Strategy : Margin Recovery Ahead, Geopolitics Caps Upside by Elara Capital

Despite fresh escalation between US & Iran, we believe that the peak conflict is behind us and thus do not see commodity prices scaling back to previous highs. Bloomberg Commodity Index is 10% below its previous peak, although up 6.6% vs. recent lows. If commodities remain in the current range, it should help to bolster manufacturing operating margins by Q3FY27E. Gradually easing global risks amid domestic resilience should prompt capital rotation away from globally sensitive sectors towards more resilient, structural domestic themes, such as manufacturing, power and consumer discretionary. Inflation risks in India are not yet broad-based, thus obviating the need for aggressive rate hike. This backdrop is likely to also favour financials.

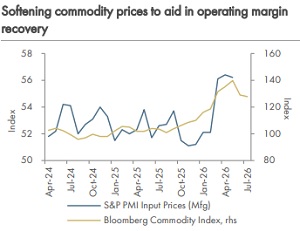

Peak conflict is behind us; sharp uptick in commodity prices unlikely:

Notwithstanding the recent risk of re-escalation of conflict, the correction in commodity prices has been encouraging. India’s crude basket has fallen 51% from its peak (USD 157 on 23rd March 2026) -- the largest price drawdown outside the COVID-19 shock since CY12. Contributing factors include China’s continued cuts to refinery throughput and use of commercial inventory along with the sale of Iranian crude (now uncertain), which together have triggered a rapid decline in crude oil prices. The Bloomberg Commodity index has declined 11.2% (as of 13 th July) from post conflict peak indicating moderating input costs. At current commodity prices levels, our analysis shows manufacturing sector operating margin could recover by ~90-100bp by end-Q3FY27E. Robust domestic demand is providing a further fillip. As such, the reversal in commodity prices is likely to lead to margin expansion with limited pass through to consumers

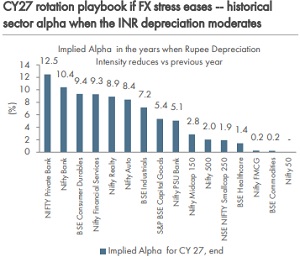

INR weakness tailwinds to flow:

Our analysis shows that across 65 Nifty50 earnings quarters since CY09, the INR depreciation of >5% led to 16% sales growth vs 9% in modestdepreciation years. The Nifty50 FX sensitivity analysis shows weak INR beneficiaries are not simply the highest exporters, but companies where currency gains flow through P&L after hedges, imported cost, and FX liabilities. We see two set of beneficiaries: exports-led beneficiaries: pharma, CDMO, IT services, textiles, upstream & refiners; realization- and pricing-led beneficiaries: steel, aluminium, and automobiles.

FPI equity inflows begin but robust surge unlikely in FY27:

After equity selling of USD 29.5bn since the onset of the US-Iran conflict, FPI invested ~USD 3.3bn since mid-June 2026 till 13 th July. While correction in India’s valuation premium vs the MSCI EM (1.30x in June 2026 vs 1.73x in June 2025) and the recent AI-led, sell off in Asia is bringing India equities into reckoning, we do not see a sharp surge in FPI inflows until a meaningful recovery in earnings unfolds (likely by Q3FY27). Further, any crack in the US AI bubble is unlikely to yield into immediate flows. History of financial bubble bursts (GFC & Dotcom) shows flows congregate in US treasuries after every crisis and it takes ~3-4 quarters before a meaningful pick up in equity flows to EMs unfolds. Moreover, a hawkish Fed and surge in dollar asset trade globally amid DXY near 52w high are emerging as headwinds.

Market breath set to outperform; SMID rally has more wings:

In Q1FY27, while the Nifty clocked in returns of 7.2%, the NSE Midcap 150 and the NSE SmallCap 250 rose by 16.7% and 23.3%, respectively. Three factors would continue to drive this outperformance: a reflation trade, easing geopolitical tensions, comfortable valuation, and structural & policy tailwinds, such as free trade agreements (FTA), the INR depreciation-led exports competitiveness, and setting up of new supply chains where small- and mid-size firms will likely see opportunities as vendors, component suppliers, and assemblers. E.g. small caps in newly developed sectors saw their share in the small-cap PAT pool increase in the past decade (0.5% in 2016 to 1.0% in 2026 for defence, 3.3% to 4.5% for electronics). With improving earnings breadth, visible ROE convergence and policy tailwinds, incremental risk-reward sits more favourably in SMID stocks vs. a defensive large cap value play

Please refer disclaimer at Report

SEBI Registration number is INH000000933