ECOSCOPE : India CPI Jun'26: CPI above 4%; food inflation key by Motilal Oswal Financial Services Ltd

India CPI Jun’26: CPI above 4%; food inflation key

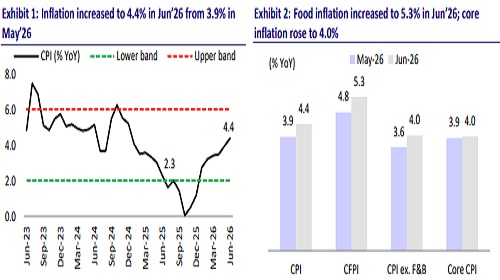

* India's CPI inflation accelerated to 4.4% YoY in Jun'26 from 3.9% in May'26 (slightly lower than our expectations of 4.5%), marking the first breach of the RBI's 4% target in nearly 18 months. The increase was primarily driven by higher food prices and the gradual pass-through of war-induced increases in global energy prices and transportation costs. Despite the June uptick, average CPI inflation during 1QFY27 stood at 3.9%, well below the RBI's forecast of 4.2%.

* Food inflation increased to 5.3% in Jun'26 from 4.8% in May'26, remaining the largest contributor to headline inflation. The acceleration was led by vegetables, spices, and edible oils. Ginger inflation surged to 50.4% YoY in Jun’26 from 32.5% in May’26, while tomato inflation remained elevated at 31.9% YoY, despite moderating from the previous month. Inflation also remained firm in edible oils, fruits, and processed food items, whereas continued deflation in potatoes and peas partly offset the increase. Going forward, uneven monsoon distribution and lower sowing of pulses and oilseeds could keep food inflation elevated over the coming quarters.

* The impact of the West Asia conflict is now becoming increasingly visible in domestic inflation. Higher global crude oil prices, elevated freight costs, and supply chain disruptions have started feeding into transportation and services prices. Transport inflation accelerated further to 4.3% YoY in Jun'26 from 1.8% in May'26, while restaurant and accommodation service inflation increased to 6.9% YoY in Jun’26 from 5.7% in May’26, reflecting the pass-through of higher fuel and commercial LPG prices.

* Headline core CPI inflation (excluding food and fuel) edged up marginally to 4.0% YoY in Jun'26 from 3.9% in May’26. Besides transport and hospitality, inflation also strengthened across several demand-sensitive categories, with education services rising to 3.3% in Jun’26 from 2.9% in May’26 and clothing & footwear to 3.2% from 3.0%. Meanwhile, personal care, social protection, and miscellaneous goods & services inflation remained elevated at 16.7% in Jun’26, largely due to persistently high gold and silver prices.

* Going forward, food inflation is likely to remain the key upside risk to headline CPI, even as fuel-related pressures moderate. Following the war-led spike, Brent crude has eased to the USD 76-80/bbl range, reducing the likelihood of further retail petrol and diesel price hikes. However, the agricultural outlook has weakened, with cumulative monsoon rainfall 18% below the LPA (as of 12th July) and kharif sowing down 16.0% YoY, led by sharp declines in pulses (-23.3%), oilseeds (-21.0%), coarse cereals (-22.5%), and rice (-8.6%). Unless rainfall improves materially over the coming weeks, food inflation is likely to remain elevated during the second half of FY27.

* Rural inflation continued to outpace urban inflation, with CPI inflation at 4.7% YoY in Jun'26 versus 3.9% in urban areas, reflecting greater food price pressures. Persistently high food inflation, coupled with delayed monsoon progress, could weigh on rural purchasing power and discretionary consumption. Nevertheless, with average CPI inflation at 3.9% in 1QFY27, below the RBI's 4.2% forecast, we expect the MPC to remain on hold through CY26, with the next policy rate hike more likely in 2027, contingent on food inflation and monsoon conditions. We peg CPI inflation at 5.2% in FY27, 10bp higher than RBI’s forecast of 5.1%.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412