NBFCs Sector Update : Healthy Credit Demand to Drive NII Growth; Asset Quality Remains Key Monitorable by Choice Institutional Equities

AUM Growth Momentum for NBFCs is Expected to Remain Resilient across Segments in Q1FY27E; Sector Outlook Remains Positive

We maintain a positive outlook on India’s NBFC sector on account of sustained credit demand in Q1FY27E, which in turn is majorly driven by stronger momentum across Gold Financing, Housing Loans, SME Loans and Vehicle Financing (excluding CV segment).

Our Coverage Universe

Gold Loan AUM, driven by rapid expansion of branch network and maturation of existing branches, is anticipated to grow at 101.2% YoY. Housing Loan AUM is expected to grow at 45.8% YoY, led by stronger demand across borrower profile. 2-Wheeler Loan is forecast to increase at 26.9% YoY on account of buoyant auto demand across rural and urban India, whereas SME Loan AUM is anticipated to grow at 21.6% YoY, led by higher need for working capital loan due to West Asia conflict. We believe the Cost of Funding (CoF) for our coverage universe is expected to remain range-bound, as 10-year G-sec yield advanced upwards, which impacted NBFCs’ NCD borrowing programme. Moreover, bank borrowing rates for NBFCs are not projected to decline in Q1FY27E, as the latter were highly dependent on term loans. We estimate overall credit cost for our coverage universe to remain stable largely on account of improved underwriting norms practiced by the companies

Sector View

We anticipate credit offtake across NBFCs to expand at 16.0%–18.0% CAGR over FY26–FY28E. Led by stronger formal credit demand, we believe that NBFCs are projected to gain market share from banks, driven by stronger loan origination, shorter TAT and niche emphasis on product categories. We forecast the CV Loan segment to underperform the overall credit growth in the short term, affected by the ongoing West Asia conflict, with inch-up in NPAs across CV financiers. Some stress is projected in the MSME segment in Q1FY27E affected by the conflict, which, we believe, would be transitory in nature. Gold Loan Financers are anticipated to witness stronger credit growth on account of recent custom duty hike and expansion of physical branch network. Yields are forecast to witness compression due to intense competition, whereas the asset quality is anticipated to remain contained.

High-conviction Investment Idea

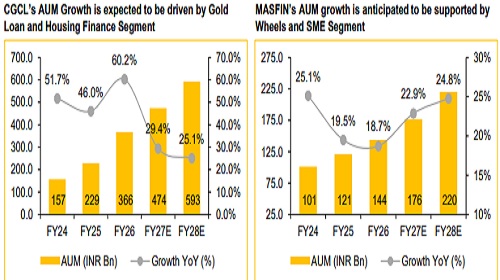

We maintain a positive stance on Capri Global, which is expected to deliver strong AUM growth in Q1FY27E.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

Tag News

Trade Idea of The Day - Bajaj Finance Ltd Target Rs. 45 - Religare Broking Ltd