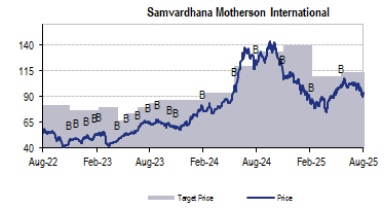

Buy Samvardhana Motherson International Ltd for the Target Rs. 1,320 by JM Financial Services Ltd

In 1QFY26, SAMIL reported a consolidated EBITDA margin of 8.1% (-150bps YoY), 100bps below JMFe. Margins were impacted by structural challenges in the EU, upfront booking of tariff associated costs, and start-up costs from greenfield projects. Despite subdued global light vehicle demand, SAMIL continues to outperform, driven by higher content per vehicle owing to premiumisation. The company does not expect a material tariff impact, as most US sales are USMCA-compliant, while discussions with customers are on-going for the remainder. Although the management remains silent on the EMS business, we expect it to contribute meaningfully to revenue from FY27 onwards. Near-term margin pressures are likely to persist, given weak demand in developed markets and ramp-up costs from greenfields. Therefore, we lower our EBITDA margin estimates by 20bps/30bps for FY26E/FY27E. We maintain our BUY rating with a Mar’27 TP of INR 110 (19x FY27E EPS). Recovery in global LV demand remaining a key monitorable.

* 1QFY26 – Margin below JMFe: SAMIL reported consol. net sales of INR 302bn (+5% YoY, +3% QoQ), c.3% below JMFe. EBITDA stood at INR 24.5bn (-11%YoY, -7% QoQ), 13% below JMFe. EBITDA margin stood at 8.1% (-150bps YoY, -90bps QoQ), 100bps below JMFe, due to higher employee costs. Margin for Wiring Harness, Modules & Polymer, Vision Systems, Integrated Assemblies, Emerging businesses improved / (declined) YoY by -30bps / -230bps / -30bps / +120bps / -390bps to 11.4% / 6.4% / 9.2% / 11.4% / 8.4%. Consol. adj. PAT for 1Q was INR 6.5bn (-35% YoY, -38% QoQ), 38% below JMFe, due to lower-than-expected other income and higher-than-expected depreciation

* Demand and margin outlook: SAMIL highlighted a challenging automotive production environment. Global light vehicle (LV) volumes grew 2% YoY in 1QFY26, with emerging markets expanding while developed markets contracted. CV volumes remained flat and followed a similar trend across regions. Despite this, SAMIL delivered YoY revenue growth, supported by its diversified portfolio and recent acquisitions. The modules and polymers business was impacted by structural issues in the EU and consolidation costs; however, recovery is expected in 2H, driven by multiple EV launches in the EU and ongoing restructuring measures. Exports to the US from India were less than USD 10mn in 1Q. The company does not anticipate a material impact, as most US sales are USMCAcompliant and discussions are underway with customers to pass on the remainder. SAMIL will provide further updates at its Investor Day in Sep’25.

* Update on acquisitions: Atsumitec revenue for the quarter stood at INR 7bn. Additionally, integration benefits are expected to yield results in the next few quarters. Excluding Atsumitec, inorganic revenue grew 2% YoY

* Non-automotive segment: In the consumer electronics business (JV with BIEL Crystal), the ramp-up of capacity to 15–17 million units by FY26-end remains on track, with the company indicating no signs of slowdown from the customer end. Additionally, it has received customer approval for a plant scheduled to commence SOP in 2QFY26. The aerospace segment was impacted as 1Q is seasonally weak. Overall, with the ramp-up in production, the company anticipates a strong performance in 2H.

* Other highlights: 1) Effective net debt increased from INR 97.9bn (Mar’25) to INR 112.3bn (Jun’25). Net Debt/EBITDA stood at 1.1x (0.9x in Mar’25). 2) Capex during the quarter was INR 12bn. FY26 capex guidance stands maintained at INR 60bn (+/-10%). 3 greenfields have operationalized during 1Q and 11 are at various stages of completion – 7 in India, 2 in UAE, and 1 each in China and Poland. 3) Working capital remained elevated during the quarter due to tariffs/geopolitical issues and regulatory payments.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361