Buy TBO Tek Ltd for the Target Rs.1,360 by Motilal Oswal Financial Services Ltd

Scaling the global travel stack

Niche B2B global travel aggregator: Connecting supply, compounding growth

* TBOTEK is a technology-driven B2B travel platform that connects over 750 airlines, more than 1m hotels, and travel buyers worldwide. Its platform offers a one-stop solution for travel buyers, having evolved from a simple air ticketing platform for agents into a comprehensive global travel booking platform, with an annual GTV of INR308b (~41% from airlines and ~59% from hotels and ancillaries) and over 50k transacting partners.

* TBOTEK has built strong moats in the global B2B travel distribution ecosystem over time through deep supply aggregation across airlines, hotels, and ancillaries (transfers and sightseeing, car rentals, and cruises), targeting a highly fragmented travel agent universe of ~2m, spanning freelancers, home-based consultants, small independent agencies, and full-time professional firms.

* The global travel and tourism market, valued at ~USD1,869b, is expected to expand at a CAGR of 8.2% over CY23–27. Within this, the hotel segment is likely to expand at a faster CAGR of ~10%, while the ancillary and air segments are expected to expand at a CAGR of 8.5% and 5.7%, respectively. In terms of market composition, the segment mix currently stands at: 46% for Hotels, 38% for Air, and 16% for Ancillary Services. Notably, the hotels segment is highly fragmented, with over 80% of hotels (~3-3.6m) being independently owned, making it extremely difficult for intermediaries to establish direct reach.

* TBOTEK addresses the structural challenges faced by fragmented travel intermediaries by providing an integrated global travel distribution platform. It aggregates travel supply across 4,25,000+ source destination pairs, supported by payment rails in 88 currencies, localized solutions, and 24×7 near-shore support in 16 languages. A multi-market compliance layer and streamlined booking infrastructure enable travel agents to broaden product access, improve operational efficiency, and compete more effectively, ultimately enhancing the end-traveler experience.

* We expect TBOTEK to deliver Revenue/EBIT/PAT CAGR of 35%/37%/32% over FY25- 28, primarily on the back of increased contribution from high take-rate hotels and ancillary segments in the GTV mix, rising from 59% currently to 70%. Contribution from CV, which is focused on luxury and premium hotel properties, is expected to drive overall profitability. We value the stock at 28x FY28E EPS of INR48.7 to arrive at a TP of INR1,360. We initiate coverage on TBOTEK with a BUY rating.

* On the operating profitability front, we expect EBITDA margins to expand gradually from FY27 onwards, led by operating leverage as the business continues to scale and a gradual tapering of SG&A expenses, with EBITDA margins rising from 13.7% as of 3QFY26 to ~18.0% by 4QFY28. A structurally negative working capital model is expected to support a strong FCF CAGR of over 40% between FY25-28.

A B2B play in the fragmented global travel ecosystem

* The B2B model provides structural advantages over OTAs, allowing agents to access highly fragmented travel inventory at B2B pricing with lower mark-ups. This enables agents to match OTA prices while maintaining healthy margins.

Scalable asset-light model

* In FY25, TBOTEK expanded into over 15 new countries and 40 cities to strengthen its distribution reach. Its cost-efficient India back-end, combined with localized front-end operations and local support across 55 countries, enhances agent stickiness.

* Notably, travelers often rely on offline agents for on-trip assistance and the convenience of paying in local currencies. This is particularly relevant for firsttime international travelers from Tier-2/3 towns, who typically require support with forex arrangements and complex multi-destination itineraries. Platforms like TBOTEK support agents in navigating these operational hurdles effectively.

Acquisition-led growth strategy

* Acquisitions strengthen TBOTEK’s premium supply and increase wallet share in the fragmented global travel ecosystem. For instance, the acquisition of CV provides entry into the large US luxury outbound market, adding ~1,500 premium hotel contracts and a network of ~10K advisors.

* While CV currently operates at lower margins, TBOTEK expects to unlock synergies through cross-selling global premium destinations, integrating luxury supply into its platform, and reducing costs via technology integration and offshore operations. Interestingly, this strategy mirrors global OTA leaders, such as Expedia Group and Booking Holdings, which have historically leveraged acquisitions to scale supply, expand into new markets, and drive cross-platform growth.

Focus on high-margin hotel play

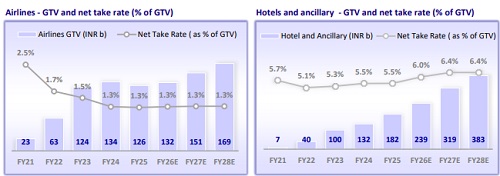

* TBOTEK is shifting its business away from low-margin air ticketing to highermargin hotels and ancillaries by strengthening its international supply of luxury hotels, cruises, car rentals, and Eurorail products. Hotel GTV contribution increased from 45% to 59% over FY23-25.

Valuation and view: Initiate coverage with a BUY rating

* We believe TBOTEK offers a structural play in the B2B global outbound travel market, enabling offline travel agents and enterprise buyers across geographies to access international airlines, hotels, and ancillaries.

* Globally, the B2A travel distribution landscape comprises nearly ~2m travel agents, spanning freelancers, home-based consultants, small independent agencies, and full-time professional firms. Notably, TBOTEK targets the full spectrum of travel agents, and the breadth and fragmentation of this base underscores a large total addressable market, providing significant headroom for penetration, wallet share gains, and geographic expansion over time.

* We expect TBOTEK to deliver Revenue/EBIT/PAT CAGR of 35%/37%/32% over FY25-28, mainly on the back of increased contribution from high take-rate hotels and ancillary segments in the GTV mix, rising from 59% currently to over 70%. Contribution from CV is expected to drive overall profitability, given its focus on luxury and premium hotel properties.

* TBOTEK is currently trading at a P/E of 46x/32x/21x for FY26E/FY27E/FY28E. With an RoE/RoCE of 26%/21% in FY28E, we value TBOTEK at a 28xFY28E EPS of INR48.7 to arrive at our TP of INR1,360 and initiate with a BUY rating

Key risks and concerns

* Extreme weather may impact destination accessibility; 2. Rising travel costs could impact airfares and accommodation prices; 3. Geopolitical uncertainty may influence traveler sentiment and route planning.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041