India monsoon tracker Research Report by Emkay Global Financial Services

Prolonged weak monsoon disrupts sowing activity

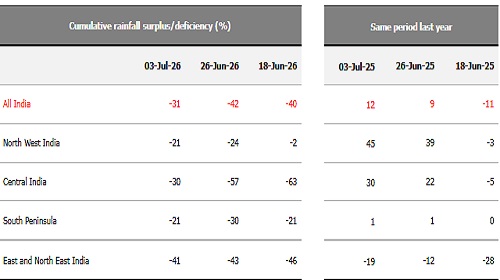

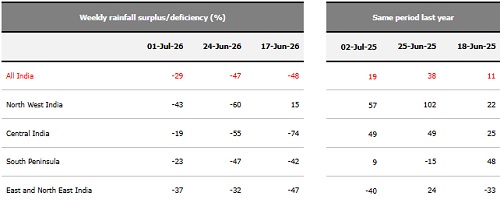

* Rainfall remains weak despite some improvement Cumulative rainfall as on 3-Jul-26 was 31% below the long-period average (LPA) as the monsoon stayed weak, albeit with some improvement over the previous week. Weekly rainfall (as on 1-Jul-26) was also poor, at 29% below LPA. Rainfall deficiency has been geographically spread out: North and West India (-21%), Central India (-30%), Southern Peninsula (-21%), and East and North East India (-41%) have all seen heavily deficient rains so far. Jun-26 ended with rainfall 40% lower than LPA, making it the worst June month for rainfall in the last decade. With the IMD expecting Jul-26 rainfall to be below normal (<94% of LPA), concerns around the monsoon and the Kharif sowing season remain elevated.

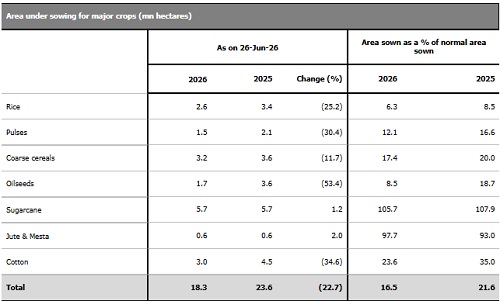

* leading to a sharp decline in sowing activity: Kharif sowing activity has now collapsed as the monsoon remains weak. Total area under sowing as on 26-Jun-26 (18mnha) was 23% lower than that last year. This has been due to much lower sowing for most major food crops – rice (2.6mnha; -25% YoY), pulses (1.5mnha; -30% YoY), coarse cereals (3.2mnha; -12% YoY), and oilseeds (1.7mnha; -53% YoY). Among non-food crops, cotton sowing (3mnha; -35% YoY) remains a concern. Overall area under sowing is at 17% of normal area sown, compared with 22% at the same point in 2025. With the July month typically accounting for 60-80% of total Kharif sowing, an improvement in monsoon activity is crucial for food production outlook.

* Food price inflation remains contained: Average weekly change in retail prices for vegetables (1.5%) and eggs (1%) was relatively high, while cereals (0.5%), spices (0.4%), pulses (0.2%), oils and fats (0.2%), and milk (0.1%) saw modest price increases. On an annual basis, average prices for oils and fats (11%) remain sharply higher, while those for eggs (6%), vegetables (3%), milk (3%), spices (3%), cereals (2%), and pulses (1%) have had more modest increases. Continued deficient monsoons over key food-producing states such as Maharashtra, Gujarat, Madhya Pradesh, and Uttar Pradesh, among others, could imperil food supplies and put upward pressure on prices in the coming weeks.

* Reservoir levels remain under pressure: Overall basin-wise reservoir levels are heavily depleted, and well below last year’s levels. As of 2-Jul-26, pan-India reservoir levels are at just 26% of capacity and 39% lower than over the same period last year. Central India has the highest capacity (32%), followed by North India (29%) and West India (28%). Storage levels are significantly low in South India (20%) and East India (19%).

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354