Monthly Report on the Indian Aviation Sector June 2026 by ICRA

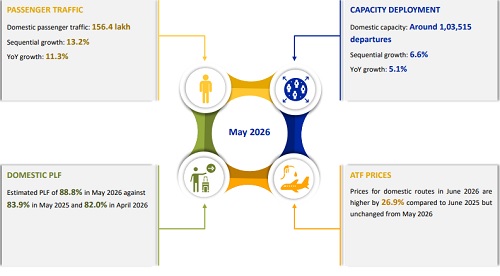

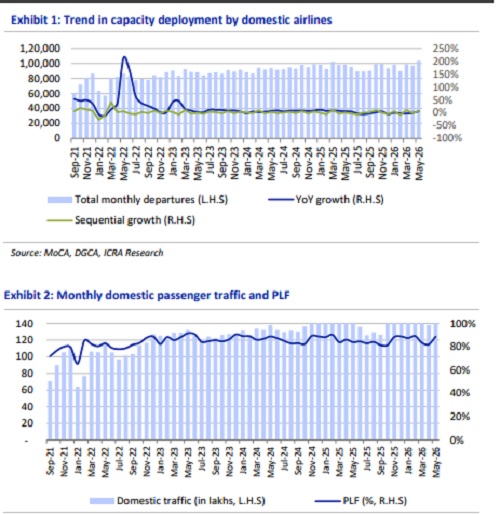

Domestic air passenger traffic has been estimated1 at 156.4 lakh in May 2026, 11.3% higher than 140.5 lakh in May 2025 and 13.2% higher than 138.1 lakh in April 2026. The airlines’ capacity deployment in May 2026 was 5.1% higher than May 2025 and 6.6% higher than April 2026. Domestic passenger traffic stood at 294.6 lakh in 2M FY2026 (April–May 2026), registering a year-over-year (YoY) growth of 3.8%. For FY2026 (April 2025-March 2026), domestic air passenger traffic was reported at 1,674.2 lakh, reflecting a modest YoY growth of 1.2%. The international air passenger traffic for Indian carriers grew by 3.9% to 350.0 lakh in FY2026. However, the same declined sharply by 39.0% YoY in April 2026 amid the disruptions caused by the West Asian conflict.

• Negative outlook on the Indian aviation industry – In March 2026, ICRA revised its outlook on the Indian aviation industry to Negative from Stable owing to expected weakening of the revenue per available seat kilometre – cost per available seat kilometre (RASK-CASK) spread due to hardening of aviation turbine fuel (ATF) prices and disruptions in the availability of certain international airspaces starting February 28, 2026, following escalation of the geopolitical conflict in West Asia, coupled with continued depreciation of the INR against the USD. Despite a 11% YoY growth in domestic air passenger traffic in May 2026, which was supported by a favourable base, given the demand disruption in May 2025 following the Pahalgam attack and the subsequent military conflict between India and Pakistan, ICRA has revised downwards its forecasts for the domestic air passenger traffic growth in FY2027 to 3-6%, from its earlier projections of 6- 8%. ICRA has also revised downwards its international air passenger traffic growth (for Indian carriers) forecasts for FY2027 to 0-3% from 8-10% earlier. These revisions reflect the impact of the West Asian conflict, which has resulted in a hike in fares due to the cost escalations for the airlines and the anticipated curtailment of discretionary spends because of increased inflation. Further, flight cancellations amid airspace closures have impacted international air travel demand, with some of the carriers having already announced curtailment of international flights in the coming few months.

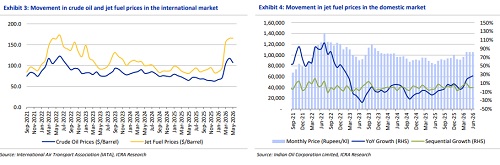

• ATF prices in June 2026 remained unchanged for domestic routes and reduced by 27% for international routes on a sequential basis – While the ATF prices announced on June 1, 2026, were kept unchanged for domestic routes vis-à-vis April and May 2026 prices, they are still higher by 26.9% on a YoY basis. This follows the pricing policies of oil marketing companies (OMCs) to support the domestic airlines. For international operations, the ATF prices in June 2026 have been slashed by around 27% on a sequential basis, tracking the correction in global aviation fuel benchmarks. However, the ATF prices for international operations remained higher by around 45% on a YoY basis.

Although domestic ATF price increases have been moderated through government intervention, fuel remains a dominant cost, accounting for 30-40% of airline operating expenses. Further, with 35-50% of airline costs being dollar-denominated—including fuel, aircraft lease rentals and maintenance expenses—sustained high crude prices and a weak rupee continue to pose risks. Also, some airlines have foreign currency debt. Although domestic airlines benefit from a partial natural hedge through earnings from international operations, they have net payables in foreign currency. The yield movement thus remains monitorable in the current situation of escalating costs.

To support the industry, in April 2026, the Ministry of Civil Aviation (MoCA) announced a reduction in the landing and parking charges for domestic airlines by 25% for three months starting April 2026. Further, on May 5, 2026, the Government approved the Emergency Credit Line Guarantee Scheme (ECLGS) 5.0 worth Rs. 5,000 crore to provide targeted support to the aviation sector by addressing nearterm liquidity constraints and improving access to credit. The scheme enables scheduled passenger airlines to avail additional funding, with credit guarantee coverage of 90% and borrowing limits of up to 100% of the peak working capital utilised during Q4 FY2026 (capped at Rs. 1,500 crore per airline). Such liquidity support, coupled with a longer repayment tenure of up to seven years (including a twoyear moratorium), provides airlines with greater financial flexibility to manage operational disruptions arising from the geopolitical uncertainties. SpiceJet has drawn a part of the eligible limits under ECLGS 5.0 in June 2026.

In addition, the Governments of Maharashtra and Delhi have undertaken reductions in value-added tax (VAT) on ATF, with Maharashtra reducing VAT to 7% from 18% effective May 15, 2026, and Delhi implementing a decrease to 7% from 25% effective May 16, 2026. While this measure offers only partial mitigation against structurally high fuel costs and currency pressures, easing of ATF prices and the overall operating costs remain critical for a sustainable revival in profitability of the sector.

• The Government of India’s approval of the ATF price stabilisation fund, announced on June 3, 2026, is another intervention aimed at cushioning airlines from this extreme fuel price volatility. The scheme provides a one-time budgetary support, not exceeding Rs. 10,000 crore, to OMCs through interest-free advances, enabling them to offer more stable and predictable ATF pricing to scheduled Indian airlines for a 36-month period (with provision for annual review). By effectively smoothing out sharp fluctuations in international fuel prices, the mechanism creates a buffer for airlines and reduces their exposure to sudden cost spikes amid the West Asian crisis. The stabilisation fund is expected to improve cost visibility for airlines, particularly in a phase where profitability remains under pressure due to high fuel costs and competitive intensity. It will reduce the pass-through of fuel price shocks to passengers, thereby helping to moderate fare volatility, and thus assisting in the sustenance of passenger demand. The mechanism can help limit margin volatility and support continuity of operations, reducing the likelihood of abrupt capacity cuts or network rationalisation that were visible in recent months due to elevated fuel prices. At the same time, the measure is structured as a temporary buffer. Nevertheless, the scheme involves price lock-in over an extended period, which could influence airline participation. With global fuel prices having softened meaningfully since mid-June 2026, following expectations of a peace agreement to resolve the West Asian conflict, airlines opting for the mechanism may be unable to fully benefit from lower spot prices. Accordingly, the extent of participation, and the proportion of ATF requirements that airlines choose to route through this mechanism, will remain monitorable.

• Indian aviation industry2 to report net loss of Rs. 360-380 billion in FY2027, as against an estimated net loss of Rs. 320-340 billion in FY2026 –The Indian aviation industry is estimated to have reported a net loss of Rs. 320-340 billion in FY2026, much higher than ICRA’s earlier estimates of Rs. 170-180 billion, primarily on account of the foreign exchange (forex) losses arising from the sharp depreciation of the INR, moderation in passenger traffic growth and an increase in ATF prices following the rise in crude oil prices amid the West Asian conflict towards the end of FY2026. For FY2027, while losses were earlier projected to narrow to Rs. 110-120 billion, supported by an improvement in passenger traffic, the outlook has since deteriorated. The onset of the West Asian conflict since end-February 2026 is expected to result in subdued air passenger traffic growth in FY2027. Additionally, increased costs due to depreciation of the INR against the USD, elevated ATF prices and an anticipated rise in lease rentals owing to continued aircraft deliveries have collectively led ICRA to revise its FY2027 net loss forecasts upwards to Rs. 360-380 billion, as these cost escalations may not be adequately passed on by way of fare hikes.

• Supply chain challenges persist – The industry continues to face supply chain challenges with respect to the engine failure issues with Pratt & Whitney (P&W). Overall, engine failures and supply chain challenges resulted in the grounding of 99 aircraft for select airlines as of March 2026, accounting for 11-13% of the total industry fleet, affecting the overall industry capacity. This, however, gradually improved from 20-22% of the total industry fleet grounded as on September 30, 2023. The aircraft-on-ground situation has resulted in growing operating expenses owing to the cost of grounding, higher lease rentals on account of additional aircraft taken on lease (primarily wet leases) to offset the grounded capacity, rising lease rates and lower fuel efficiency (due to replacement by older aircraft taken on spot lease). These factors have adversely impacted airlines’ cost structures. However, healthy yields, high passenger load factor (PLF) and partial compensation from engine original equipment manufacturers (OEMs) are helping absorb the impact to an extent.

• Select airlines face financial challenges, liquidity tightness – While some airlines have adequate liquidity and/or financial assistance from strong parent companies, supporting their credit profiles, the credit metrics and liquidity profiles of others remain under pressure, despite some improvement in recent years.

Domestic air passenger traffic: 11.3% YoY growth in May 2026

The capacity deployment for May 2026 was higher by 5.1% than May 2025 (around 103,515 departures in May 2026 against 98,457 in May 2025). The number of departures in May 2026 was higher by 6.6% on a month-over-month basis. In FY2026, the capacity deployment remained largely flat, after a rise in the same by 7.3% in FY2025.

In May 2026, domestic air passenger traffic stood at 156.4 lakh against 140.5 lakh in May 2025, implying a YoY growth of 11.3%. On a sequential basis, domestic air passenger traffic in May 2026 was higher by 13.2%. The domestic air passenger traffic for May 2025 was impacted due to the Pahalgam terror attack in the later part of April 2025 and the subsequent military conflict between India and Pakistan in May 2025, which caused a temporary moderation in travel demand. In FY2026, domestic air passenger traffic stood at 1,674.2 lakh, reflecting a growth of 1.2% over FY2025, in line with ICRA’s estimates of 0-3%.

In May 2026, the average daily departures were around 3,339, 5.1% higher than around 3,176 in May 2025 and higher by 3.2% compared to around 3,236 in April 2026. The average number of passengers per flight was 151 in May 2026, higher than 143 in May 2025 and 142 in April 2026. It is estimated that the domestic aviation industry operated at a PLF of 88.8% in May 2026 vis-à-vis 83.9% in May 2025 and 82.0% in April 2026.

ATF prices for domestic routes were higher by 26.9% YoY in June 2026 but remained unchanged on a sequential basi

The ATF prices announced on June 01, 2026, remained unchanged on a sequential basis but increased by 26.9% on a YoY basis. For Q1 FY2027, the ATF prices are higher by 22.8% on a YoY basis. In FY2026, the average ATF prices were lower by 4.1% than the average prices in FY2025 as crude oil prices moderated in most of the months in FY2026 on a YoY basis, before hardening post the initiation of the conflict in West Asia. Crude oil prices have witnessed a significant correction since mid-June 2026, driven by improved market sentiment following expectations of a peace agreement to resolve the West Asian conflict.

Above views are of the author and not of the website kindly read disclaimer