Hold TATA Elxsi Ltd For the Target Rs. 4,900 by Choice Broking Ltd

Assessing Q3 Results amid Trump Tariffs & Macroeconomic Challenges

TELX missed estimates by substantial margins.

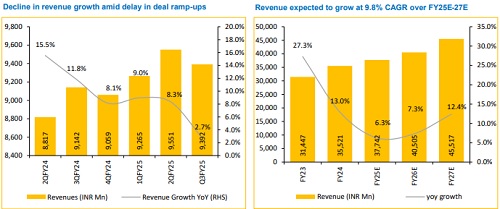

* Revenue for Q3FY25 came at INR 9.3Bn up 2.7% YoY but down 1.7% QoQ (vs CEBPL est. at INR 9.9Bn).

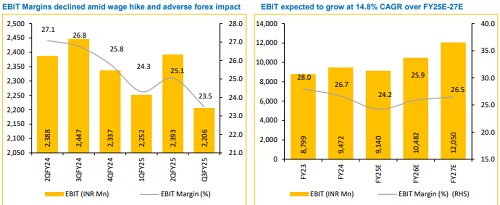

* EBIT for Q3FY25 came at INR 2.2Bn, down 9.8% YoY and 7.8% QoQ (vs CEBPL est. at INR 2.6Bn). EBIT margin was down 327bps YoY and 156bps QoQ to 23.5% (vs CEBPL est. at 26.8%).

* PAT for Q3FY25 stood at INR 1.9Bn, down 3.6% YoY and 13.3% QoQ (vs CEBPL est. at INR 2.2Bn).

Growth Hinges on Transportation Segment Amid Market Struggles:

* TELX’s Q3FY25 performance shows mixed results across its verticals and geographies. Overall growth across segments remained flattish, Transportation business grew 0.5% QoQ in CC, though impacted by weaker automotive demand in Europe & US, & remains the largest revenue contributor at 55%. Media & Communications saw a 0.4% QoQ growth in CC, while Healthcare & Life sciences grew 1.1% QoQ in CC, driven by new customer wins & traction in digital and Gen AI offerings, contributing 11.8% to revenue. Looking ahead, near-term outlook appears weak, primarily due to challenging demand environment in Transportation segment.

* The rise of Chinese EV manufacturers is reshaping the global automotive market, impacting TELX, whose revenue heavily depends on the transportation sector. As Chinese EVs gain market share, Western OEMs in China face declining profitability, prompting them to rethink strategies, cut R&D budgets, and refocus on ICE and hybrid vehicles. This slowdown directly affects TELX’s transportation business, reflected in modest QoQ growth. In response, TELX is diversifying geographically, with strong growth in India, Japan, and emerging markets. Additionally, TELX is investing in innovative solutions such as the AVENIR SDV platform with Qualcomm, expanding into commercial vehicles, avionics, and defense, while utilizing global OEM partnerships to indirectly engage with China. However, we expect these strategic efforts to take time before they largely impact the company’s performance.

Potential slowdown in IT spends amid Trump tariffs poses risk for TELX: TELX may face revenue challenges due to uncertainty over Trump-era tariffs, impacting European auto companies and TELX's revenue. With 30% of revenue from the US and 40% from Europe, any reduction in IT spending or delays in contracts could slow growth. Currency volatility poses margin risks, but stable tariffs may boost demand.

Q3FY25 EBIT margin drops to 23.5%, Plans recovery with improved efficiency and top-line growth: In Q3FY25, TELX reported an EBIT margin of 23.5%, down from 25.1% in Q2FY25 and 26.8% in Q3FY24. The decline was primarily due to adverse currency movements in EUR, GBP, and JPY (140bps impact) and wage hikes (100bps). However, operational efficiency and reduced on-site salary costs partially offset these effects. The attrition rate remained low at 12.4%. TELX aims to return to an EBIT margin of 25-26% through improved top-line growth, better billability, and utilization, following the completion of the wage hike cycle.

View and Valuation:

TELX's performance fell short of expectations, with broad weaknesses across business segments. Healthcare saw slight improvement, but Transportation and Media remained weak. Delayed growth from recent deals hindered progress, with Transportation challenges expected to persist. Media & Communications and Healthcare may contribute more significantly starting H2FY26E. Additionally, the impact of Trump tariffs and increasing competitive pressures from China should be closely monitored. Given these factors, we've reduced our revenue estimates by 12-17%, downgraded our rating to HOLD, and lowered the target price to INR4,900, reflecting a reduced PE multiple of 30x (earlier 46x) due to a weaker outlook compared to peers in our coverage based on FY27E EPS of INR 163.2.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

600-400.jpg)