Buy Infosys Limited for Target Rs. 1450 - Religare Broking Ltd

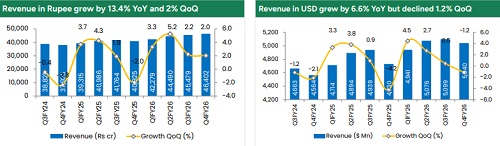

Strong Financial Performance with Margin Stability: Infosys delivered a resilient Q4FY26 performance, with net profit rising 21% YoY to ?8,509 crore and revenue growing 13.4% YoY, reflecting steady execution despite a challenging macro environment. Operating margins remained stable at 21%, supported by structural cost initiatives such as Project Maximus, higher utilization, automation, and improved realizations. Sequential margin improvement was aided by the absence of one-off costs seen in Q3. The company also reported strong free cash flow of $3.5 billion in FY26, highlighting disciplined capital allocation and operational efficiency. Overall, Infosys demonstrated its ability to sustain profitability and protect margins even as revenue growth remained moderate.

Deal Wins Strong, but Conversion Slower: : Infosys continued to show strong deal momentum, with Q4FY26 TCV at $3.2 billion and full-year TCV (Total Contract Value) reaching $14.9 billion, marking healthy growth YoY. Importantly, 55% of deals were net new, indicating fresh client additions and increased wallet share. However, the key challenge remains slower deal conversion and delayed ramp-ups, as clients defer discretionary spending amid macro uncertainty. While vendor consolidation trends are favorable, with clients preferring fewer strategic partners, revenue realization timelines are extending. Europe remains relatively strong, but elongated execution cycles mean that strong deal wins are not immediately translating into revenue acceleration in the near term.

AI Double-Edged Impact on Growth: Infosys is aggressively advancing its AI strategy through platforms like Topaz and Cobalt, with over 4,600 AI projects underway, spanning generative AI, automation, and data transformation. Strategic partnerships with global leaders further enhance its capabilities and market positioning. However, AI is also acting as a near-term headwind, as productivity gains enable clients to achieve more with lower IT spending, leading to pricing pressure in traditional services. While Infosys is securing higher-value, premium AI-led transformation deals, the revenue offset is gradual. Over time, AI is expected to drive significant growth, but in the near term, it contributes to slower revenue expansion despite efficiency gains.

Demand Environment Remains Weak: The demand environment remains cautious, with macroeconomic uncertainty continuing to impact client spending behavior across key sectors. Discretionary spending in Retail, Manufacturing, and Communications remains weak, leading to delayed decision-making and slower deal ramp-ups. Clients are increasingly prioritizing cost optimization, automation, and efficiency-led initiatives over large-scale transformation programs. Financial Services and Energy & Utilities segments show relatively better resilience, supported by regulatory requirements and infrastructure investments. Geographically, Europe remains stable, while the US continues to face demand softness. Overall, the shift from growth-led to efficiencyled spending supports Infosys’ strengths but limits near-term revenue acceleration.

Execution Strength Supports Stability: Infosys continues to demonstrate strong execution capabilities through workforce optimization and productivity improvements. Attrition has declined significantly to 12.6%, improving employee stability and reducing hiring pressures. The company hired over 20,000 freshers in FY26 and plans similar hiring in FY27, reflecting confidence in longterm demand. Increased adoption of AI tools, automation platforms, and developer copilots is enhancing productivity and reducing delivery timelines. These efficiency gains are critical in sustaining margins in a low-growth environment. Additionally, Infosys’ ability to execute large, complex transformation deals globally reinforces its reputation as a reliable IT partner, making execution a key differentiator.

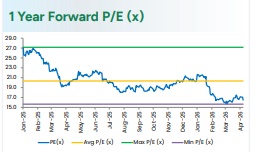

Outlook and Valuation: Infosys has provided a conservative FY27 revenue growth guidance of 1.5%-3.5% (vs FY26 3.0%-3.5%) in constant currency, reflecting macro headwinds, cautious discretionary spending, and AI-led productivity gains. Margin guidance remains stable at 20%- 22%, indicating continued focus on operational efficiency and cost discipline. While near-term growth is expected to remain muted, strong deal wins, a robust pipeline, and expanding AI capabilities provide visibility for gradual recovery over the medium term. We estimate Revenue/ EBIT/PAT CAGR of 10.6%/11.7%/11.6% over FY26-28E and maintain a BUY rating with a revised target price of Rs.1,450.

Please refer disclaimer at https://www.religareonline.com/disclaimer

SEBI Registration number is INZ00017433