Pick of the Week : Buy Varun Beverages Ltd for the Target Rs. 500 - Axis Securities Ltd

Why Varun Beverages Ltd

• A Key Global Beverages Player

• Second Largest PepsiCo Franchisee Globally

About the Company VBL is a key global beverage player and PepsiCo’s second-largest franchisee worldwide (ex-US). It operates across 10 countries with distribution rights in four more, with India as the core market, contributing ~90% of PepsiCo’s beverage volumes domestically. The expanding Africa-led international footprint reinforces VBL’s strategic importance within PepsiCo’s global network.

Investment Rational

A. Volume-Led Growth

• In Q4CY25, consolidated volumes rose 10.2% YoY to 237 Mn cases, led by India (+10.5%), followed by international markets (+10%).

• Domestic performance rebounded strongly in Q4, underscoring the strength of VBL’s distribution reach and brand portfolio. Further, the onset of the summer season will act as a strong demand catalyst for VBL.

B. Strategic Capacity Expansion to Drive Future Growth

• VBL continues to strengthen its growth platform through calibrated capacity expansion. Four new greenfield plants have been commissioned in high-growth regions, alongside brownfield additions across key locations to improve scale and logistics efficiency.

• Internationally, the Morocco snacks facility is now fully operational, while the Zimbabwe plant is close to commissioning, supporting portfolio diversification beyond beverages.

C. Beer Pilot Adds a New Growth Lever

• VBL plans to pilot Carlsberg in Southern Africa under an exclusive distribution tie-up, leveraging its existing infrastructure and favourable regulations.

• The low-capex, test-and-learn approach supports portfolio diversification and strengthens presence in key growth markets.

Outlook & Valuation

• VBL remains well positioned to sustain strong growth, supported by the BevCo acquisition in South Africa and DRC, expansion of its snacks business in Africa, deeper rural penetration, and ongoing capacity additions. Further, scaling high-margin brands like Sting and sharpening focus on value-added beverages are expected to drive steady revenue and margin expansion.

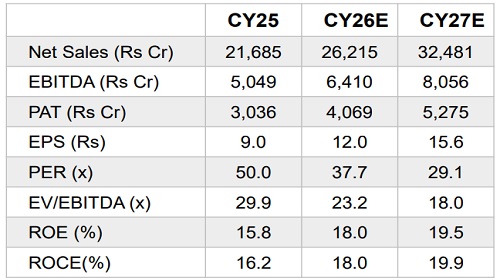

• We expect Revenue/EBITDA/PAT to grow at 19%/20%/26% CAGR over CY24-27E.

Valuation: Trading at 38x Dec’27E EPS3

Analyst Insights

We recommend a BUY with a target price of Rs 500/share, implying an upside of 10% from the CMP

Financial Summary

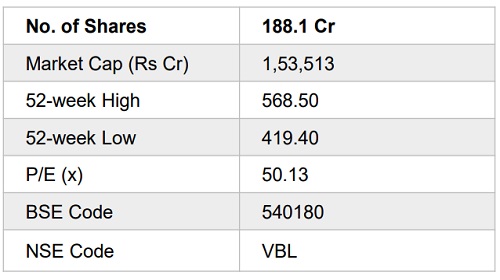

Market Data

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633