Add Hero MotoCorp Ltd For Target Rs. 5,082 By Yes Securities Ltd

Steady operating performance

View – EVs ramp-up ahead while market share gains on ICE to watch for

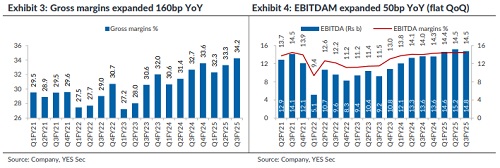

HMCL’s 3QFY25 results were steady and in-line to our/street with EBITDA margins expanded 50bp YoY (flat QoQ) at 14.5%. This was constrained by EV (margin drag of ~150bp) as underlying ICE margins were healthy at 16% (vs 16.5% in 2Q, 16.4% in 1Q, 15.6% in 4QFY24), supported by benign RM, favorable revenue mix, cost savings and price hikes. However, ~50bp QoQ decline in ICE margins was led by seasonally higher A&P spend in 3QFY25 which is expected to normalize. ~1.3% QoQ increase in ASP was led by favorable mix, ~7% QoQ increase in spares revenues with contribution at ~15.2% (vs ~13.9% in 2Q, 12.5% in 1Q and vs 14.7% in 3QFY24). The management indicated recent tax relief to reflect positive for demand sentiments which can aid current rural momentum.

Stock performance

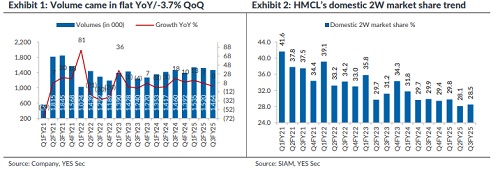

Going ahead while the management remain confident of broad-based volumes recovery within 2Ws, HMCL is aiming at market share expansion especially in the premium segment led by new product launches. The recent new product launches in the scooter (125cc and 160cc) should help improve positioning and market share gains. Within EVs too, HMCL to see market share perking up led by rebuilding of channel inventory post introduction of V2. Maintain ADD with revised TP of Rs5,082 (vs Rs5,000) based on ~18x Mar’27 S/A EPS plus Rs130 for Hero FinCorp. Management’s action to overhaul brand strategy supported by Ather’s continued brand acceptance provide an additional lever for the stock. We raise FY26/27 EPS by ~2% to factor in for higher other income and ASPs and build in revenue/EBITDA/Adj.PAT CAGR of ~10% over FY24-27E.

Result Highlights – Highest ever ASP and EBITDA/vehicle

* Revenues grew 5% YoY (-2.4% QoQ) at Rs102.1b (est ~Rs101.3b) as volumes/ASP grew 0.3%/+4.7% YoY and -3.7%/+1.3% QoQ respectively at ~1.46m units and ~Rs69.8k/unit (est ~Rs69.2k/unit). Spares (SPAM) revenues grew ~9% YoY (+6.7% QoQ) to Rs15.55b with share in revenues at 15.3% in 3Q (vs 13.9% in QoQ and 14.7% YoY). Gross margins came in better at 34.2% (+160bp YoY/+90bp QoQ). However, this was partially offset by higher staff cost at ~Rs6.6b (est Rs6.5b, +1.3% QoQ) and other exp. at ~Rs13.6b (est ~Rs12.8b, +3.2% QoQ).

* Consequently, EBITDA grew 8.4% YoY (-2.6% QoQ) at ~Rs14.8b (est Rs14.8b, ~cons Rs14.5b), leading to margins expanding by 50bp YoY (flat QoQ) at 14.5% (est 14.6%, cons 14.2%). ICE business margins came in at ~16% (vs ~16.5% in 2Q and ~16.4% in 1QFY25) led by positive mix, benign RM and LEAP savings of ~120bps in 3Q. QoQ decline in ICE margins was led by seasonal A&P spends. EBITDA/vehicle came in at ~Rs10.1k/vehicle (+8.1% YoY/+1.1% QoQ).

* Adj.PAT grew by 12.1% YoY (flat QoQ) at Rs12b (est Rs11.5b). 9MFY25 Revenues/EBITDA/Adj.PAT grew 10.3%/14.3%/14.9%.

CHARTS

Please refer disclaimer at https://yesinvest.in/privacy_policy_disclaimers

SEBI Registration number is INZ000185632