Buy Bajaj Finance Ltd for the Target Rs.1000 by Motilal Oswal Financial Services Ltd

* Bajaj Finance’s (BAF) 4QFY26 PAT grew 22% YoY to ~INR55.5b (in line). Reported PAT for FY26 grew ~17% YoY to INR193b.

* 4Q NII grew 20% YoY to ~INR117.8b (in line). Non-interest income stood at ~INR24.3b (up 15% YoY). Opex grew ~22% YoY to ~INR48b (in line). PPoP stood at INR94b (in line), up 18% YoY. PPoP for FY26 grew ~18% YoY to ~INR355b. Annualized credit costs in 4Q declined to ~1.6% (PQ: ~1.9% excluding accelerated ECL provisions and PY: ~2.3%).

* BAF guided for ~22-24% AUM growth in FY27, supported by a steadily expanding customer base (~15-17m additions), along with continued investments in strengthening distribution and deepening penetration. Growth is expected to be driven by emerging segments, including gold loans, where rapid branch expansion is likely to support scale-up. Further momentum is expected from tractor and CV financing, while low market share across key portfolio segments will provide significant headroom for further growth.

* BAF has witnessed steady improvement in asset quality, with a sequential decline in Stage 2 and Stage 3 assets, and FY27 credit cost is guided at ~1.45-1.6.0%. Stress levels are normalizing, supported by disciplined underwriting and conservative provisioning practices. While MSME continued to trend weak, BAF guided that it has further pruned business in this segment and a gradual recovery is expected in MSME by 2HFY27. The captive 2W and 3W portfolio, contributing <1% of AUM but ~5% of credit costs, has been winding down and should further ease pressure on credit costs going forward.

* BAF remains fundamentally strong, supported by a well-capitalized balance sheet and diversified, broad-based growth across emerging lending segments. Its aggressive AI-led transformation stands out in the industry, with clear, measurable deployment, expected to enhance productivity, improve customer experience, and materially reduce operating costs. Growth is expected to remain well distributed across businesses, while credit costs are likely to moderate, aided by strong provisioning buffers.

* The stock trades at 4.2x FY27E P/BV and ~23x P/E. Despite a strong PAT CAGR of ~27% over FY26-FY28E and RoA/RoE of 4.1%/21% in FY28E, we see limited near-term upside catalysts in the absence of immediate triggers for a meaningful re-rating. We maintain our Neutral rating on the stock with a TP of INR1,000 (premised on 3.8x FY28E BVPS).

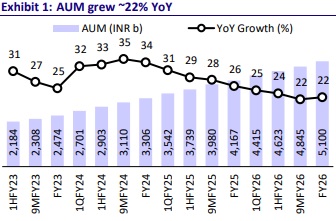

Stable AUM growth despite rising competitive intensity

* Total AUM grew 22% YoY/ 5.3% QoQ to INR5.1t. QoQ AUM growth was driven by Gold loans (+26%), Rural Sales Finance (+11%), LAS (5%) and Car Loans (+7%).

* New customer acquisition stood at ~3.93m in 4Q. The company added ~17.51m customers in FY26 and the total customer franchise rose to ~119.3m.

* 4Q NIM declined ~8bp QoQ to 9.5%.

* We expect BAF to deliver ~23% AUM growth over FY26-28E, with NIM of ~9.6% in FY27E/FY28E.

Improving asset quality signals strong visibility on credit cost moderation in FY27

* As of Mar’26, GNPA stood at 1.01% (down ~20bp QoQ) and NNPA at 0.41% (down ~5bp QoQ). PCR on Stage 3 assets stood at ~60% (PQ:61%).

* Management highlighted that 3 MOB, 6 MOB, and 9 MOB indicators are now below FY20 levels, signaling a meaningful improvement in portfolio quality and providing confidence that credit costs are likely to trend lower in FY27. We expect BAF’s credit costs to decrease sharply from ~1.9% in FY26 (before accelerated ECL provisions) to ~1.6%/1.5% in FY27E/FY28E.

Highlights from the management commentary

* The captive 2W and 3W portfolio, now contributing <1% of AUM, accounted for ~5% of credit costs in 4Q; this book is expected to wind down further to <INR15b by Sep’26, which will reduce credit costs incurred on this portfolio.

* BAF continues to invest deeply in customer centricity, aiming to increase wallet share through enhanced customer experience and engagement.

Valuation and view

* BAF reported a largely in-line performance in 4QFY26. AUM growth moderated to 22% YoY, reflecting calibrated business volumes in the MSME segment and the ongoing wind-down of the captive 2W/3W portfolio. NIM is expected to exhibit minor compression in the near-term. Asset quality is likely to exhibit an improvement ahead, aided by a more resilient balance sheet strengthened through accelerated ECL provisions. However, in the current uncertain macro-environment and considering the West Asia War, the impact on AUM growth and credit costs in the near term will remain key monitorables.

* The stock trades at 4.2x FY27E P/BV and ~23x P/E. Despite a strong PAT CAGR of ~27% over FY26-FY28E and RoA/RoE of 4.1%/21% in FY28E, we see limited near-term upside catalysts and the absence of immediate triggers for a meaningful re-rating. Maintain our Neutral rating on the stock with a TP of INR1,000 (premised on 3.8x FY28E BVPS).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041