over Rs 14,200 Cr, including framework contracts.

Outlook: VA Tech Wabag Ltd. (VTW) has consistently grown its order book while strategically enhancing its revenue quality and predictability, which aligns with this focus. The company is looking to increase its share of more profitable international, industrial, and O&M contracts. With its current order book providing clear revenue visibility for the next 3-4 years, especially in terms of international orders, these strategic efforts are expected to help the company achieve its targeted margins, further strengthening its financial position and business sustainability.

Valuation & Recommendation: Our revised estimates reflect the expectation that some of the revenue growth and margin improvement will be pushed over from FY25 to FY26 and beyond. However, our long-term view remains positive. Consequently, we maintain our BUY rating and continue to value the stock at 21x FY27E. Our target price remains unchanged at Rs 1,970/share, implying an upside of 39% from the current market price (CMP).

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633