Metals and Mining Sector Update : HRC up ~13%, rebar up ~20% quarter-to-date By Elara Capital

War disruption bolsters near-term prices

Quarter-to-date, average prices of hot-rolled coil (HRC) and primary rebar have surged by ~13% and ~20%, respectively. This upward momentum positively influences margin of steel producers. A 19% spike in international thermal coal prices in the past two months, combined with ongoing gas shortages, will likely hinder secondary steel mills’ capacity to cut prices once peak seasonal demand subsides. With competing product prices holding firm, primary long steel prices are poised to remain supported. Gas constraints should further limit supply of galvanized steel, adding upward pressure on prices. On the aluminium front, near-term prices are likely to remain elevated, fueled by higher thermal coal cost and supply disruptions in the Middle East, which accounts for ~8% of global aluminium production.

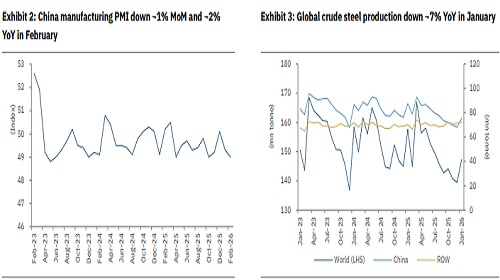

CY26 begins with a decline in global steel production YoY: According to the World Steel Association, global crude steel production began CY26 on a weaker note, declining ~7% YoY to ~147.3mn tonne. The drop was primarily driven by China’s production falling ~14% YoY while output in the rest of the world (ROW) increased ~3% YoY, partly offsetting the decline. On a monthly basis, however, global production improved ~6% MoM, led by a ~10% MoM rebound in China’s crude steel output, while production in ROW increased ~1% MoM. The monthly recovery suggests stabilization in production after the sharp YoY decline.

Middle East disruptions impact steel trade flows: China exports roughly 25–30mn tonne of steel annually to the Middle East. Disruption to regional shipping routes could force China’s mills to redirect shipments toward Southeast Asia or domestic markets, thereby increasing supply pressure across alternative export destinations. Meanwhile, India’s steel exports to the Middle East have slowed amid freight volatility and rising shipping risks. Cargo originally bound for the EU is increasingly being rerouted via the Cape of Good Hope, extending transit times by ~10–20 days and significantly increasing freight cost.

Steel prices sustain upward momentum globally: China’s HRC export prices continue their recovery trend that began in December, rising ~3% MoM in January and ~2% MoM in February. The strengthening price trend was visible in other global markets. North Europe HRC prices increased ~6% MoM, while the US and Japan HRC prices rose ~3% MoM each, indicating a broad-based improvement in steel pricing across key regions.

Steel prices in India continue to rebound in February. Primary rebar prices rose ~7% MoM, supported by production shutdown at a key steel producer, tight supply of some sizes, and healthy demand from infrastructure projects. Domestic HRC prices increased ~3% MoM, aided by elevated raw material cost, reduced imports following the safeguard duty announcement, and improved market sentiments. However, the recovery in demand remains moderate, which limited further upside in prices. On the raw materials front, iron ore prices declined ~6% MoM in both China and Australia during February, reflecting softer input cost trends. Given the ongoing gas shortage, partly driven by supply disruption amid the escalating US–Iran conflict in the Middle East, galvanized steel prices are set to remain firm, due to supply constraints.

Broad non-ferrous metal rally pauses in February 2026: Following a rally in the previous month, the non-ferrous metals basket witnessed a correction, led by a ~4% MoM decline in LME lead and ~3% MoM fall in LME nickel prices, while LME aluminium declined ~2% MoM in February. Taking advantage of higher prices in the prior month, aluminium production increased in some provinces in China. However, as demand moderated during the month, the resulting excess supply exerted pressure on prices, with China inventory rising sharply. In contrast, LME copper prices remain stable MoM, while LME zinc was the only non-ferrous metal to register a gain, up ~3% MoM in February.

The ongoing Middle East conflict has introduced uncertainty in the global aluminium market, primarily due to vulnerability of the Gulf Cooperation Council (GCC) supply chain. As per International Aluminium Institute, the GCC region accounts for ~8% of global aluminium production. However, most smelters in the region rely on imported alumina and bauxite transported through the Strait of Hormuz and are heavily dependent on gas for power generation. If the conflict persists, it could tighten global aluminium supply and push the market further into deficit, thereby supporting higher LME aluminium prices. In contrast, India’s producers with relatively integrated operations and domestic raw material linkages are better positioned to benefit from a potential rise in aluminium prices.

Meanwhile, China alumina prices remain largely flat MoM, as global aluminium markets expect a supply squeeze in the up months, which could result in weaker demand growth for alumina. Additionally, healthy production levels from Australia continue to keep alumina prices in check.

Coal prices trend higher across markets: Coking coal prices in China reversed the declining trend in the previous two months, rising ~2% MoM in February, while Australian coking coal prices increased ~5% MoM during the same period. Thermal coal prices in China gained ~2% MoM after correcting in the prior two months, whereas South Africa’s thermal coal prices rose ~4% MoM. On a March-to-date basis, price trends have been mixed across markets. Coking coal prices in China have edged up ~1%, while Australia’s have declined ~10%. Similarly, thermal coal prices in China have increased ~6% MoM, while South Africa’s have surged ~14% MoM.

Thermal coal prices in Q4FY26 YTD have risen ~13% QoQ compared to Q3FY26 average, leading to higher input cost for sponge iron producers. As a result, seasonal buoyancy in long prices is set to sustain longer term. This dynamic is set to create a positive bias for primary long steel prices.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

.jpg)