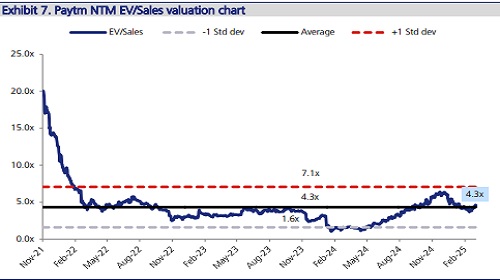

Buy One 97 Communications Ltd For Target Rs. 1,010 By JM Financial Services

Potential regulatory triggers enabling strong optionality

With Paytm working its way up post the disruption last year, we anticipate three potential regulatory triggers over the coming fiscal year – 1) MDR on higher ticket / larger merchants’ UPI payments, 2) Removal of embargo on Paytm Payments Bank, and 3) Grant of PA (Payment Aggregator) /PG (Payment Gateway) license. While even one of these coming to fruition could create significant upside opportunity, timing is trickier to predict. The company has already received a reprieve with NPCI allowing it to onboard UPI customers. With CMP implying 25x FY27E Adj. EBITDA multiple, we find limited downside but upside movement could be sharp and substantial, particularly considering our FY27 EBITDA estimate can rise by c.35% if either of trigger 1 or trigger 2 materialise. Hence, we reiterate BUY with Mar’26 TP of INR 1,010 with potential for sharp upside risks. However, we lower target multiple to 60x FY27E PER, lowered from 70x earlier considering the rising volatility in equity markets.

Trigger 1: Tiered MDR on UPI payments – payments above a threshold or at large merchants

* Strong business case for tiered monetisation via MDR: Pre Jan-2020, 0.30% MDR was applicable on UPI P2M transactions that was reduced to zero to promote digital transactions. With merchant penetration still having headroom to grow in smaller tier cities, we do not expect a blanket MDR implementation on UPI anytime soon. However, there is a strong business case for MDR on higher ticket payments or on payments made at larger merchants as these merchants anyways accept payments from debit / credit cards where MDR is already applicable. This shelters the small merchants while also taking away the burden from the government that needs to fund UPI incentives for the ecosystem. In fact, 0.3% MDR on INR 2,000+ P2M transactions in FY25 can generate INR 140-150bn for the UPI ecosystem (refer exhibit 1), enough to compensate for the expense of maintaining and expanding it, as per PCI.

* Precursors to MDR reactivation emanating recently: There has been rising chatter of MDR since the government announced INR 4.37bn allocation for UPI incentives in FY26, roughly 12% / 29% of FY24/FY25 payment of INR 35bn / 15bn. Industry checks suggest that the dip is a big precursor that government is likely to move away from subsidy to tiered monetisation. Moreover, FY25 UPI incentive circular also noted a couple of firsts (1. demarcation between small and large merchants with incentive only on small merchants, and 2. detailed background on MDR before it was made zero) that suggest that groundwork for MDR is being laid out. There have also been media reports suggesting finance ministry officials being amenable to 25bps MDR on large merchants.

* MDR on UPI can enable 50-100% upgrade to Paytm’s EBITDA estimates: Our estimates have Paytm’s FY26 GMV at INR 23,000 bn. We further estimate c.85% GMV from UPI and 60-70% of UPI GMV being generated from transactions above INR 2,000. Assuming 0.3% MDR on INR 2,000+ transactions, Paytm’s FY26 GMV would generate INR 38bn. Furthermore, we assume Paytm’s share of this MDR to stay similar to FY24 UPI incentive distribution, suggesting c.25% MDR being paid to the company. This calculation suggests Paytm would likely see its FY26 revenue rise by INR 9.5bn. Though the costs of generating this GMV are already there in the income statement, we still believe that the company would spend money on promotional activities to gain market share once monetisation is allowed. Hence, we assume 60% incremental margin on this revenue resulting in INR 5.7bn EBITDA rise, almost doubling JMFe of INR 5.3bn. Similar maths on FY27 numbers suggests EBITDA becoming c.1.5x if MDR comes into play

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361