India Strategy : Energy shock hit, but strong underlying trends by Emkay Global Financial Services Ltd

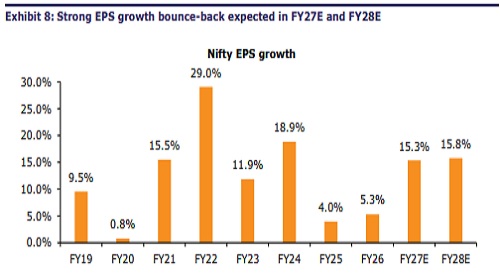

Q1FY27E should be understandably soft, with average Brent at $97/bbl and supply tightness across multiple sectors. The good news is that demand remained strong, with revenue growth across staples/discretionary at 10%/51% yoy, showing little signs of fatigue. We see little risk to the FY27E Nifty EPSg forecast of 15%, with demand remaining strong and some margin tailwinds kicking in from 2QFY27E onwards. The two-year time correction has taken Nifty PE to 18.9x, 3.5% below 5Y LTA, and we remain constructive on Indian equities. We maintain our Mar-27 Nifty forecast at 29,000, implying a 1YF PE at 20.9x, close to LTA. We prefer discretionary (including autos), industrials, and are UW on BFSI.

Q1FY27 results summary

We expect weak Nifty PATg at 8.6% yoy, vs 5.2% in 4QFY25. Topline growth (excluding BFSI) decelerates to 9.5% from 13.6%, despite the pickup in inflation, but EBITDA margins improve by 230bp qoq to 20.3%. PATg for Emkay coverage (excluding OMCs) is stronger at 16.2%. Excluding OMC/BFSI, topline growth is expected at 22.9% yoy, while EBITDA margin at 17.4%. The headline PATg (Emkay universe) for FY27E is at (-12.7%), as OMC under-recoveries should drive a collective loss of Rs686bn. The 10% weighted Nifty EPSg for 1QFY27E is slightly behind the annual forecast of 15%, but we recognize that there was some pressure from the energy shock, which should recede in the latter part of FY27. We do not see this as a cause for worry

Earnings recovery on track

We see little risk to the FY27E Nifty EPSg forecast of 15%, with demand remaining strong and some margin tailwinds kicking in from 2QFY27E onwards. The earnings recovery (FY24-FY26 CAGR: 6%) is aided by a broad macro revival. We expect consumption demand to remain strong on the back of multiple stimuli through CY25—GST cuts, 125bp of rate cuts by the RBI, and income tax cuts in Feb-25 and GOI capex/GDP remains resilient, though state and corporate capex is sluggish. Broader earnings forecasts also indicate a revival—the share of companies with +25% EPSg is expected to rise from 31% in FY26 to 43% in FY27 (based on the consensus universe of 500+ companies with 5+ analyst coverage). Discretionary, industrials, and materials are leading the earnings recovery. Energy is expected to report poor headline numbers because of the OMC losses.

Discretionary and metals lead the pack

Telecom, discretionary (excluding auto), and metals are the leading sectors in the Emkay coverage universe, with +35% PATg forecasts. Materials (excluding metals), pharma, and industrials are the laggards, with negative growth. Financials are set to post another strong quarter, with expected PATg at 18% (banks 19% and NBFCs 17%). Technology is also expected to post 12%, with currency-assisted margin tailwinds. Staples PATg is expected to be weak at 1.6% despite strong volume growth, with margin declines for ITC, Emami, and Colgate being the key drag. Excluding OMCs, mid-caps led the pack, posting a robust 33% PAT growth alongside 17.2% EBITDA growth, reflecting strong operating leverage. Small caps lagged materially, with adjusted PAT growth stuck in single digits.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354