Accumulate Hero MotoCorp Ltd for the Target Rs.6,300 by PL Capital

Quick Pointers:

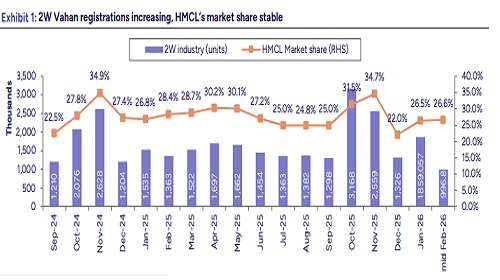

* Oct’25-Jan’26 retail sales grew 19.4% YoY, in line with industry

* First-time buyers increased to ~80% of total buyers in Jan’26 vs. avg of ~75%

HMCL has ample headroom for growth in scooters (including EVs), global markets, premium motorcycles and PAM business. The company is stepping up capacities and marketing campaigns led by the improvement in rural sentiments post good monsoon/ reservoir levels, festivities and wedding season in Q3FY26; sentiments are expected to remain positive in the upcoming months. However, some challenges might moderate the industry growth post H1FY27 and need to be monitored. We estimate volume/ realization CAGR of 5.7%/3.6% over FY25-28E translating into revenue/EBITDA/APAT CAGR of 9.5%/10.8%/10.1%. Retain ‘Accumulate’ rating with TP of Rs6,300 (previous Rs6,575). We value the core business at P/E of 20x (previous 21x) Sep’27E and its stake in Hero FinCorp at Rs50 and Ather Energy at Rs300.

Domestic scooter dispatches grow by 45.6% YoY Apr’25-Jan’26: It outpaced the industry growth of 15.2%, and we see this momentum continuing with strong urban sentiments, increasing women’s workforce participation and utility across family members. HMCL’s scooters have a lean inventory as per our channel checks with some models/variants having 2-3 months waiting period even as demand remains high. Its e-2W market share has been stable, at 10.8% (+610bps YoY) in Q3FY26, as realizations and unit economics improve. In contrast, domestic motorcycles (~85% of overall volumes) grew by 2.5% YoY, tad lower than the 4.1% industry growth. Although we note strength in recent months with Nov’25-Jan’26 sales growing by 28.2% vs. industry growth of 23.6%, led by marketing campaigns and model refreshes/ upgrades. Market share of Deluxe 100cc stood at 90.7% (+390bps YoY) and Deluxe 125cc at 18.5% (+100bps QoQ). HMCL increased its Premia network to 106 stores, covering >50% of the domestic premium industry footprint. Its overall inventory was 4-5 weeks in Q3FY26 vs. 6-7 weeks in both Q3FY25 and Q4FY25, which should augur well for the stock as we expect it to build inventory as replacement demand is anticipated to kick in.

Global business dispatches grow by 41% YoY in Q3FY26: HMCL’s market share in exports stood at 7.5% (+90bps YoY) as the company kept growing faster than the industry, expanding its footprint to 52 countries across 5 continents with Euro5+ compliant models. It continues to gain share across key markets with its premium portfolio contributing to ~40% of global volumes.

Weaker monsoon may dampen rural demand in CY26: With CY26 expected to see lower-than-average rainfall, rural cashflows may be impacted, directly affecting entry level motorcycle demand. Continued commodity inflation, INR depreciation and new regulations can drive prices higher (or reduce discounts), offsetting the benefits received from GST rate cuts. Further, a high base may lead to moderate industry-wide growth in H2FY27, posing downside risks to the stock.

Above views are of the author and not of the website kindly read disclaimer