Healthcare Sector Update : EBITDA growth to remain subdued by Motilal Oswal Financial Services Ltd

* After a subdued show in FY26 (revenue growth of 10.8% YoY excl. hospitals), we expect our coverage universe to deliver better growth in 1QFY27. Aggregate revenue is likely to rise 13.2% YoY. However, profitability is expected to remain under pressure, with EBITDA likely to grow by a modest 5% YoY and PAT estimated to decline 5% YoY, primarily due to pricing pressure in select high-margin niche products in the US and an unfavorable geopolitical environment. These headwinds are expected to be partly offset by currency tailwinds and robust growth in the domestic formulation (DF) segment.

* DF growth is expected to strengthen, supported by a healthy recovery in acute therapies alongside stable momentum in chronic therapies. The launch of generic semaglutide in India following patent expiry in Mar'26 marks a key development, and the initial impact on market expansion and competitive dynamics will be closely monitored during the quarter. In the US, while pricing pressure persists in the base business, several companies continue to focus on complex generics, specialty products, and limited-competition launches, supported by exclusivity opportunities, which should drive healthy outperformance for select players. USFDA ANDA approvals recovered during 1QFY27, while the pace of USFDA inspections remained healthy, providing incremental support to the regulatory outlook.

* Among healthcare services, hospitals are likely to maintain their outperformance, with ~16% YoY revenue growth, driven by ongoing capacity additions and healthy ARPOB improvement. However, margins may remain under pressure owing to the ramp-up of newly commissioned facilities. Overall, we believe near-term profitability across pharma and hospitals is likely to remain constrained by margin headwinds, though healthy domestic demand, regulatory normalization and capacity-led expansion support a constructive medium-term growth outlook

DF: Growth momentum remains intact, led by acute recovery and resilient chronic demand

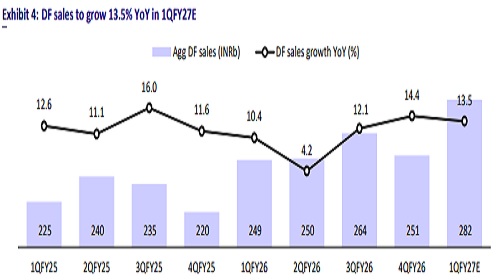

Coverage companies to sustain growth

For our coverage universe, we expect aggregate DF segment sales to grow 13.5% YoY to INR282b in 1QFY27. Following a modest 4% YoY growth in 2QFY26, the DF market has witnessed a steady improvement, and we expect YoY growth to accelerate for the third consecutive quarter, supported by a recovery in acute therapies and sustained strength in chronic segments. Our coverage companies are likely to broadly track industry growth, aided by continued product launches, pricing actions and an increasing portfolio mix toward high-growth chronic therapies.

Chronic therapies show resilient; acute recovery gains traction

During the first two months of 1QFY27 (Apr-May'26), chronic therapies delivered ~15.5% YoY growth, largely in line with 16% YoY growth recorded in 4QFY26 and well ahead of 13.6%/9.9% growth seen in FY26/FY25. Acute therapies also exhibited a meaningful recovery, with growth improving to 10% YoY in Apr-May'26 from7.5%/7% in FY26/FY25. Robust momentum in cardiac, anti-diabetic, and vitamins, minerals & nutrients (VMN) continued to outperform the IPM, although overall IPM growth remained constrained partly by softer trends in anti-infectives and respiratory therapies.

TRP/LPC/DRRD to lead DF growth in 1QFY27

We expect TRP/LPC/DRRD to report DF sales growth of 43%/13%/13% YoY, driven by a combination of price hikes, new product launches and improving productivity of medical representatives (MRs). TRP's growth will be aided by the consolidation and integration of the acquired JB Pharma business, alongside broad-based doubledigit growth in its key therapies, particularly chronic segments, supported by strong IQVIA market share trends for the three months ending in May'26. Meanwhile, LPC and DRRD are expected to post broad-based growth across most therapy areas. We also expect GNP to deliver 12.5% YoY DF growth, supported by continued strength in its anti-infectives and antineoplastic portfolios.

ALPM/GSK/ERIS expected to underperform in 1QFY27

We expect ALPM/GSK/ERIS to underperform peers in 1QFY27, with DF sales growth of 6%/8%/9% YoY owing to muted performance of key therapies in the acute and chronic segments.

US sales: YoY decline to continue amid g-Revlimid normalization CIPLA/DRRD/ZYDUSLIF to drag down overall YoY growth

For our coverage universe, US revenue is expected to decline 5.4% YoY to USD2.3b in 1QFY27, primarily due to a steep 28%/30% YoY decline in US sales for CIPLA/DRRD to USD163m/USD327m. The decline reflects intensifying competition across several niche products, including g-Revlimid, resulting in price erosion and lower revenue contribution for domestic generic players, particularly CIPLA, DRRD and ZYDUSLIF. INR depreciation is, however, likely to provide a favorable forex tailwind, translating into 4.6% YoY growth in INR terms. Additionally, high freight costs amid ongoing geopolitical disruptions are expected to weigh on profitability during the quarter. Excluding CIPLA and DRRD, aggregate US revenue for the coverage universe is expected to grow 2.6% YoY, reflecting relatively resilient underlying demand and contribution from recent product launches.

RUBICON/LPC/GNP to outperform in the US market

The overall weakness in US sales is expected to be partially offset by robust growth from RUBICON, LPC and GNP. We expect RUBICON to report 32% YoY growth, supported by a healthy pipeline of new launches, continued market share gains in its base portfolio, increasing contribution from specialty and differentiated products, and expansion in the domestic business. LPC is likely to deliver 28% YoY US growth, driven by sustained product launch momentum, which should more than offset competitive pressure in Mirabegron and Tolvaptan. GNP is also expected to post healthy growth, supported by continued execution of its launch pipeline.

USFDA approval momentum to recover

USFDA regulatory activity remained healthy in 1Q. About 13 manufacturing facilities belonging to companies under our coverage were inspected during 1QFY27. At the industry level, 202 final approvals were granted during the quarter (vs. 184 in 4QFY26), while our coverage companies received 59 final approvals. The steady improvement from the lows witnessed in 2QFY26, followed by stabilization over subsequent quarters, indicates a gradual normalization in inspection activity, approval conversion and regulatory review timelines, which should support product launch momentum over the medium term.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

Automobiles Sector Update : MSIL/TMPV outperform in PVs, TVS in 2Ws, and TMCV in CVs by Moti...

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...