Buy Tata Consultancy Services for the Target Rs.3,350 by Choice Institutional Equities

View & Valuation: TCS delivered a strong Q4FY26 beat, with resilient execution and robust deal wins (USD 12 Bn Q4 TCV; USD 40.7 Bn FY26) reinforcing growth visibility despite a soft macro backdrop. AI is emerging as a key growth driver, with revenues at a USD 2.3bn annualised run-rate and deployments scaling up across enterprises into FY27. Although the 26% EBIT margin target has shifted to the longer term, TCS’s strong profitability continues to provide room for reinvestment in AI, data centres and strategic growth initiatives. We believe, TCS to deliver Revenue/EBIT/PAT CAGRs of 8.6%/10.0%/12.3% over FY26– FY29E, driven by improving demand conversion and operating leverage. Hence, we maintain our BUY rating with a target price of INR 3,350, based on FY28E EPS of INR 176.2 in line with our earlier upward revision of the target price from INR 3,275 to INR 3,350 in the Q4FY26 preview

Q4FY26 Revenue Better than Estimate; Deal Wins Momentum Continue

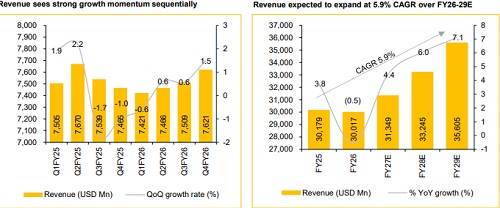

* TCS reported Q4FY26 revenue of USD 7.6 Bn, up 1.5% QoQ (vs CIE est. 0.7%), with CC growth of 1.2% QoQ. In INR terms, revenue stood at INR 706.9 Bn, rising 5.4% QoQ (vs CIE est. 3.0%). For FY26, revenue came in at USD 30.0 Bn, down 0.5% YoY (vs CIE est. -0.7%), while CC revenue declined 2.4% YoY. In INR terms, FY26 revenue stood at INR 2,670.2 Bn, up 4.6% YoY (vs CIE est. 4.0%).

* EBIT margin came in at 25.3% for the quarter (in line with CIE estimate).

* In absence of one-offs such as Labour Code change, charges and restructuring expenses incurred in Q3, the reported PAT stood at INR 137,180, up 28.7% QoQ (vs CIE estimate of 27.7% QoQ growth).

Robust TCV Performance and AI-led Execution Reinforce FY27 Confidence TCS reported a strong TCV of USD 12.0 Bn for Q4 and USD 40.7 Bn for the full year, propelled by five mega deals and a strategic shift towards vendor consolidation and AI-led transformation. Vertical performance was characterised by continued growth momentum in BFSI despite macro-caution, an all-time high TCV in Consumer business driven by major renewals such as Marks & Spencer and first-ever mega deal in CMI segment as it prepares for a rebound. Management has maintained a positive outlook for FY27. AI services have already reach a USD 2.3 Bn in annualised revenue. This will be net-accretive to overall growth as client inquiries transition into scaled deployment and structural headwinds move behind them

AI Conversion Starts to Accelerate AI−led services were supported by the Hypervault business's progress towards 1GW of infrastructure capacity through strategic partnerships with OpenAI and AMD. Moving into FY27, the management is confident in its "infrastructure to intelligence" strategy, expecting AI deployment to be net-accretive to growth as the company pursues its aspiration to become the world’s largest AI-led technology services firm.

Margin Strength Provides Room for Strategic Investments EBIT margin stood at a four-year high of 25% and Q4 margin improved sequentially to 25.3%. Margin gains were supported by better realisation and currency tailwinds, partly reinvested into AI capability building, partnerships and strategic growth initiatives. While annual wage hike from April pose a near-term headwind of 150–200 bps, which is expected to offset through operational efficiencies and pyramid optimisation. Management aspires a 26% margin aspiration while continuing to invest in future growth drivers.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131