Q1FY27 Retail Securitisation at Rs 59,000 Cr; Off to a Stable Start by CareEdge Ratings

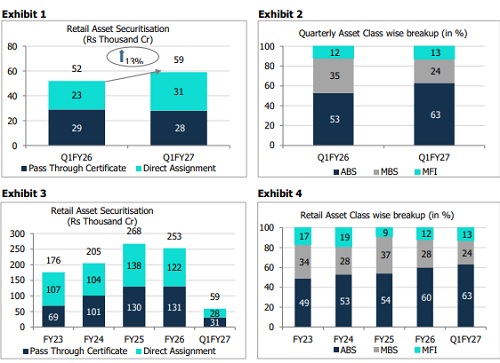

The retail asset securitisation market remained resilient during Q1FY27, recording total transaction volumes of approximately Rs 59,000 crore (Refer to Exhibit 1) across pass-through certificate (PTC) issuances and direct assignment (DA) transactions. This represents a robust year-on-year growth of around 13%, reflecting sustained momentum in market activity. The continued traction in the securitisation space underscores the sector’s inherent strength, driven by healthy credit demand, sustained investor appetite, and originators' ongoing focus on diversifying funding avenues.

Banks continued to be the dominant investors in the securitisation market during the quarter, accounting for well over 80% of total market volume. This included investments from the public and private sectors, as well as foreign banks. Other participants in the market included large NBFCs, alternative investment funds (AIFs), mutual funds, insurance companies, high-net-worth individuals (HNIs), and family offices

Q1FY27 witnessed a notable shift in the composition of securitisation transactions. Gold loan emerged as a key asset class, contributing nearly 33% of the total direct assignment (DA) volumes, while Mortgage-Backed Securitisation (MBS) transactions accounted for around 40% of the overall market. At the same time, the share of vehicle loan-backed PTC transactions declined significantly, largely due to the absence of one of the largest NBFCs from the securitisation market.

The changing asset mix also influenced the preferred mode of securitisation. (Refer to Exhibit 1) DA transactions accounted for approximately 52% (compared to 44% in Q1FY26) of the total transaction volume, slightly surpassing PTC transactions, which contributed the remaining 48% (compared to 56% in Q1FY26).

ABS and MBS Trends in Retail Securitisation

Asset-backed securitisation (ABS) pools constituted a substantial portion of the total overall volumes, contributing around 63% (compared to 53% in Q1FY26) of the total issuances (Refer Exhibit 2). Meanwhile, the share of Mortgage-backed securitisation (MBS) transactions was at around 24% (compared to 35% in Q1FY26), and the share of Microfinance Institution (MFI) loans constituted around 13% (compared to 12% in Q1FY26) of the overall volumes. ABS have now become the dominant asset class in the DA space as well, marking a notable shift from the trend seen in previous years. Notably, the contribution of gold loans has reached levels comparable to that of vehicle loans in the overall securitisation market.

Meanwhile, the microfinance sector showed signs of stability. Supported by improving industry conditions and sustained demand for priority-sector lending assets, MFI backed pools accounted for 17% of total PTC issuances in Q1FY27, up from 15% in the corresponding quarter of the previous year (Refer Exhibit 5).

Outlook

The retail asset securitisation market is expected to maintain steady growth in FY27, supported by strong Q1FY27 volumes of Rs 59,000 crore. The trend reflects NBFCs' continued reliance on securitisation to meet funding requirements amid sustained credit demand and healthy investor appetite. Gold loan financiers have been key contributors, particularly through the DA route, while improving investor confidence and stable pool performance has boosted the share of microfinance-backed PTC issuances. Although vehicle loans were the dominant asset class in previous years, the growing contribution of gold loans and unsecured loans highlights the market’s increasing diversification. The evolving asset mix reflects the market's ability to cater to originators' changing funding requirements while providing investors with access to a broader range of retail asset classes.

The potential economic impact of the West Asia crisis and El Nino remains uncertain. Any adverse development could have a knock-on effect on inflation and, in turn, on credit growth. Assuming these factors do not materially worsen, CareEdge Ratings expects volumes in FY27 to reach approximately Rs 2.60 trillion

Above views are of the author and not of the website kindly read disclaimer