Buy Tata Consultancy Services Ltd for the Target Rs.4,040 by PL Capital

Steady performance, multiple one-offs impact bottom line

Quick Pointers:

* Marginal beat in revenue with steady operating margin

* Deal wins of USD 9.3 bn compared to USD 10 bn in Q2

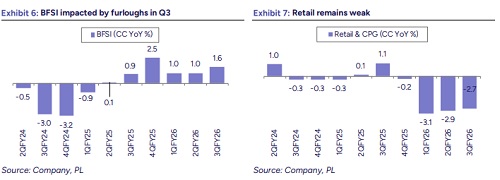

The revenue performance (+0.8% QoQ CC) exceeded our estimates (+0.5% QoQ CC), aided by broad-based growth, international business was up 0.4% QoQ CC. Beyond furloughs, the growth momentum within BFS was steady and should rejoin the positive growth trajectory from Q4. The pockets of weakness is visible in certain sub-segments of Retail and Manufacturing, while essential and non-Automotive delivered healthy performance. The slowdown in legacy offerings is partly compensated against strong uptick in AI revenue stream, which reported annualized revenue run-rate of USD1.8bn (+17.3% QoQ CC). The management was confident of sustaining international revenue growth in the coming year on the back improving visibility in North America and continued momentum within key pockets. Given the low base of revenue in FY26 and steady recovery within international business, we expect 5.4% USD revenue CAGR over FY26-28E. On the margins, the compensation revision is behind, while we also anticipate the residual headcount trimming exercise to be executed in Q4. Hence, we are revising FY26E/FY27E/FY28E, adjusting operating margin up by 10bps/20bps/10bps respectively. We assign 23x to FY28E EPS that translates a TP of 4,040. Maintain BUY

Revenue: TCS’s Q3 performance marginally beat both our and consensus estimates despite furlough-related headwinds. Revenue stood at USD 7.5 bn, up 0.8% QoQ CC, compared with our and consensus expectations of ~0.5% QoQ CC growth. Growth was largely broad-based, except in BFSI and Technology. Geographically, India and MEA led the performance, posting 8.0% and 3.2% QoQ CC growth, respectively, while the international business grew 0.4% QoQ CC.

Operating Margin: EBIT margin remained steady at 25.2% during the quarter. The margin walk reflected tailwinds from pyramid optimization (+80 bps) and currency depreciation (+20 bps), which were offset by headwinds from wage hikes (-50 bps) and elevated marketing expenses (-50 bps). Reported PAT was impacted by multiple one-offs, including restructuring expenses, provisions for legal claims, and provisions related to changes in the new labour laws.

Deal Wins: TCS won deal wins of USD 9.3 bn were within the comfort band. Deal win included a mega deal in BFSI, North America. BFSI, Retail & North America TCV came at USD US$3.8 bn (18.7% QoQ), US$ 1.4 bn (-22% QoQ) & US$ 4.9 bn (13.9% QoQ) respectively with steady LTM BTB of 1.4x

Valuations and outlook: We estimate USD revenue/earnings CAGR of 5.4%/14.5% over FY26E-FY28E. The stock is currently trading at 18.4x FY28E earnings, we are assigning P/E of 23x to FY28E earnings with a target price of INR 4,040. We maintain “BUY” rating.

Above views are of the author and not of the website kindly read disclaimer