Buy Infosys Ltd for the Target Rs. 1,450 by Motilal Oswal Financial Services Ltd

Tough road ahead

AI deflation begins to bite as FY27 guidance comes in soft

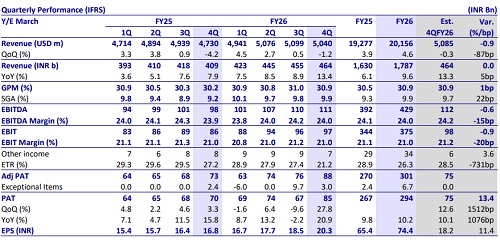

* Infosys (INFO) reported 4QFY26 revenue of USD5b, down 1.2% QoQ. In CC, it was down -1.3% QoQ, below our estimate of -0.7% QoQ. Adj. EBIT margin stood at 21%, below our estimate of 21.2%. Adj. EBIT rose 16.6% QoQ/13.6% YoY to INR97b (est. INR98b). Adj. PAT came in at INR88b, up 15.4% QoQ/21% YoY, above our estimate of INR73b.

* Guidance for FY27 is maintained at 1.5-3.5% YoY cc (vs. our expectation of 1.5-4.5% YoY cc). Adj. EBIT margin guidance was maintained in the 20-22% range. Large deal TCV stood at USD3.2b, down 33.3% QoQ. The book-to-bill ratio was 0.6.

* For FY26, revenue/adj. EBIT/adj. PAT grew 9.6%/8.9%/13.7% YoY in INR terms. In 1QFY27, we expect INFO’s revenue/adj. EBIT/adj. PAT to grow 13.7%/15.5%/13.7% YoY. Free cash flow stood at 125% of net profit for FY26. RoE came in at 31.9% in FY26 (vs. 28.8%/29.8%/32% in FY25/FY24/FY23). We value INFO at 17x FY28E EPS with a TP of INR1,450, implying a 17% upside potential.

Our view: AI deflation to aggravate in the coming year

* Guidance reflects increasing pressure on existing book of business: INFO’s guidance of 1.5–3.5% (1.25–3.25% in organic cc) is below our estimates at the top end, and it tells us that AI is now compressing the existing book of business. While part of this is attributable to competitive intensity and pricing in a low-demand environment, we expect the impact of deflation to continue as AI productivity benefits are passed on to clients.

* We assume INFO to grow at the mid-point of FY27 guidance (~2.5% organic), which is a deceleration vs FY26 (3.1% CC). We estimate FY27E/FY28E revenue growth at 3.7%/3.9% YoY CC.

* Telecom demand shaky amid higher AI-led services delivery: INFO, in line with peers, pointed out that telecom demand remains uncertain in FY27, as clients pare back spends and move to agentic AI across IT and BPS. This comes on the back of a difficult couple of years for the sector, with discretionary spends still selective and decision-making slowing in pockets like manufacturing and Europe. Manufacturing faces a 75–100bp headwind from Daimler ramp-down.

* Deal economics suffering as INFO (and peers) leave deals on the table: INFO is the second company this quarter to highlight large deals being left on the table due to untenable deal economics and high competitive intensity. While large deal TCV remains strong at USD15b (+24% YoY; 4Q at USD3.2b), we believe this trend could pick up pace going forward, possibly as traditional IT service delivery models start to get disrupted. The industry may need to accelerate a pivot to newer, leaner models, and this will be a key monitorable.

* Margins stable as all benefits from INR being re-invested: Margins remained stable at ~21% in FY26, with benefits from currency and Project Maximus being reinvested into AI capabilities, talent, and sales (S&M +40bps YoY). FY27 margin guidance of 20–22% factors in headwinds from wage hikes, AI productivity pass-through, and ~70bp impact from acquisitions, partly offset by efficiency initiatives. We estimate EBIT margins at 20.9%/21.0% for FY27E/FY28E.

* We pare our PAT growth estimates by 3–4%, driven by softer organic growth vs FY26, in line with the 1.5–3.5% FY27 guidance, continued AI-led pricing pressure on the existing book, and vertical headwinds in telecom and manufacturing.

Valuation and changes to our estimates

* We cut our FY27E/FY28E EPS estimates by ~2–4% to reflect lower growth assumptions and continued pricing pressure from AI-led deflation, partly cushioned by lower taxes. Near-term growth remains constrained, with guidance implying ~2.5% organic growth.

* While execution on deal conversion and pricing remains a key monitorable, INFO’s positioning across AI-led transformation and cost optimization programs should support gradual improvement over the medium term. We value INFO at 17x FY28E EPS with a TP of INR1,450, implying ~17% upside. Reiterate BUY rating.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412