Buy Kalyan Jewellers Ltd for the Target Rs.550 by Motilal Oswal Financial Services Ltd

India demand resilient; deleveraging to boost return ratios

* Kalyan Jewellers (KALYAN) is likely to sustain a strong growth trajectory as India's jewelry demand for top brands remains strong. Despite a sharp rise in average gold prices (~80% YoY, ~20% QoQ in 4QFY26), the demand momentum remained robust through Jan–Mar, well supported by the wedding season. In 9MFY26, the India business reported ~35% revenue growth for KALYAN, driven by ~20% SSSG and network expansion (net additions of ~40 My Kalyan and ~37 Candere stores). NonSouth markets (54% of revenue) outperformed and clocked 42% growth vs. 28% growth in the South, reflecting successful pan-India diversification. Elevated gold prices continue to accelerate the shift towards organized players, with a new customer mix for KALYAN standing at ~40%.

* Candere continues to scale strongly, supported by demand for lightweight and studded jewelry, with revenue increasing to ~INR2.9b in 9MFY26 (vs. ~INR1.4b YoY). The business turned profitable in 3QFY26 and is driving incremental customer acquisition. Consumer preference for lightweight jewelry is certainly helping the company to attain a faster growth trend.

* In the Middle East (~11–12% of revenue), the company reported ~21% growth during 9MFY26. The demand momentum was healthy at the beginning of the quarter, but the same has been hit by the geopolitical challenges. These geopolitical escalations will remain a key monitorable in the near term.

* KALYAN plans to open 80-90 stores in FY26, with gross additions of 46 stores (net 40) already achieved in 9MFY26. Execution remains on track, though minor store openings may see a delay due to the recent geopolitical impact on construction activities.

* The company’s India EBITDA margin expanded ~30bp YoY to ~6.9% in 9MFY26, supported by favorable product mix, operating leverage, and procurement efficiencies. The company continues to focus on vendor consolidation and cost optimization to sustain margin expansion. Balance sheet strength is improving, with plans to reduce net debt to ~INR4b in FY26 (INR5.5b in 1HFY26) and a target to become debt-free by FY27. Lower interest costs will support PBT margin expansion (~90bp YoY to ~5.8% in 9MFY26).

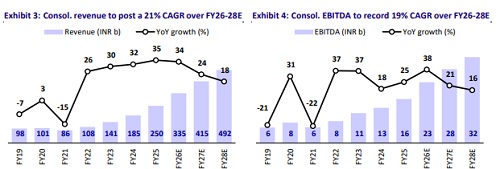

* KALYAN would deliver a revenue/EBITDA/APAT CAGR of 33%/29%/54% over FY22- 26E. We model a CAGR of 21%/19%/23% in revenue/EBITDA/PAT over FY26-28E. The stock trades at ~24x/20x P/E on FY27/FY28E and at <1x FY27E sales, offering an attractive risk-reward. We reiterate our BUY rating with a TP of INR550, based on 30x Mar’28E P/E.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041