Oil & Gas Sector Update : Gulf Crisis – GoI steps in to manage LPG demand-supply by Emkay Global Financial Services Ltd

The LPG situation, owing to the Hormuz shutdown, is perceived to have turned more precarious due to ~55% of the demand being met by direct imports from the Gulf and days of cover being 20-25 generally. Given the halt in ME cargos, the buffer would have reduced to 5-10 days by end-March with potential exhaustion by mid-April had the GoI not intervened. However, the GoI has initiated multiple demand-supply management measures, which we believe are aimed at maintaining the buffer at 20-25 days. The GoI has indicated daily sale of 5mn cylinders which we believe amounts to ~10% curtailment, likely from raising the booking gap to 25-45 days (urban-rural, from 21 earlier), besides the RSP hike of Rs60/cyl. Additionally, diversion of refinery propane-butane streams from petchem to LPG has led to a 28% jump in production so far, implying yield rising from 4.5% in Jan-26 to ~6% now; this can rise to 7%. Per media reports, OMCs are also procuring spot cargos, albeit at a much higher price, while 1mmt of LPG has been secured from the US under a G2G deal; this LPG should be delivered within 35-40 days. The announcement of supplies at 20% of monthly average consumption to C&I LPG users also aligns with the demand-supply balance, which should improve as more volumes come in. Given the criticality of LPG as a key cooking fuel, with ~25% share of PMUY consumers, the GoI’s measures are essential, though reduction in supply of propylene, PP, butadiene, and butanol could impact the plastic, rubber, solvent, coating, and pharma industries. Refineries also tend to lose if incremental LPG is priced at Mar-26 Aramco CP, as margin vs oil is -USD150-200/mt vs +USD350-400/mt for propylene; however, given the supernormal diesel-kero cracks, refineries are net gainers in the current scenario.

60% import dependency and 20-25 days of cover in LPG Indian annual LPG demand of 33-34mmt (8% YoY growth in Apr-Jan ’26) comprises ~85% domestic and ~10% commercial, with the balance 5% bulk, auto, etc. Domestic/import supply share before the ME conflict was ~40%/60%; ~90% of imports were routed via the Strait of Hormuz, with new US contracts supplying 2.2mmtpa from Jan-26. The GoI has stated that other supplying countries include Norway, Canada, Algeria, and Russia. Domestically, of the ~13mmtpa production, ~12mmt comes from refineries, where LPG yield is ~4.5% of crude throughput, while the balance is from the natural gas side, primarily supplied by GAIL through extraction of propane and butane

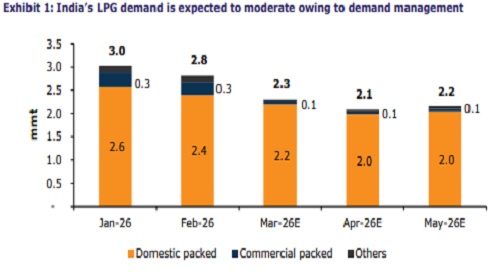

LPG control order and demand-side measures by GoI to manage the situation The GoI, on 9-Mar, directed all refineries to maximize LPG yields and channel the entire propane-butane stream output (including propylene, butene) solely to PSU OMCs, for domestic LPG. This has led to 28% rise in domestic output so far, implying ~6% yield. We estimate ~7.5mmtpa of total petchem conversion to LPG which could take the yield to 7%. On the demand front, the GoI raised price of a domestic cylinder by Rs60 wef 7- Mar, while also increasing the minimum booking gap from 21 to 25/45 days for urban/rural users. The booking-to-delivery cycle remains at 2.5 days, but per our checks, there could be a few days’ delay due to spurt in panic-booking. Supplies to C&I had been stopped, with a committee being set up for reviewing allocation; but this was followed by 20% normal allocation, which we believe is because there is already fall in demand (5mn domestic cylinders delivered daily vs ~6mn in Jan-26). GoI has also taken steps to raise supply (and usage) of kerosene, FO, and other fuels to domestic and C&I customers

International spot propane prices jump to >USD800/mt vs Saudi CP of USD545 While the Saudi CP on a monthly basis stands at USD545/mt for March and the Argus April swaps are at ~USD570 (possibly due to the Gulf illiquidity), media articles have cited that Indian spot prices jumped to USD800-850/mt. US propane, however, still seems to be priced at under USD600/mt (cif); going ahead, it can provide some respite as more volume comes in. Following the Rs60/cyl RSP hike, LPG losses for OMCs are at Rs74, though they increase to almost Rs500 for spot cargo, with the rupee weakening further; hence, the OMC under-recovery scenario is uncertain and would depend on Aramco-Sonatrach CP for April, besides US propane and Asian spot prices. Commercial LPG prices were also increased, by 7% on 7-Mar, with Delhi rate at Rs1,883/cyl, while auto LPG prices were raised by Rs5-6/ltr on 11-Mar, with Kolkata rate at Rs62.7/ltr.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

Pharma Sector Update : Pharmaceuticals Pharma Weekly ? ICYMI by Emkay Global Financial Servi...