Buy Urban Company Ltd for the Target Rs.125 by Motilal Oswal Financial Services Ltd

Convenience at a pricey valuation

* Urban Company (URBANCO) operates a hyperlocal online home services marketplace spanning cleaning, repairs, beauty, and maintenance. The broader home services market (~USD60b in FY25) is poised to benefit from rising urbanization, busier lifestyles, and improving income levels.

* Persistent offline inefficiencies such as inconsistent service quality, opaque pricing, unreliable availability, and weak post-service support are being addressed by technology-led platforms offering standardized service, transparent pricing, and structured grievance redressal.

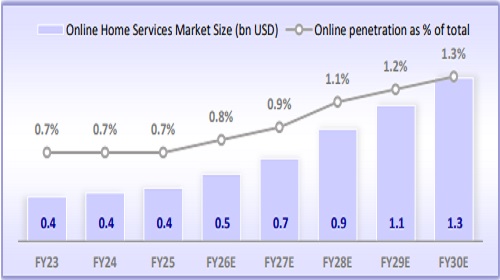

* The online full-stack home services market stood at ~INR41–43b in FY25 and is expected to grow at 18–22% CAGR over FY25–30. Yet online penetration remains sub-1% of the overall industry.

* We believe habit formation will take time, given the relationship-driven nature of services traditionally fulfilled offline. URBANCO commands ~70% online market share; as competition rises, we expect this to moderate toward ~55%, while retaining category leadership.

* We forecast India’s consumer services NTV to post ~17% CAGR over FY25- 37E, aided by rising urbanization, higher category adoption per cohort, and a gradual rise in online penetration. Its EBITDA margin is expected to improve by ~840bp over FY25–37, driven by operating leverage, better micro-market densification, and a higher share of retained users.

* Adjacencies such as Native deepen ecosystem integration: Leveraging appliance installation and servicing expertise, Native (water purifiers and electronic door locks) enhances customer stickiness through lower lifetime ownership costs, app-led monitoring, and reliable after-sales service. Rising revenue contribution positions this segment as a higher-margin growth lever beyond core services. ? InstaHelp represents early-stage optionality with near-term profitability trade-offs: The on-demand instant services category addresses real needs but remains more situational than habitual. Continued investments in onboarding, training, and supply expansion are likely to sustain cash burn, making the adoption trajectory and unit economics key monitorables.

* We value URBANCO on an SoTP basis. For the India Consumer business, we ascribe a 50x EV/EBITDA multiple, given URBANCO’s strong market share, translating into a per-share value contribution of INR 85. We value Native at 3x FY28 EV/sales(~20% premium to traditional OEMs) due to its higher growth and differentiated value proposition, resulting in a per-share value of INR 11. The International business is valued at 2x FY28 EV/Sales (per-share value of INR5).

* We believe InstaHelp is at an early stage of its business and remains an optionality; hence, we value it at 1.5x FY28 EV/NTV (per-share value of INR 10). Adjusted for cash, we arrive at an SoTP-based price of INR 125. Despite strong structural tailwinds and category leadership, we see a balanced riskreward at current valuations given gradual habit formation, penetration, potential competitive risks, and investment-led margin trade-offs; hence, we initiate coverage with a NEUTRAL rating.

First-mover advantage: Early to pick the market in the hyperlocal home services marketplace ? URBANCO’s operating model provides an early structural advantage in building a multi-category, hyperlocal home services marketplace.

* The platform is organized at a micro-market level (typically 3–5 km radius), enabling tighter supply-demand matching, lower travel time, and improved fulfillment timelines.

* As penetration deepens within micro-markets, demand density improves, strengthening unit economics and enabling cross-category expansion. With over 12,000 service micro-market combinations across cities and categories, the company has built granular operational depth.

* We believe this densification model aids repeat usage, higher NTV per cohort, and gradual emergence of network effects as scale improves across cities.

Habit formation still early; penetration and disintermediation key monitorables

* Despite operating in a large serviceable addressable market, online penetration in home services remains sub-1% of the overall industry. The online full-stack market stood at ~INR41–43b in FY25 and is expected to grow at 18–22% CAGR over FY25–30, yet habit formation remains gradual. ? The category is inherently relationship-driven, traditionally fulfilled by local offline providers, which slows behavioral transition to digital platforms.

* Disintermediation remains a structural risk, as consumers and professionals may transact off-platform once relationships are formed. This dynamic can act as a natural friction to faster habit formation and monetization.

* While engagement metrics are improving—retained users contributing ~84% of NTV in 9MFY26 versus ~72% in FY22—penetration expansion is likely to remain measured. ? We believe penetration velocity, repeat frequency, and disintermediation levels will be critical variables in assessing long-term growth sustainability.

Retention improving; monetization expanding, but new cohorts softer

* Cohort analysis indicates steady improvement in retention and monetization among older customer vintages. NTV contribution from retained users has increased meaningfully over time, supported by cross-selling across supercategories and rising category adoption per household.

* By later years, retained users engage across more than five categories on average, reflecting a gradual deepening of platform reliance rather than frontloaded adoption.

* However, more recent cohorts have exhibited relatively softer spending vs. earlier vintages, possibly due to broader acquisition, rising competition, and slower habit formation among newer users.

* While this divergence warrants monitoring, overall retention trends remain constructive. We believe sustained customer acquisition combined with crosscategory penetration will be necessary to maintain healthy NTV growth as the platform scales.

Superior service professional monetization strengthens the supply moat

* Service professional earnings remain structurally stronger than both offline peers and hyperlocal gig workers, reinforcing supply stability. On average, platformassociated professionals earned 30–40% more than non-platform peers, aided by higher utilization and reduced travel time through tighter micro-markets.

* Compared to hyperlocal delivery workers, hourly earnings are superior despite fewer working hours. Tier-based progression (Bronze, Silver, Gold) incentivizes continuity and productivity.

* We believe this superior monetization profile supports service quality, reduces churn risk, and strengthens the transition of skilled workers from the unorganized and organized offline ecosystem onto the platform.

InstaHelp: Optionality today, scaled opportunity tomorrow

* InstaHelp represents URBANCO’s entry into on-demand instant household services, addressing short-duration cleaning and housekeeping needs. The category is early-stage and largely situational rather than habitual, given the relationship-driven nature of domestic help in India.

* While order ramp-up has been rapid, the segment requires significant upfront investment in onboarding, training, and supply density, which is likely to keep near-term profitability under pressure.

* AOV remains relatively low, and unit economics are still evolving. However, we view InstaHelp as an engagement lever that can increase household touchpoints and expand addressable use cases over time.

Valuation and View: Initiate with Neutral rating

* URBANCO will be a significant beneficiary of the gradual formalization of India’s fragmented home services market as consumption shifts from unorganized offline providers to organized, technology-led platforms.

* With a dominant share in online home services (~70%), strong micro-market execution, and structurally superior service professional monetization, the company is well-positioned to scale profitably as penetration improves over the medium term.

* The Indian consumer services business remains the primary growth and valuation driver. We forecast India consumer services NTV to clock ~17% CAGR over FY25-37E, supported by rising urbanization, higher category adoption per cohort, and gradual online penetration increase from sub-1% currently.

* EBITDA margin is expected to improve by ~840bp over FY25–37, driven by operating leverage, better micro-market densification, and a higher share of retained users (NTV contribution from retained users rising from ~72% in FY22 to ~84% in 9MFY26).

* While disintermediation and slower habit formation remain structural risks, improving cohort retention, category expansion (five-plus super categories over time), and stable app ratings (~4.8) support long-term monetization visibility.

* The Native segment represents a strategic adjacency leveraging URBANCO’s appliance servicing ecosystem. We estimate Native NTV CAGR of ~25.4% over FY25–37E, supported by low penetration in water purifiers.

* InstaHelp addresses short-duration, on-demand domestic assistance and represents URBANCO’s entry into a large but habit-fragmented segment.

* We value URBANCO on an SoTP basis. For the India Consumer business, we ascribe a 50x EV/EBITDA multiple, given URBANCO’s strong market share, translating into a per-share value contribution of INR 85. We value Native at 3x FY28 EV/sales(~20% premium to traditional OEMs) due to its higher growth and differentiated value proposition, resulting in a per-share value of INR 11. The International business is valued at 2x FY28 EV/Sales (per-share value of INR5).

* We believe InstaHelp is at an early stage of its business and remains an optionality; hence, we value it at 1.5x FY28 EV/NTV (per-share value of INR10). Adjusted for cash, we arrive at an SoTP-based price of INR 125.

* While URBANCO is well positioned to benefit from the long-term formalization of home services, we believe current valuations already reflect much of the growth potential, and execution risks around habit formation, penetration, disintermediation, and newer initiatives keep the risk-reward balanced; accordingly, we initiate with a NEUTRAL rating.

* Key downside risks: 1) slower-than-expected growth in online penetration given the relationship-driven and informal nature of home services, 2) elevated disintermediation as consumers and service professionals transact off-platform post initial discovery, 3) rising competitive intensity—particularly in instant services leading to higher discounts and customer acquisition costs, and 4) prolonged losses in InstaHelp due to supply build-out and lower AOVs.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041