Neutral Bajaj Finance Ltd for the Target Rs.900 by Motilal Oswal Financial Services Ltd

AI-led transformation; risk-disciplined growth

Balancing near-term asset quality with long-term platform-led compounding

* Bajaj Finance (BAF) is navigating the current credit cycle with a clear focus on balance sheet resilience, consciously sacrificing near-term growth to protect long-term asset quality. The tightening of underwriting in the MSME and unsecured segments reflects a proactive, cycle-aware risk strategy rather than reactive stress management.

* Growth moderated in FY26 due to MSME weakness, the run-down of the captive 2W/3W portfolio, and increased competitive intensity in housing. However, this moderation is self-induced and transitory, with growth expected to re-accelerate from FY27, driven by MSME normalization (with momentum expected to pick up in 2HFY27), secured product momentum, and cross-sell-led expansion. This is expected to foster a more efficient and profitable growth trajectory over time.

* BAF has adopted a more conservative stance on asset quality, with a clear emphasis on strengthening balance sheet resilience amid evolving stress in the MFI, unsecured, and MSME segments. Asset quality is approaching an inflection point, with early delinquency trends (3MOB/6MOB) improving across vintages. We expect credit costs (as a % of loans) to normalize to ~1.7-1.8% in FY27-28E (vs. 2.2%, including accelerated ECL provisions in FY26E), as legacy stress unwinds and tighter underwriting standards take effect.

* BAF’s LRS 2026-30 strategy marks a structural pivot toward a platform-led, AInative operating model that embeds intelligence across origination, underwriting, servicing, and collections—enhancing both risk selection and customer monetization. Although BAF originates a significant portion of incremental retail credit, its AUM penetration remains low across segments, indicating substantial monetization potential within its existing customer base.

* The franchise is transitioning from “scale-led expansion” to “productivityled compounding." Over FY26-30, the company expects to double its customer franchise to ~200-220m, scale app installs to ~160-180m, and meaningfully improve product-per-customer to ~6.5-7.5. This shift indicates a structural move toward a platform-led model characterized by higher cross-sell intensity, lower acquisition costs, and improved operating leverage. While near-term margins may remain range-bound, structural drivers around improvement in productivity and credit costs remain intact.

* We view BAF as entering a more mature, structurally stronger phase, defined by tighter risk controls, moderated but higher-quality growth, and increasing reliance on data/AI for competitive advantage. BAF trades at 3.7x FY27E P/BV and 20x P/E for a PAT CAGR of ~28% over FY26-FY28E and an RoA/RoE of 4.2%/21% in FY28E. We believe that the risk-reward is evenly balanced, and in the context of the near-term uncertainties, we reiterate our Neutral rating on the stock with a TP of INR900 (premised on 3.6x Dec’27E BVPS).

Growth outlook: Near-term reset, medium-term acceleration intact

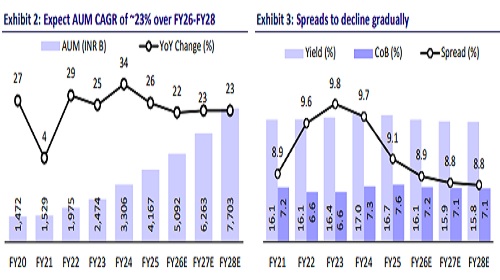

* BAF’s growth moderation reflects a strategic recalibration, not demand constraints evidenced by deliberate tightening in MSME and the run-down of lower-quality captive 2W/3W portfolios. AUM growth of ~22-23% in FY26 is a reset year, setting the base for a more durable growth trajectory. MSME growth, currently subdued, is expected to rebound to 20%+ after 2-3 quarters, contingent on sustained improvement in early delinquency trends.

* Secured segments particularly gold loans and new car finance are emerging as key growth anchors, offering better risk-adjusted returns. Cross-sell remains the most powerful structural lever, with the company shifting from acquisitionheavy (60:40) to engagement-led (40:60) growth, driving higher wallet share.

* BAF continues to operate with a relatively low market share across most lending segments (gold loans ~1%, new car financing ~1%, used car financing ~5%, secured business loans + LAP ~1%, and unsecured MSME and two-wheeler financing ~4% each). With market share across segments still in the low single digits, BAF retains significant headroom to scale without stretching risk.

* BAF remains focused on calibrated expansion, with new businesses being scaled up only where there is clear visibility on sustainable unit economics and riskadjusted returns. We build in ~23% AUM CAGR over FY26–FY28E, supported by segment recovery, cross-sell intensity, and customer base expansion.

AI as a core operating layer: Driving productivity, precision, and scale

* BAF is evolving into a fully integrated, AI-driven financial platform, with AI embedded throughout the entire value chain from sourcing to servicing. On the customer side, AI is enabling initiatives such as voice-to-text processing of ~20m calls, generation of ~100k customer offers, AI-driven marketing creatives, and conversational bots across multiple products. These advancements enhance customer acquisition, engagement, and conversion rates.

* On the operations side, AI is driving significant efficiencies through highaccuracy document processing (~95-96%), increasing automation in quality checks (targeting ~85-90%), and enabling disbursements and cross-sell opportunities via data analytics, while also delivering technology development efficiencies of ~25-45%.

* These initiatives are expected to structurally reduce operating costs, with the company targeting about a 50% reduction in operations and service expenses over the medium term, supported by higher digital adoption and automation. Consequently, cost ratios are expected to improve gradually, with the cost-toincome ratio declining to ~32% by FY28E (vs. ~33% in FY26E).

Risk and asset quality: From reactive clean-up to proactive risk architecture

* FY26 credit costs (at ~2.2%, including accelerated ECL provisions) reflect a confluence of cyclical stress and legacy portfolio drag, particularly in unsecured MSME and captive 2W/3W vehicle finance. The captive 2W/3W book (~1.1% of AUM but an outsized contribution to credit costs) is being systematically run down, with normalization expected by Sep’26. Early-stage delinquency indicators (3MOB/6MOB) are showing consistent improvement, signaling stabilization in newer vintages.

* Credit costs are expected to decline to ~1.8%/1.7% in FY27/FY28E, driven by tighter underwriting, improved vintage performance, and a portfolio mix shift towards secured lending.

* BAF also undertook accelerated ECL provisioning of ~INR14b in 3QFY26 to account for macro uncertainties and introduced minimum LGD floors across segments, leading to higher coverage ratios and stronger buffers against potential credit volatility.

* BAF is gradually repositioning toward a lower-risk balance sheet, supported by AI-led underwriting and real-time risk monitoring, with a medium-term target of GNPA below ~1.2% and NNPA below ~0.4%, reinforcing its positioning as a lowrisk and high-efficiency lender.

* Despite higher provisioning, credit costs are expected to remain within the guided range of ~165-175bp, supported by improving vintage performance, tighter underwriting, and proactive provisioning.

Valuation and view: Strong structural story; near-term overhang persists

* BAF is transitioning into a more mature phase of growth, characterized by tighter risk controls, moderated expansion in select segments, and a sharp pivot toward technology and customer monetization. This will enhance long-term earnings visibility and reduce cyclicality.

* While the stock has corrected sharply over the past one month, we believe ongoing global turmoil could result in near-term uncertainties, including potential prolonged stress in unsecured MSMEs (especially export-linked) and elevated credit costs over the next few quarters. Regulatory overhangs such as the NBFC-to-bank transition and leadership norms, as indicated in recent media reports could also weigh on the stock in the near term, despite the company’s succession planning currently being underway.

* Current valuations (~3.7x FY27E P/BV, ~20x P/E) are fair but not particularly compelling in the context of near-term uncertainties. We reiterate our Neutral rating on the stock with a TP of INR900 (premised on 3.6x Dec’27E BVPS)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041