Textiles Sector Update : Headwinds easing, margin recovery awaited by Prabhudas Liladhar Capital

Indian textiles sector, more particularly the ready-made garments (RMG) segment, is entering FY27 with renewed structural optimism. Following a challenging period marked by global inflation and elevated trade barriers, recent macro-policy shifts— including key tariff realignments and highly anticipated FTAs—are expected to lift industry revenue for the fiscal year, with expectations of some early momentum in Q1FY27. However, most of the order bookings for the first quarter (rather for H1FY27) were already done before the abolishment of reciprocal tariffs, and hence, margin recovery may not be very prominent during the quarter.

Prices of fuel, packaging, polyester trims, etc., remained elevated during the quarter due to Middle East tensions. However, we expect gross margins of RMG players to be stable (on YoY basis) due to their ability to pass on the raw-material price increases. These companies are expected to post marginal improvement in EBITDA margin due to better fixed cost absorption as volume grows. Upstream players supplying yarn are expected to see robust revenue growth and improved profitability due to better cotton-yarn spreads and strong demand from export markets, especially China. Given the ability to control the complete supply chain, integrated textile players are more likely to benefit from the multiple tailwinds on yarn as well as the RMG front.

Pearl Global Industries Ltd (PGIL): We expect PGIL to report 18% YoY growth in garment volume to 20.3mn pcs, with Bangladesh continuing to grow and India experiencing some recovery post removal of reciprocal tariffs. However, the company is unlikely to see any immediate price revisions, and we expect the blended realization to remain steady on QoQ basis, close to INR640/pc. Accordingly, we estimate revenue of INR13,179mn at consolidated level, implying YoY growth of 7.3%. We expect EBITDA margin to improve by 80bps led by higher volume. The stock price has seen a sharp run-up since we initiated coverage on the stock, owing to heightened optimism around the India-UK Comprehensive Economic and Trade Agreement (CETA) and US-India Bilateral Trade Agreement (BTA). While our FY28 estimates are broadly unchanged, we remain positive on PGIL’s growth prospects and re-rate the stock at 24x of FY28EPS (earlier, 22x FY28 EPS). This implies TP of INR2,274/share. We revise the rating to ‘Accumulate’.

US market

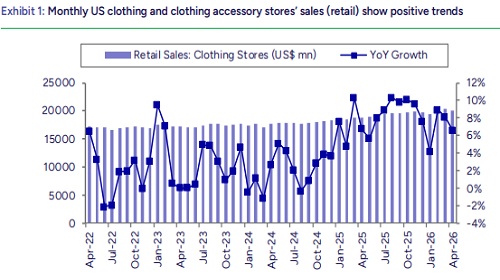

The steep reciprocal tariffs on Indian textiles and apparels were slashed to 18% effective Feb’26, a sharp drop from the 50% peak (comprising 25% baseline plus 25% Russian-oil penalty) that severely disrupted exports in FY26. With the effective rate now at or below several competing sourcing hubs, India has regained its competitive footing against Vietnam and Bangladesh. However, because buyers who diversified during the tariff spike are migrating back gradually, order book normalization is expected to be a phased process. Consequently, we expect a gradual volume recovery in Q1–Q2FY27, with the ongoing US-India BTA negotiations serving as a critical swing factor. Recent sales data from US apparel retail stores shows encouraging trends, signaling robust underlying demand for imported apparels.

EU market

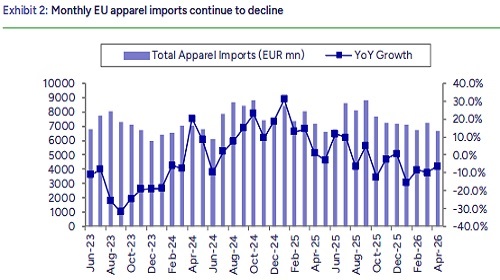

Latest available Eurostat data shows continued YoY decline in apparel imports (knitted + woven) during the first 4 months of CY26. This contraction is largely driven by weak European consumer demand and high retailer caution regarding existing inventories. Conclusion of the India-EU FTA on 27th Jan’26 marks a structural turning point for Indian apparel exporters, eliminating the 9.6% to 12% tariff that long favored duty-free competitors like Bangladesh and Pakistan. While complex ratification processes mean the operational tailwinds will materialize over FY27–29, rather than driving immediate Q1FY27 numbers, forward-looking sourcing discussions between international buyers and Indian export houses are already underway

UK market

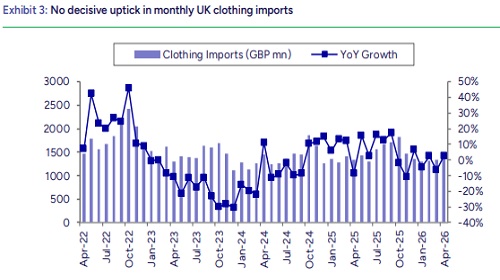

Effective 15th Jul’26, the India-UK CETA removes the 8% to 12% duty disadvantage that historically restricted Indian apparel exporters. While UK’s clothing imports have shown mixed trends in recent months, this agreement levels the playing field against duty-free competitors like Bangladesh, Cambodia and Turkey. This structural shift heavily favors organized Indian manufacturers over the UK's traditional, smaller scale supplier base. However, given that the ratification of CETA will start from Jul’26, and retailers may need time to realign supply chains, Indian apparel exporters may not see a marked uptick in exports to the UK during Q1FY27.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...