Buy L&T Finance Ltd for the Target Rs 340 by Motilal Oswal Financial Services Ltd

Lakshya 2031: Building a premier AI-enabled retail financier

Risk First. Tech First. Scale Ready. Retailization complete; AI journey begins FY26 marked a strategic inflection point for L&T Finance (LTF) as the company concluded its Lakshya 2026 transformation roadmap and now transitions into the next growth phase under Lakshya 2031. The company has effectively transformed itself from a diversified, wholesale-oriented financier into a predominantly retailfocused NBFC with 98% retailization, an INR1.2t total loan book, and one of the most technology-intensive operating models within the Indian NBFC sector. Despite macroeconomic volatility and stress in the microfinance ecosystem, LTF delivered a healthy FY26. The bigger story, however, lies in the development of institutional architecture around AI-led underwriting, digital servicing, cross-sell ecosystems, and granular retail franchise expansion.

* Over the last four years, LTF has transformed itself from a diversified, wholesale-oriented lender into a granular, retail-focused financier anchored on a “Risk-First, Tech-First” operating philosophy. A key highlight of FY26 was the deepening integration of proprietary AI-led underwriting, monitoring, and servicing capabilities across business verticals. Platforms such as Project Cyclops, Project Nostradamus, Project Helios, Project Orion, and the PLANET ecosystem have collectively strengthened customer acquisition, underwriting precision, portfolio monitoring, collections efficiency, servicing, and cross-sell capabilities.

* LTF also strategically entered the high-yield secured gold finance segment through the acquisition of Paul Merchants Finance’s gold loan business. Within a relatively short period, it expanded the gold loan branch network to 330 branches and is positioning gold finance as one of the key fulcrum businesses under the Lakshya 2031 roadmap, aided by strong cross-sell opportunities within its existing rural and retail customer base.

* Going forward, Lakshya 2031 aims to position LTF as India’s premier AIenabled retail BFSI franchise. The next phase of growth is expected to be driven by technology-led execution, resilient and granular portfolios, AIenabled cross-sell engines, productivity enhancement initiatives, and a sharper focus on sustainable profitability improvement.

* Management has guided for more than 20% loan book growth, <2% credit costs, RoA of 3.0-3.2%, and RoE of 16-18% over the medium term under Lakshya 2031. We believe the company’s granular retail franchise, AI-led operating architecture, expanding secured product mix, and improving cross-sell capabilities position it well to deliver sustainable earnings compounding over the next few years.

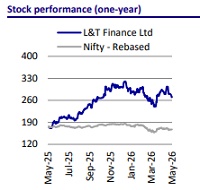

* We expect LTF to deliver a PAT CAGR of ~28% over FY26-28, driven by healthy retail loan growth, operating leverage benefits from technology investments, moderation in credit costs, and improving profitability across key business segments. Consequently, we estimate the RoA/RoE to improve to 2.6%/15.0% by FY28. We reiterate our BUY rating on LTF with a TP of INR340, based on 2.4x Mar’28E P/BV, supported by improving return ratios, strengthening franchise quality, and the company’s emergence as a scalable AI-enabled retail financial services platform.

Gold finance could become a major growth driver

* The acquisition of the gold finance business from Paul Merchants may emerge as one of the most strategically important decisions for LTF. Gold loans offer secured lending, high yields, lower credit costs, faster loan cycles, and strong rural cross-sell potential.

* Within only eight months, LTF has added 200+ gold loan branches, and the total number of gold branches has surpassed 330. Management also highlighted that many of its existing MFI and farmer finance customers already have unmet gold loan demand, making cross-sell economics attractive. This will help LTF improve the secured loan mix, reduce volatility of earnings, deepen customer engagement, and increase lifetime customer value.

Valuation and View

* LTF’s transformation into a granular, technology-led retail financier is now visibly translating into stronger business fundamentals, improving resilience, and scalable growth opportunities. Importantly, LTF has demonstrated relatively superior navigation through the ongoing MFI credit cycle, while simultaneously diversifying into relatively less leveraged and more secured retail segments, thereby strengthening the overall quality and resilience of the franchise.

* With a rapidly expanding retail ecosystem, growing cross-sell capabilities, improving secured product mix, and technology-led operating leverage, we expect LTF to deliver a PAT CAGR of ~28% over FY26-28E, resulting in RoA/RoE of 2.6%/15% by FY28E. We reiterate our BUY rating on LTF with a TP of INR340, based on 2.4x Mar’28E P/BV. Key risks to our thesis include NIM compression arising from increasing focus on prime customer segments, potential asset quality deterioration in relatively vulnerable retail products such as twowheeler finance, unsecured business loans, and micro-LAP, and moderation in growth or elevated stress in rural portfolios amid uncertain geopolitical and macroeconomic conditions.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412