Buy Infosys Ltd for Target Rs.1,500 by Choice Institutional Equities

Deal Strength Offsets Growth Constraints INFO delivered a stable quarter with broadly positive full-year performance, though FY27 outlook and guidance weighed on the overall outlook. The record USD-15 Bn deal wins and the 24% YoY TCV growth are genuine positives which underpin revenue visibility for FY27. However, flat volume trends, limited clarity on AI-related deflation, a 75–100 bps impact from a European manufacturing client, and onsite mix pressures are likely to cap near-term revenue growth at around 3.5% unless macro conditions improve. While narrowing down the guidance range signals confidence, the FY27 midpoint of 2.5% CC growth suggests only a modest improvement over FY26’s underlying growth. Factoring in the muted outlook, we forecast Revenue/EBIT/PAT to grow at a CAGR of 9.3%/9.9%/8.0% over FY26–FY29E. Accordingly, we reiterate our BUY rating revising our target price to INR 1,500 (from INR 1,650), based on FY28E EPS of INR 83

Q4FY26 Witnesses Modest Growth with Strong PAT Upside

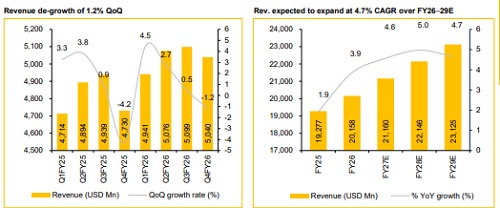

* INFO reported Q4FY26 revenues at USD 5,040 Mn, down 1.2% QoQ (vs CIE estimate of 0.7% QoQ de-growth), while the CC growth stood at -1.3% QoQ. INR revenue stood at INR 464.0 Bn, up 2.0% QoQ (vs CIE estimate of 1.8% QoQ growth). For FY26, USD revenue stood at USD 20,158 Mn up 4.6% YoY, whereas, revenue in INR terms, came in at INR 1,786.5 Bn, up 9.6% YoY.

* EBIT margin came in at 21% for Q4FY26, up 15bps sequentially, whereas, for the full year, EBIT margin stood at 20.9%, down 20 bps YoY.

* PAT for the quarter came in at INR 85 Bn, up 27.8% QoQ (vs CIE estimate of 10.9% QoQ growth). For the full year, PAT stood at INR 294.4 Bn, up 10.2% YoY. EPS for Q4FY26 is INR 21.

Resilient Deal Pipeline amid Soft Growth Outlook

INFO delivered steady growth in large deal TCV at USD 3.2 Bn for the quarter, where 55% deals were net new; and further expected to continue in FY27. The Q4 sequential decline was driven by typical seasonality and delayed client decision-making in March. Energy & Utilities and Hi-tech verticals led growth sequentially, while on YoY basis Communications, Manufacturing and Europe outperformed, growing above the company average, supported by rampup of large deals. BFSI, aided by AI-led transformation and vendor consolidation grew 4.4% in FY26. Manufacturing outlook remains cautious due to weak auto demand and macro headwinds, while FY27 growth is expected to see a 0.75%– 1% impact from ramp-downs of a large European client. Management has guided for revenue growth of 1.5% to 3.5% in CC terms in FY27.

Balanced Margin Despite Multiple Headwinds, Guidance Maintained

INFO reported a stable EBIT margin of 21% for FY26, and 20.9% for the quarter, adjusted for the Labor Code impact in Q3. Margin faced ~100 bps headwinds from acquisition-related amortisation, normalisation of one-off gains and compensation costs, partly offset by ~70 bps tailwinds from currency benefits and operational efficiency under the Maximus program. Management has reiterated its FY27 EBIT margin guidance of 20%–22%, factoring in headwinds from wage hikes, productivity pass-through, AI investments and the optimum healthcare strategy (~70 bps impact), partially offset by efficiency gains under Project Maximus.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131