ECOSCOPE : Fiscal monthly: Center maintains strong capex growth by Motilal Oswal Financial Services Ltd

Key takeaway:

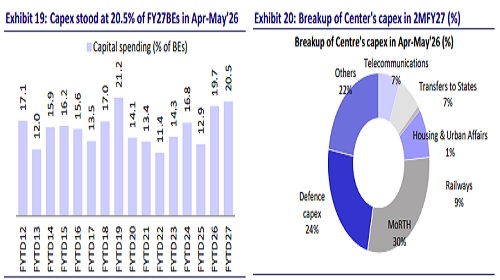

* Cumulative capital expenditure of the central govt. remained strong, rising 13.4% YoY during Apr–May FY27 despite the sharp increase in subsidy spending arising from the West Asia conflict. Importantly, the composition of spending was encouraging, with railway capex and capital transfers to states recording robust growth, while road sector spending remained relatively muted and defense capital expenditure contracted.

* Moreover, the current capex run rate of around INR1.3t per month remains comfortably above the INR1.0t monthly pace required to meet the FY27 Budget target, indicating that the government's infrastructure spending remains well ahead of schedule. The key takeaway is that the government has accommodated the temporary rise in revenue expenditure without compromising its infrastructure-led investment strategy, preserving the quality of expenditure even amid elevated geopolitical and commodity price uncertainties.

Outlook:

* We continue to expect the Center's fiscal deficit to widen to around 4.6% of GDP in FY27, compared with the Budget target of 4.3%, implying a slippage of around 30bp. Although the de-escalation of tensions in West Asia and the US-Iran peace agreement have reduced the risk of a prolonged commodity shock, the fiscal impact has already been embedded in government finances through the reduction in fuel excise duties and the front-loaded increase in fertilizer and food subsidies. Additional downside risks stem from a potential shortfall in disinvestment receipts and weaker corporate tax collections.

* Nevertheless, we view the expected slippage as manageable rather than structural. The government has protected the quality of expenditure, with capital expenditure rising 13.4% YoY during Apr–May FY27 and running ahead of the pace required to meet the Budget target.

* Moreover, we do not expect the fiscal slippage to result in additional dated G-sec borrowings, as the government has sufficient financing flexibility through cash balances, small savings, and other financing sources. Consequently, we expect 10-year G-sec yields to remain broadly range-bound and continue to forecast the benchmark yield at around 7.2% by end-FY27.

May fiscal data showed continued resilience in tax collections, while expenditure normalized after the frontloaded spending in April.

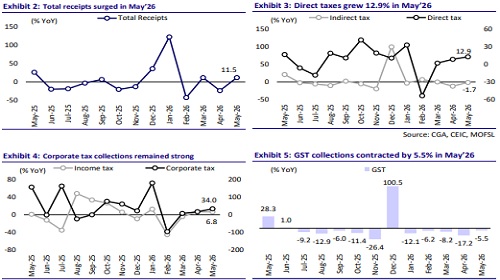

* The Center's fiscal position remained healthy in May 2026, with total receipts increasing 11.5% YoY to INR5.1t, supported by robust growth in non-tax revenue and continued strength in direct tax collections. Gross tax revenue rose 5.9% YoY, led by a 12.9% YoY increase in direct taxes, with corporate tax collections rising 34.0% YoY and income tax collections increasing 6.8% YoY.

* On the indirect tax front, collections remained broadly unchanged in May’26 (-1.7% YoY), as a sharp 48.8% YoY increase in customs duty collections was offset by a 21.5% YoY decline in excise duty collections, following the reduction in excise duties on petrol and diesel.

* Non-tax revenue increased 12.7% YoY in May’26, largely reflecting higher dividend and other receipts, lifting overall revenue collections during the month.

* On the expenditure side, total expenditure increased 9.1% YoY in May’26, driven primarily by revenue expenditure, which rose 11.8% YoY. Higher interest payments (+32.3% YoY) and subsidy expenditure (+43.1% YoY) continued to support revenue spending. Capital expenditure remained broadly flat (-0.6% YoY) after the sharp front-loading witnessed in April, reflecting normal month-to-month variation in project execution rather than any moderation in the government's investment priorities. Consequently, the Center recorded a monthly fiscal deficit of INR2.0t during May.

Center’s finances (FYTD; Apr’26-May’26)

* The Center's fiscal position during the first two months of FY27 reflects front-loaded expenditure while preserving capital spending, despite elevated geopolitical and commodity price uncertainties. Total expenditure increased 18.1% YoY, broadly similar to the 19.7% YoY growth recorded in the corresponding period last year.

* The increase was led by revenue expenditure, which expanded 20.1% YoY (vs. 9.4% YoY in FYTD26), largely due to a 47.4% YoY increase in subsidy payments amid elevated global fertilizer and food prices during the West Asia conflict. Interest payments also increased 22.8% YoY during the period.

* Importantly, cumulative capital expenditure remained robust, rising 13.4% YoY despite the sharp increase in subsidy spending. The composition of spending was particularly encouraging, with railway capex and capital transfers to states recording strong growth, while road sector spending remained relatively muted and defense capital expenditure contracted, largely reflecting the timing of project execution and procurement. Moreover, the current capex run rate of around INR1.3t per month is comfortably above the INR1.0t monthly pace required to achieve the FY27 Budget target of INR12.2t, indicating that infrastructure spending remains well ahead of schedule.

* On the receipts side, gross tax revenue remained broadly stable (+1.8% YoY). Within this, direct tax collections increased 10.5% YoY, led by a 26.1% YoY increase in corporate tax collections, while income tax collections grew 6.8% YoY, reflecting resilient corporate profitability and steady income growth. However, indirect tax collections declined 7.0% YoY, primarily due to a 19.7% YoY fall in excise duty collections following the reduction in fuel excise duties, which more than offset the 37.5% YoY increase in customs duty collections. Consequently, net tax revenue remained broadly unchanged (- 0.8% YoY) during the first two months of FY27.

* Meanwhile, non-tax revenue declined marginally by 1.7% YoY, although collections have already reached 52.7% of the full-year Budget Estimate, reflecting the front-loading of dividend receipts. Non-debt capital receipts contracted 22.0% YoY, highlighting the need for faster progress in disinvestment over the remainder of the fiscal year.

* As receipts lagged expenditure growth, the fiscal deficit widened to INR1.6t, equivalent to 9.6% of the FY27 Budget estimate. Nevertheless, the key takeaway is that the government has absorbed the temporary increase in subsidy expenditure without compromising its infrastructure-led investment strategy. With crude oil and fertilizer prices easing following the de-escalation of tensions in West Asia, subsidy pressures are expected to moderate, allowing the government to maintain its capital expenditure program while remaining broadly on track to achieve its FY27 fiscal deficit target.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412