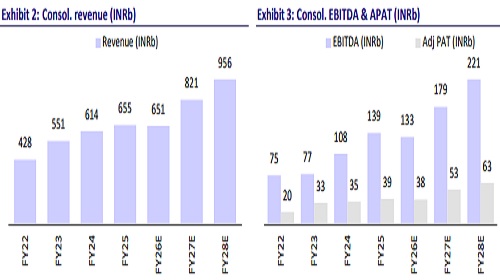

Buy Tata Power Ltd for the Target Rs.455 by Motilal Oswal Financial Services Ltd

Mundra SPPA nearly resolved; coal business provides upside

* Tata Power’s(TPWR) finalization of the Supplemental Power Purchase Agreement (SPPA) with Gujarat is a significant positive development, addressing the viability challenges of the Mundra plant. If the SPPA is adopted by all states, losses at Mundra are likely to reduce by 75% from the current INR17-18b p.a. This would lead to a 4.5- 5.5% upward earnings revision to our FY27/28 PAT estimates, as we currently factor in an annual net loss of INR7b at Mundra. Further, TPWR’s Indonesian coal business could provide an additional upside of 18% (annualised) to FY27 net profit for every USD10/t of additional realizations, driven by higher coal prices amid the Iran-Israel conflict.

* Beyond Mundra, TPWR’s continued strong performance in the Odisha and Delhi distribution businesses, as well as the rooftop solar segment, along with backward integration through a planned 10GW ingot/wafer manufacturing capacity, emerging distribution opportunities (e.g., Uttar Pradesh discom privatization), and an increased focus on expanding its own renewable energy capacity (amid declining third-party EPC installations) remain key growth drivers and catalysts for TPWR.

* We reiterate our BUY rating with a TP of INR455.

Mundra plant to restart as Gujarat SPPA has been finalized

* According to a press release issued by TPWR, the Government of Gujarat has approved the execution of an SPPA for the Mundra imported coal-based power plant. This development marks a significant step towards restarting the asset, which was previously operated under Section 11 of the Electricity Act, 2003, until Jun’25 and has remained non-operational since then.

* Gujarat, being the largest off-taker (~48% of 4.1GW), has finalized the SPPA with TPWR. We believe that under the proposed structure, the variable cost is expected to be largely fully passed through, even as the final commercial terms are still awaited. Based on our previous discussions, we anticipate a likelihood of tariff rationalization and/or sharing of coal-related gains. Subject to regulatory approval, the SPPA is expected to remain valid through 2038. ? In its current non-operational state, the Mundra plant incurs an annualized PAT loss of ~INR17-18b, excluding profits from the Indonesia coal mining joint venture.

* Following the full implementation of the SPPA, the loss is expected to significantly reduce to ~INR3-4b annually.

Benefiting from chaos: PAT upside potential from coal operations

* TPWR has exposure to coal mining through its stakes in the Indonesian ventures Kaltim Prima (30%) and BSSR & AGM (26%). Following the onset of the Israel-Iran conflict, coal prices have surged, and we estimate that realizations for the Indonesian coal business have spiked ~USD10/t on average. On an annualized basis, this translates to an 18% upside to our current FY27 PAT estimate.

Mundra to operate at full capacity under Section 11

* According to recent reports (link), the 4.1GW Mundra plant has been directed to operate at full capacity from 1st Apr’26 to 30th Jun’26 under Section 11, in response to the anticipated peak summer demand.

* For the remaining ~52% capacity tied to other states—Maharashtra, Punjab, Haryana, and Rajasthan—operations are expected to continue under Section 11 in the near term, with a likelihood of transitioning to arrangements broadly aligned with the Gujarat SPPA framework.

* Mundra plant is currently non-operational and is incurring a net loss of ~INR4b every quarter. However, under section 11, the losses are likely to dip 75%.

Valuation and view

* The valuation of TPWR is segmented across various business units, leading to a TP of INR455.

* The regulated business is valued using a 2.5x multiple on the regulated equity.

* The coal segment is valued at 1x book value. ? The renewables segment is valued at 12x FY28E EBITDA.

* The pumped storage segment and other segments are valued at 1x P/B. Cash and investments add INR37/share.

* The sum of these contributions results in a TP of INR455/share, reflecting the comprehensive valuation of TPWR’s diverse business segments.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041