India Strategy : Equities recovery on peace deal by Emkay Global Financial Services Ltd

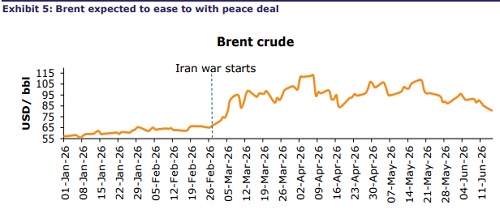

Nifty rallied +2% and Brent eased -4% as the US and Iran agreed on a peace deal, set to be signed on Friday, 19-Jun-26. We see crude settling at USD75- 80/bbl, and this is unambiguously positive for India on external account, domestic liquidity, and supply chain easing. We maintain our FY27 Nifty target at 29,000 and see a strong rally sustaining in the short term. Our bullishness is supported by strong earnings, with FY27E Nifty EPSg at 15.7% and moderate valuations at ~17.8x PER (1YF). OMCs, transportation, cement, and select lenders (banks/NBFCs) are the best ways to play the recovery.

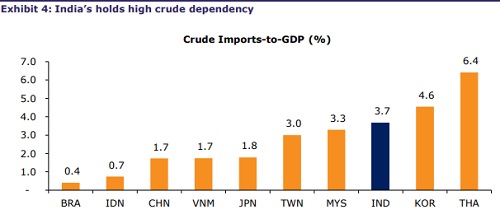

Macro boon for India

The US and Iran agreed on a deal to end the war in the Middle East, with the Strait of Hormuz set to re-open on Friday, 19-Jun-26. This has a three-fold macro benefit for India. First, Brent should settle at USD75-80/bbl vs an average of USD103/bbl in AprMay-26. This delivers a proforma benefit of 64% on the CAD. Second, it addresses supply chain bottlenecks and potential RM shortage worries across multiple sectors and averts a potential inflation shock. Third, the relief on the external account translates to improved domestic liquidity, which should help interest rate transmission. We expect a multi-asset rally: Rs93/USD, the 10-year gilt to 6.75%, and the 12M T-bill to 5.5%. We expect the consumption cycle to be a standout beneficiary, continuing the upward momentum from Q4CY25 after GST cuts kicked in.

Earnings outlook – set for a strong FY27

India earnings held up strongly through the crisis, with a strong 4QFY26 (Nifty PATg: +4%), despite the energy shock and commodity inflation pressures. Some residual impact could still flow through in Q1FY27, but there is no apparent instability in earnings momentum. With energy prices normalizing, FY27 forecasts (Nifty EPSg: +16%) stay on course for the best year in three. Financials and consumption drive this recovery, and the end of the war is a positive for both sectors. Broader market estimates are also positive – the share of companies in our consensus universe delivering >25% EPSg rises from 31% in FY26 to 41% in FY27. The share of companies with >5% EPS downgrades (FY27) is a minuscule 29% (from 1-Apr-26).

We maintain our Mar-27 Nifty target of 29,000

Valuing the market at 19.6x PER (1YF), ~LTA. The recent correction (Nifty down 7% since 28-Feb-26) has normalized valuations for the broader market. The Nifty trades at 17.8x 1YF PER, below its past 5Y LTA of 19.6x. Breadth is supportive too, with 48% of the consensus universe below LTA mean (28% below -1SD). FY27E EPSg of 15.7% suggests strong earnings recovery, subject to slight near-term risks from the oil shock and the effects of the ME crisis.

Play through consumption

The immediate beneficiaries are OMCs, transportation, cement, and select lenders (banks/NBFCs), along with ME-exposed stocks like L&T. Conversely, the case for upstream energy is now weak, as with safe haven sectors like FMCG, pharma, and technology. Our top ideas to play the market recovery: OMCs

Key risks

First, the deal gets inked on Friday, 19-Jun-26, so it is still a high probability, but not a certainty – given the number of false dawns during the ceasefire, any disruption would send oil spiking and reverse our entire thesis. Second, the entire region is on a knife’s edge, and flare-ups could recur even after the deal is signed. Third, the damage to oil infra is still not clear – there may be a negative surprise on timelines for supply normalization (though we think the oil market is pricing in 3-6M delays). We see low probabilities of these risks crystallizing, and are working of our base case of the SoH fully reopening on Friday and oil receding to USD75-80.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354