Buy IIFL Finance Ltd for the Target Rs. 600 by Motilal Oswal Financial Services Ltd

* IIFL Finance (IIFL)'s NII in 4QFY26 grew 31% YoY to ~INR17.2b (inline). Other income stood at ~INR3.7b (14% miss) compared to INR4.1b in 3QFY26. This included assignment income of ~INR2.1b (PQ: INR2.8b).

* Net total income (NTI) in 4QFY26 grew ~50% YoY to ~INR20.9b (in line). Opex grew ~26% YoY to INR9.3b (in line) with the cost-income ratio declining to ~45% (PQ: 47% and PY: 53%). PPoP stood at INR11.6b and grew ~76% YoY (inline). PAT (post NCI) in 4QFY26 stood at INR5.9b (~10% beat). FY26 PAT (post-NCI) stood at INR16.6b (vs. INR3.8b in FY25).

* Calculated NIM contracted ~5bp QoQ to 6.7%. Credit costs stood at INR3.3b (~12% lower than MOSLe). This translated into annualized credit costs of ~1.9% (PQ: ~2.6% and PY: ~2.7%).

* Management indicated that income tax assessment orders for group entities have begun to come through, with the order for IIFL Finance expected over the next few days. The company does not anticipate any material adverse financial impact from these proceedings and maintains that there was no tax liability or evasion, and any adverse tax demand will be appropriately challenged by the company through the appellate forum.

* We raise our FY27 EPS by ~6% to factor in higher other income due to assignments/co-lending and slightly higher AUM growth. We have a BUY rating on the stock with a TP of INR600 (based on Mar'28E SoTP).

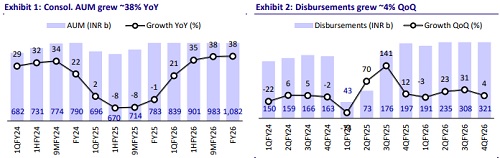

Consol. AUM rises ~38% YoY; strong 21% QoQ growth in gold loans

* Consol. AUM grew 38% YoY and ~10% QoQ to INR1.08t. On-book loans grew ~28% YoY. Off-book formed ~35% of the AUM mix.

* Sequential growth in AUM was primarily led by Gold loans (up 21% QoQ), which stood at INR526b, and MFI (up ~9% QoQ). Home loans grew just ~1% QoQ, while discontinued business AUM declined to INR26b (PQ: INR31b).

* Management highlighted that the business is now anchored around three core pillars: secured lending (primarily gold loans and mortgages) as the backbone of the portfolio; capital-efficient growth driven through co-lending and off-book partnerships with banks; and an AI-led operating model focused on enhancing productivity and strengthening risk control.

* The company shared that momentum in the gold loans has remained strong, with expectations of 20-25% gold loan growth, contingent on gold prices sustaining at current levels.

* Additionally, the housing business is at an inflection point, supported by a cleaner portfolio mix, with the company guiding for ~18-20% AUM growth and ~25-27% disbursement growth in this segment. We estimate gold loans/consolidated AUM to grow ~28%/~22% YoY in FY27 and a consolidated AUM CAGR of ~21% over FY26-28E.

GS3 declines ~15bp QoQ; sequential moderation in credit costs

* GS3 declined ~15bp QoQ to ~1.45%, while NS3 declined ~7bp QoQ to ~0.73%. PCR declined ~3pp QoQ to ~50.3%.

* Management shared that the company has consciously scaled down high-risk segments and strengthened its balance sheet, indicating a shift towards stable and controlled growth. The company expects credit costs to meaningfully decline in FY27 and has guided for credit costs of 1.5-1.7%. We model credit costs of 2.4%/2.2% for FY27/FY28 (vs. 2.8% in FY26).

* IIFL (Standalone) CRAR stood at ~17.8% as of Mar’26.

Highlights from the management commentary

* The company has fully complied with the revised gold loan guidelines, particularly for loans above INR250k, where detailed credit assessment and ongoing monitoring are mandated. It has implemented robust systems to conduct comprehensive credit evaluation for such loans.

* The MFI segment is showing improved collection efficiency and stabilizing asset quality, though growth remains calibrated with a focus on asset quality and stability.

Valuation and view

* IIFL reported a healthy quarter, driven by strong momentum in the gold loan segment amid robust demand and supportive gold prices, while the MFI business showed recovery with an improving growth trajectory alongside better asset quality. Asset quality improved across all segments, including MFI, and the company’s exit from riskier segments such as micro-LAP and personal loans led to a sequential decline in credit costs.

* We raise our FY27 EPS by ~6% to factor in higher other income from assignments and co-lending and slightly higher AUM growth. The stock trades at 1.2x FY27E P/BV and ~8x P/E for an estimated RoA/RoE of 2.7%/18% in FY28. We have a BUY rating on the stock with a TP of INR600 (based on SoTP valuation; refer to the table below).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041