Private Insurers Drive Life Insurance New Business Premium Growth in Q1FY27 CareEdge Ratings

Overview

India's life insurance industry reported a strong start to FY27, with New Business Premiums (NBP) increasing 16.6% year-on-year (y-o-y) in Q1FY27, reflecting sustained demand across both retail and group segments. Growth was primarily driven by private insurers, whose premium collections expanded significantly, supported by continued traction in retail products and a recovery in group business. Consequently, private insurers further strengthened their market share to nearly 40%, although LIC continued to account for the majority of industry premiums. Industry Annualised Premium Equivalent (APE) also maintained strong momentum in Q1FY27, rising 23.4% y-o-y. Growth was led by private insurers, whose APE increased 27.6% y-o-y, while LIC recorded a healthy 16.8% increase.

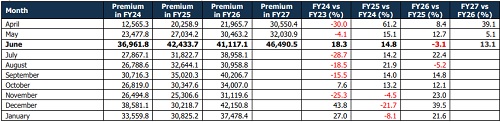

On a monthly basis, industry NBP increased 13.1% y-o-y to Rs 46,490.5 crore in June 2026, reversing the 3.1% contraction recorded in the corresponding month last year. The improvement was led by a robust 36.8% y-o-y increase in private insurers' premiums, supported by a recovery in group business and sustained growth in individual non-single products. In comparison, LIC recorded a modest 1.2% y-o-y increase. Industry APE grew 27.7% y-o-y in June 2026, supported by broad-based growth across both private insurers (29.0% y-o-y) and LIC (25.6% y-o-y), indicating continued strength in regular-premium business.

Figure 1: Movement in New Business Premium (Rs crore

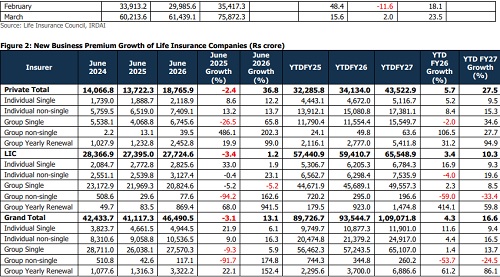

Figure 2: New Business Premium Growth of Life Insurance Companies (Rs crore)

recovery, with NBP rising 13.1% y-o-y to Rs 46,490.5 crore, reversing the 3.1% contraction recorded in the corresponding month last year. The recovery was driven primarily by private insurers, which reported a robust 36.8% y-o-y increase in premiums, significantly outpacing LIC's 1.2% growth. As a result, the private sector's share of industry NBP increased to nearly 40%, up from 36.5% a year ago, although LIC continues to dominate, accounting for around 60% of the market. The overall improvement in industry premiums was supported by private insurers, which recorded a sharp 65.8% y-o-y growth in group single premiums, more than offsetting the 5.2% decline in LIC's group single business and enabling the overall group single segment to return to growth. The group's yearly renewal segment also registered strong growth of 152.4% y-o-y, aided by favourable base effects and higher renewal collections, albeit from a relatively low base. Meanwhile, healthy growth in retail segments, particularly individual non-single premiums, continued to reflect sustained demand for protection and longterm savings products.

Going forward, continued expansion in digital and diversified distribution channels, alongside improving traction in protection and annuity products, and a gradual recovery in group business, are expected to support premium growth. However, any regulatory changes governing bancassurance may lead to a more cautious approach to the channel, prompting insurers to further strengthen their agency franchise and diversify their distribution. The government planned cooperative life insurance company could further improve insurance penetration by leveraging the extensive cooperative network to expand access in underserved and rural markets, while increasing competitive intensity and improving affordability over the medium term. However, the overall pace of expansion is likely to remain influenced by product mix, competitive intensity, interest rate environment and global macroeconomic developments. In contrast, LIC's ability to revive growth in its group portfolio will remain an important monitorable.

Figure 3: Movement in Premium Type of Life Insurance Companies (Rs crore)

Single-premium business increased by 5.9% y-o-y in June 2026, recovering from the 5.6% contraction recorded in the corresponding month last year. The growth was primarily supported by the recovery in private insurers' group single business, although the overall pace remained moderate due to the decline in LIC's group single premiums. In contrast, non-single premiums recorded a sharp 34.2% y-o-y increase, reflecting sustained traction in regular-premium retail products, higher renewal collections and continued demand for long-term protection and savings-oriented products. The stronger growth in non-single premiums also indicates an improving product mix towards recurring premium policies, which provide greater persistency and visibility of future cash flows for insurers. On a YTDFY27 basis, single premiums grew by 13.0% y-o-y, while non-single premiums expanded by a stronger 26.1%. Going forward, steady growth and sustained momentumare expected to remain resilient; meanwhile, the performance of the single-premium segment is likely to remain contingent on institutional business flows and the pace of recovery in group policies.

Figure 4: Movement in Premium Type of Life Insurance Companies (Rs crore)

New business premiums across both individual and group segments remained healthy in June 2026, increasing by 12.8% and 13.2% y-o-y, respectively. Growth in the individual segment continued to be supported by healthy demand for retail protection and savings products. Meanwhile, the growth in the group segment normalised from the contraction witnessed in the corresponding period last year, driven primarily by a strong recovery in private insurers' group single business, which more than offset the continued moderation in LIC's group single premiums. Despite the recovery, the group segment continued to account for nearly twothirds of total new business premiums, highlighting the continued importance of institutional business in the industry's premium mix. On a YTDFY27 basis, group premiums increased by 17.9% y-o-y, outpacing the 14.1% growth recorded in the individual segment. Going forward, continued expansion in group protection products and expanding networks are expected to support balanced growth across both segments.

Figure 5: Movement in Individual Non-Single Policies of Life Insurance Companies (in lakh)

Individual non-single policy volumes increased by 7.3% y-o-y to 21.5 lakh policies in June 2026, normalising from the 7.9% contraction recorded in the corresponding month last year. Growth was led by private insurers, whose policy volumes expanded by 11.4%, supported by sustained demand for retail protection and long-term savings products. LIC also returned to positive territory, with policy volumes rising 4.8% y-o-y, indicating an improvement in its retail business. On a YTDFY27 basis, individual non-single policy volumes grew by 6.1% y-o-y to 51.1 lakh policies.

Figure 6: Movement in APE of Life insurance companies (Rs crore)

Industry APE increased by 27.7% y-o-y in June 2026, compared with 2.5% growth in the corresponding month last year. Growth was broad-based, with private insurers and LIC recording APE growth of 29.0% and 25.6%, respectively, supported by healthy growth in regular-premium business. On a YTDFY27 basis, industry APE rose by 23.4% y-o-y. Private insurers continued to lead with 27.6% growth, while LIC recorded 16.8% increase. Going forward, steady demand for protection and savings products, along with continued expansion in distribution channels, is expected to support APE growth.

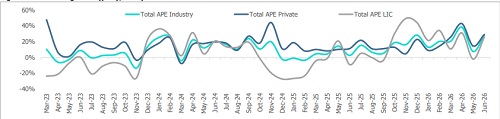

Figure 7: Total APE growth (y-o-y, in %)

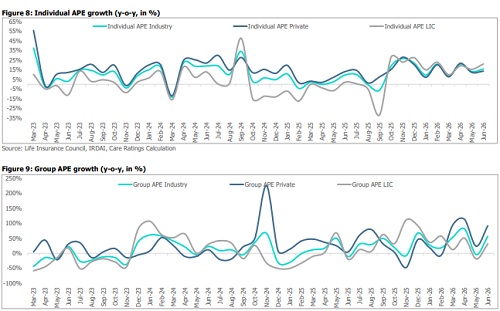

Figure 8: Individual APE growth (y-o-y, in %)

Conclusion

India's life insurance industry maintained healthy momentum during Q1FY27, with new business premiums increasing 16.6% y-o-y. Within this, June 2026 recorded a broad-based improvement, with new business premiums rising 13.1% y-o-y to Rs 46,490.5 crore, reversing the contraction witnessed in the corresponding month last year. Growth was driven by strong performance from private insurers, recovery in group business, and sustained demand for retail protection and long-term savings products, as reflected in healthy growth in individual non-single premiums, policy volumes and APE. While LIC continued to dominate the market, private insurers further strengthened their market share, supported by expanding distribution networks and product innovation. Going forward, the industry's growth is expected to remain supported by increasing insurance awareness, deeper penetration through digital, agency and bancassurance channels, and continued demand for protection, savings and annuity products. The govt. A planned cooperative life insurance company could further deepen insurance penetration by leveraging the cooperative ecosystem to expand coverage in rural and underserved markets, supporting the sector's medium-term growth. While the removal of GST-related input tax credits may put pressure on insurers' profitability, the growing focus on higher-margin protection and nonparticipating products is expected to offset this impact partly. Additionally, increasing participation by private insurers in the group single business segment is likely to intensify competition. The pace of growth will also be influenced by evolving interest-rate expectations, financial market volatility stemming from global geopolitical developments, and the performance of the group's business. Overall, we expect the life insurance industry to maintain a healthy medium-term growth trajectory of 8%–11%

Above views are of the author and not of the website kindly read disclaimer