Neutral PowerGrid Ltd for the Target Rs.302 by Motilal Oswal Financial Services Ltd

Leading India's transmission buildout

We attended the analyst meet hosted by PowerGrid (PWGR), where management updated investors on execution progress and the sizeable pipeline opportunity. Following were our key takeaways:

* Management has raised FY26 capex/capitalization guidance to INR350b/INR250b, from INR320b/INR220b guided in Feb’26.

* The Central Electricity Authority’s (CEA) transmission plan for renewable energy (RE) integration outlines a pipeline of INR7.9t till FY36. Including incremental opportunities such as the Brahmaputra basin (~INR4t) and prospective HVDC interconnections with countries such as Oman, UAE, and Saudi Arabia (~INR3-4t), the overall addressable pipeline expands to ~INR15t. With an estimated ~50% share for PWGR, this translates into a long-term bid pipeline of ~INR6–7.5t (~INR600b annually), providing a multi-year structural tailwind.

* Execution momentum in the country has picked up sharply, with transmission line/transformation capacity additions beating targets by 56%/71% in Jan–Feb'26, after missing targets for most of FY26.

* A robust HVDC pipeline is emerging, with Bikaner-Begunia and Barmer–South Kalamb expected to be awarded in the near to medium term. ? Rising capex commitments are expected to weigh on shareholder returns; we expect DPS to remain flat or witness a modest cut. We value PWGR based on Dec’27 BVPS and a P/B multiple of 2.5x; reiterate our Neutral rating.

Upward revision in capex and capitalization guidance for FY26

* PWGR has raised its capex/capitalization guidance for FY26 to INR350b/INR250b from its 3QFY26 guidance of INR320b/INR220b.

* The revised target is significantly higher than the initial guidance of INR280b/INR200b provided in 3QFY26.

* Capitalization and capex guidance for FY27/28 remained unchanged at INR300b/INR350b and INR370b/INR450b, respectively.

* Management indicated that the capex guidance is based on the works in hand, and further project wins could lead to an upward revision.

India’s multi-trillion capex opportunity continues to unfold

* The CEA’s transmission plan for RE integration outlines projects worth INR7.9t till FY36. After including the Brahmaputra basin (INR4t till FY36) and prospective HVDC interconnections with countries such as Oman, UAE, and Saudi Arabia (INR3t-4t), PWGR estimates the overall project pipeline at ~INR15t.

* Assuming PWGR secures 50% of these opportunities, its pipeline over the next decade stands at INR6t–INR7.5t (~INR600b annually).

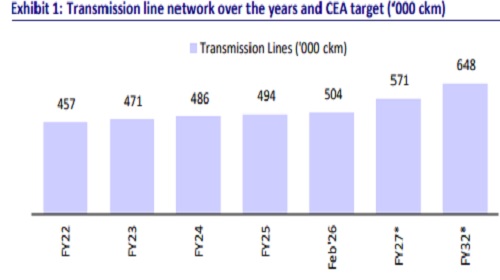

* The NEP targets 648.2k ckm of transmission network and 2,411.9 GVA of transformation capacity by FY32, implying a 4.3%/9.1% CAGR in lines/transformer capacity over FY26–32, against Feb'26 actuals of 503.7k ckm/1,428.9 GVA, respectively.

Robust HVDC pipeline underpins PWGR's growth outlook

* HVDC lines, Bikaner-Begunia and Barmer-South Kalamb, are expected to be awarded in the near to medium term.

* Other major HVDC projects include the Madurai-Mannar HVDC line and the Paradwip-Andaman undersea HVDC line, although bidding timelines for these projects remain uncertain.

* The CEA's Brahmaputra Basin Master Plan envisages ~21,000 ckm of HVDC lines in the region, representing a total opportunity of INR6.4t.

* The OSOWOG initiative creates an additional pipeline for mega undersea HVDC projects (India-UAE/Saudi Arabia, India-Singapore, etc).

* PWGR is currently executing the Khavda-Nagpur HVDC line, while the PangKaithal project remains on hold as management evaluates the conversion of the project to AC

Execution challenges easing on most fronts

* PWGR has historically faced execution headwinds related to RoW acquisitions, availability of skilled manpower, and supply-side constraints in transformers and reactors—all of which are now largely being addressed.

* Under the new RoW guidelines, the government has revised land compensation values, thereby lowering execution risk. Management does not foresee material challenges in this area going forward.

* PWGR has operationalized five skill development centers in India and eventually scaling up to seven, capable of training ~1,400 technicians annually.

* Supply constraints in transformers and reactors are also easing, supported by the rapid expansion of domestic manufacturing capacity.

Dividend payout likely to moderate as capex rises

* PWGR recorded an average dividend payout ratio of 68.3% over FY22-24, which moderated to 62.9% in FY25. We are building in a DPS of INR9.6/INR10/INR11 (implying payout ratios of 53%/52%/54%) for FY26/27/28.

* However, downside risks persist, with dividends potentially remaining flat or witnessing a modest moderation

Valuation and view

* We derive our TP of INR302 for PWGR based on Dec’27 BVPS and a P/B multiple of 2.5x (unchanged).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041