Buy Aeroflex Industries Limited for Target Rs. 285 by Arete Securities Ltd

Aeroflex Industries Limited is India's only listed pure-play manufacturer of metallic flexible flow solutions, incorporated in 1993 and headquartered at Taloja MIDC, Navi Mumbai. Its product portfolio spans SS corrugated flexible hoses, assemblies and fittings, metal bellows, composite hoses, and most recently liquid cooling skid assemblies for data centre applications. With 87 production lines across three plants 3,064 SKUs, and a presence in 90+ countries, Aeroflex derives 74% of revenues from exports, with the Americas and Europe accounting for 85% of its export book. Through its wholly-owned subsidiary Hyd-Air Engineering (Pune), Aeroflex also manufactures hydraulic fittings and fluid connectors for railways, shipbuilding, and heavy industry. The company carries zero net debt and is certified under ASME BPVC, NABL, and three ISO standards.

Investment Rationale:

Assembly Mix Upgrade - The Primary Earnings Lever

Assemblies generate 22-25% EBITDA margins against 15-19% for raw hose segment margins while metal bellows contribute 27-30%. The mix has already shifted from 24% assemblies in FY21 to more than 50% currently, with management targeting 70% by FY27E. The new 70 assembly station target (from 46 currently) and 20 million meter hose capacity by Q2 FY27 are the operational enablers of this shift.

Liquid Cooling - A New Business Within the Business

Aeroflex entered the data centre liquid cooling segment in Q3 FY26 under a five-year exclusive India supply agreement with a partner holding 20-25% market share globally. Skid assembly capacity expands from 2,000 to 15,000 units by Q1 FY27 at a total capex of under Rs 100 crore, management guides for 40-50% utilization by FY27, implying peak-year revenues of Rs 300-350 crore at Rs 3 lakh per unit. The revenue-to-capex ratio at peak approaches 3.5x, with segment EBITDA margins guided in line with the corporate blended margins of 22-23% and improvement potential over time per management.

Metal Bellows & Hyd-Air -Two Additional Growth Vectors

Metal bellows facility commenced production in January 2025, targeting peak revenues of Rs 85 crore with EBITDA margins of 27-30 as capacity scales from 120,000 to 500,000 pieces per annum. Hyd-Air Engineering has scaled rapidly since acquisition where management has guided peak revenues of Rs 45-50 crore at existing capacity, with a formal expansion announcement pending. Both segments operate largely independently of the core export hose customer base, providing earnings diversification at accretive margin profiles.

Optionality - What the Base Case Does Not Price In

Three optionality vectors are excluded from our base-case estimates. First, international skid exports: the current agreement is India-exclusive, but Aeroflex retains full freedom to pursue international customers post capacity stabilisation. Second, technology adjacency: management has confirmed existing skid assembly machines are directly applicable to EV battery cooling and semiconductor chip cooling structurally large markets accessible without incremental capex. Third, INR depreciation: with 74% of revenues USD-denominated, rupee weakness is a direct EBITDA tailwind, adding meaningful margin benefit requiring no operational change.

Valuation Summary

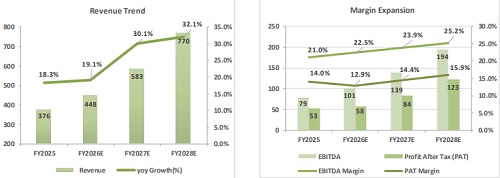

We estimate Revenue/EBITDA/PAT CAGR of 27%/35%/33% over FY25A-FY28E. We Initiate with BUY with a Target Price of Rs 285, based on 45x FY27E EPS implying 16% upside from CMP.

Risks to Our Thesis

* Execution risk: Liquid cooling skid capacity ramp from 2,000 to 15,000 units; automation capex on timeline.

* Policy risk: US tariff escalation or reversal of China+1 export tailwinds; India-EU FTA implementation delay.

* Raw material risk: Nickel/SS price spikes compressing gross margins with 1-2 quarter pass-through lag.

Industry Outlook

Market Size

* The global market for metallic flexible flow solutions and industrial hose assemblies was valued at approximately USD 6.2 billion in 2024 and is forecast to reach USD 10 billion by 2031, growing at a CAGR of 7.2%.

* Global data centre liquid cooling market: estimated ~USD 3 billion currently, growing at ~33% CAGR projected to reach USD 21 billion in 6-7 years.

* India stainless steel market projected to grow from USD 17 billion (FY25) to USD 32 billion (FY35) at 6.2% CAGR.

Oil & Gas - LNG's Infrastructure Buildout as a Demand Engine (USD 1.5 Billion)

The flexible metallic hose and connector sub-segment within global oil & gas is estimated at USD 2.4-2.6 billion (2024), growing at 6.5% CAGR. Demand is driven by LNG terminal buildouts across the Middle East, North America, and Southeast Asia - cumulative LNG infrastructure investment is expected to exceed USD 500 billion through 2035. Each LNG terminal requires thousands of certified high-pressure SS hose assemblies across regasification trains, loading arms, and pump connections. The Middle East & Africa is the fastest-growing sub-region at 7.5% CAGR, underpinned by Saudi Aramco's downstream expansion and East Africa's LNG greenfield programmes.

Data Centre Liquid Cooling - The AI Infrastructure Supercycle (USD 3 Billion to USD 21 Billion)

Legacy server racks ran at 3-5 kW, NVIDIA's H100/H200 clusters run at 40-60 kW, and Blackwell pushes 100-120 kW per rack. Air cooling is no longer viable at these densities. The global data centre liquid cooling market was valued at approx. USD 3 billion in 2024 and is projected to reach USD 21 billion by 2032 at a 33% CAGR, the highest growth rate of any industrial infrastructure segment. Within the value chain, the Component Specialist layer manufacturers of SFN precision piping, flexible hoses, and bellows running directly inside the server white space is the highest-barrier, highest-margin segment, given that a single coolant leak adjacent to a USD 300k AI rack constitutes a catastrophic failure.

Fire Safety & HVAC -Stable Recurring Demand (USD 1.8 Billion Combined)

The certified SS flexible fire hose sub-segment is approximately USD 1.1 billion within a USD 8 billion global fire protection market growing at 6.8% CAGR. The HVAC flexible metallic connector market adds USD 700 million. Both segments offer structural recurring demand every new commercial building, data centre, and industrial facility requires certified fire hose assemblies with mandatory periodic replacement cycles. Low cyclicality and consistent aftermarket demand make these reliable base-load revenue streams for diversified metallic hose manufacturers.

Please refer disclaimer at http://www.aretesecurities.com/

SEBI Regn. No.: INM0000127

Ltd ( 1 ).jpg)