Buy Tata Consultancy Services for the Target Rs.3,000 by Motilal Oswal Financial Services Ltd

Valuations are cheap, but near-term catalysts limited

TCS reported 4QFY26 USD revenue of USD7.6b, up 1.2% QoQ in CC (0.8% in organic cc terms), largely in line with our estimate of 1.5% growth. FY26 revenue declined 2.4% YoY CC. 4Q growth was led by ENU/consumer business (up 6.1%/2.8% QoQ CC). Manufacturing /technology & services/regional markets grew 1.2%/1.0%/1.2% QoQ CC. EBIT margin was 25.3% (up 10bp QoQ), in line with our estimate of 25.1%. For FY26, EBIT margin stood at 25% vs. 24.3% in FY25. Adj PAT was up 2.2% QoQ/12.2% YoY at INR138b, in line with our est. of INR138b.

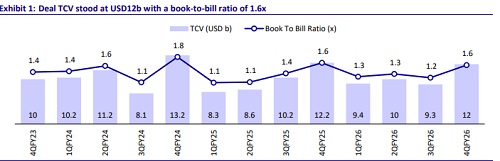

In INR terms, FY26 revenue/EBIT/adj. PAT grew 4.6%/7.5%/8.8% YoY. Cash flow from operations stood at 111.0% of net profit for FY26. FY26 ROE came in at 52% (vs. 52%/51%/47% in FY25/FY24/FY23). In 1QFY27, we expect revenue/EBIT/adj. PAT to grow 13.3%/ 14.4%/9.3% YoY. TCS reported a deal TCV of USD12b, up 29% QoQ and down 2% YoY, bringing FY26 TCV to USD40.7b (vs FY25 TCV of USD39.4b). The book-to-bill ratio was stable at 1.4x. We reiterate our BUY rating on TCS with a TP of INR3,000, implying a 16% potential upside.

Our view: Growth remains patchy; margins likely to stay flat

Another year of underperformance: TCS revenue was up 0.8% in organic QoQ cc terms, largely registering an uneventful quarter. While deal wins remained strong, this marked an end to a poor FY26 – TCS revenue declined 2.4% YoY CC (international business in FY26 grew only ~0.5% YoY CC), underperforming all large-caps (see exhibit 3 - organic YOY cc growth performance for past five years).

Industry-leading margins, but growth continues to elude: TCS has again managed to maintain its industry-leading EBIT margins of 25%. However, despite INR depreciation and improvement in revenue per employee, margin expansion remains underwhelming, with most benefits being reinvested or passed through in a cautious demand environment. We believe continued investments in talent, capability building, partnerships, and GTM are likely to keep margins range-bound, and we expect ~25.0% margin for FY27.

Growth was led by ENU; Communications remained soft: 4Q growth was led by ENU/Consumer (up 6.1%/2.8% QoQ CC), while Manufacturing/ Technology grew 1.2%/1.0% and Communications declined 0.4%. Manufacturing demand stayed cautious due to macro, supply chain, tariff and EV-related issues. Consumer delivered another strong quarter, led by UK/EMEA retail and travel, supported by market share gains. North America remained weak.

Revenue per employee improving, but most benefits being passed on to clients: TCS's revenue per employee inched up again, marking another quarter of admirable improvement. However, it is telling that despite INR depreciating by ~5% against USD on a realized basis and ~8% productivity gains, incremental margins have seen only modest flow-through. We believe a muted demand environment and AI deflation are sucking up all productivity benefits.

Hypervault strategy starting to take shape; timelines remain unclear: Hypervault has made progress this quarter, including customer commitments, land parcel finalizations and partnering agreements. Engagements with hyperscalers and model providers have also moved beyond early exploration into structured programs. TCS also announced a 100MW build-out with OpenAI (with an option to scale up), with demand converging around large AI workloads (100-200MW per customer). However, timelines remain unclear.

Revenue and margins largely in line with estimates; deal wins up 30% QoQ

* USD revenue came in at USD7.6b, up 1.2% QoQ in CC (0.8% in organic cc terms), largely in line with our estimate of 1.5% growth. FY26 revenue declined 2.4% YoY CC.

* In terms of geographies, India was up 1.7% QoQ CC, whereas North America/UK were up 1.4%/2.4%. Annualized AI services revenue stood at USD2.3b in 4Q, up 27% QoQ.

* 4Q growth was led by ENU/Consumer business (up 6.1%/2.8% QoQ CC). Manufacturing/Technology & Services/Regional markets grew 1.2%/1.0%/1.2% QoQ CC.

* EBIT margin was 25.3% (up 10bp QoQ), in line with our estimate of 25.1%. For FY26, EBIT margin stood at 25% vs. 24.3% in FY25.

* TCS reported a deal TCV of USD12b in 4Q, up 29% QoQ/down 2% YoY, bringing FY26 TCV to USD40.7b (vs FY25 TCV of USD39.4b).

* Adj PAT was up 2.2% QoQ/12.2% YoY at INR138b (in line with our est. of INR138b).

* Cash flow from operations was strong at 111.0% of net profit for FY26. FY26 ROE stood at 52% (vs. 52%/51%/47% in FY25/FY24/FY23).

* The net headcount increased by 2,356 employees to 584,519 (up 0.9% QoQ) in 4Q. Attrition (LTM) increased by 20bp QoQ to 13.7%.

* The board declared a final dividend of INR31/share.

* Key highlights from the management commentary

* Enterprises are navigating increasing complexity across technology, operating models, and business transformation, making the role of trusted system integrators more critical. Clients are seeking partners with deep technology expertise, strong domain context, and end-to-end accountability.

* The company invested significantly in strengthening AI partnerships across enterprise platforms, hyperscalers, deep-tech, AI-native, and domain-specific players, including partnerships with ServiceNow, Google Cloud, and ABB.

* Management remains positive about the FY27 outlook, particularly for international business growth. 1QFY27 and 2QFY27 are expected to follow typical seasonality and be stronger than 4QFY26.

* The geopolitical impact remains largely restricted to the Middle East and certain segments like travel and transportation.

* Transformation budgets are broadly divided into three buckets: (1) enterprise transformation (cloud, data modernization, cybersecurity, ERP upgrades), (2) AI-led modernization (tech debt reduction enabled by AI), and (3) pure-play AI transformation across industry value chains.

* Enterprises currently lack the required stack readiness for scaled AI deployment; hence, spending is directed toward infrastructure upgrades, application modernization, and data foundation building.

* Client metrics improved, with an increase in accounts generating over USD100m in revenue, indicating greater stability and willingness for large transformation programs.

Valuation and view

We expect USD revenue/EPS to compound at ~3.8%/~7.0% over FY26-28, reflecting gradual recovery, with growth continuing to come from select pockets rather than a broad-based pickup. Margins improved somewhat less with productivity gains and INR tailwinds largely being reinvested or passed through and we expect margins to remain flat in FY27. We keep our estimates largely unchanged and reiterate BUY with a TP of INR3,000, based on 18x FY28E EPS, implying ~16% upside.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041