The Strait of Hormuz May Reopen, but the World Economy Won't Go Back to Normal: Vallum Capital

Markets have a dangerous habit of confusing the resolution of a crisis with the reversal of its consequences. Brent crude has round-tripped from $78 to $120 and back to $79. The instinct is to declare the episode over. It is not.

According to the latest report by Vallum Capital, The oil price is the most visible, most politically managed, and therefore most misleading indicator of what the Hormuz closure has actually done to the global cost structure. The damage is not in the commodity. It is in the system that moves, insures, stores, and reroutes it, and that system does not snap back.

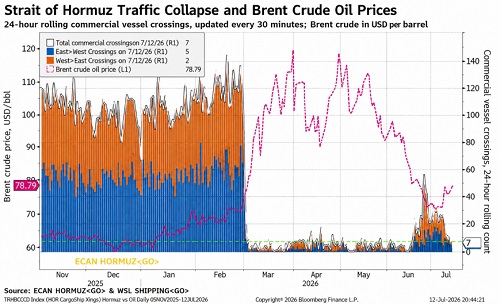

What the Chart Tells You

Pre-crisis, 100 to 120 commercial vessels transited the Strait daily. On July 12, 2026, that number was seven. Yet Brent sits at $78.79, exactly where it started. The oil price says the crisis is over. The shipping data says it has barely begun. This single divergence tells you that what markets are treating as a resolved shock is, in reality, a structural repricing still in progress.

Why the Cost Structure Won't Reverse

Every major supply disruption breeds inflation that outlasts the event itself. The mechanism is sequential and each stage operates on a longer lag than the one before it.

Freight reprices first. Every tanker rerouted around the Cape adds 3,500 nautical miles and 10 to 14 extra sailing days. hundreds of thousands of containers remain stranded across Indian, Omani, and Pakistani ports. The Breakwave Tanker Shipping ETF (BWET) is up over 700% year to date. The dry bulk ETF (BDRY) is up 107% over one year. These are not oil plays. They measure how much more expensive it has become to move anything by sea, and they have not retreated even as crude has.

Insurance reprices next, on 12 to 18 month cycles. War-risk premiums for the Persian Gulf are running at roughly eight times pre-crisis levels. As Tufton's managing director noted, referencing the Red Sea precedent: "As long as there's a threat of an attack, that's enough. You don't actually need the attack.

Then the real economy absorbs the hit, and this is where the lag is longest. The Dallas Federal Reserve's own modelling shows that the inflation impact of higher shipping costs is "most visible in the final quarter of 2026, rather than at the time of the shock," because input costs work through production chains gradually, not immediately. The data confirms this is already underway. US headline CPI accelerated to 4.2% in May 2026, its highest since April 2023, with energy costs surging 23.5% year on year. Core inflation climbed to 2.9%, a new high since September 2025, confirming that the shock is now bleeding beyond energy into broader prices. Core PCE hit 3.4% in May, and markets are pricing a 65% probability that the Fed will need to raise rates by September, not cut them.

History says this passthrough takes years, not months. After the 1973 oil embargo, US CPI rose above 12% and did not retreat until March 1975, eighteen months after the shock. The 1979 Iran revolution sent CPI above 13%, and the economy endured back-to-back recessions through 1982. Even the shorter 1990 Gulf War spike, which lasted only two months in oil markets, still produced a recession that ran from July 1990 to March 1991.

The Suez Precedent Settles It

After Houthi attacks on Red Sea shipping ended in late 2025, Suez Canal transits were still around 60% below 2023 levels months later. Ships kept sailing the Cape of Good Hope because rerouted networks, repriced insurance, and redeployed fleets develop their own inertia. Trade routes, once rerouted under duress, stay rerouted. The post-2022 Russia sanctions tell the same story: European gas costs never returned to pre-war levels. The pipes were not just turned off. They were blown up. The system rebuilt itself around the new reality.

The Strait of Hormuz will almost certainly reopen. The global cost structure that existed before February 28, 2026 will not return with it anytime sooner or later.

Above views are of the author and not of the website kindly read disclaimer

.jpg)