Buy Swiggy Ltd for the Target Rs. 550 by Motilal Oswal Financial Services Ltd

Preparing for battle, again

Dark store operating leverage aids margins, but competitive risks loom ahead

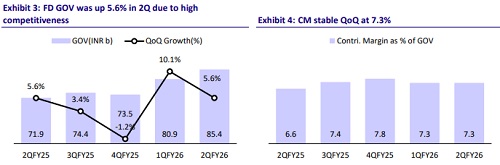

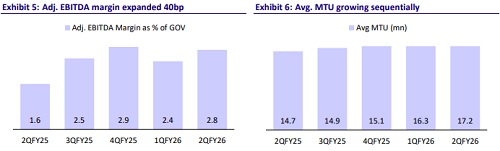

* Swiggy delivered a revenue of INR55.6b in 2QFY26 (up 12.1% QoQ) vs. our estimate of INR54.6b. The food delivery (FD) business’s GOV grew 18.7% YoY, whereas the contribution margin (CM) remained stable at 7.3%. FD’s adj. EBITDA as a % of GOV margin improved 40bp QoQ to 2.8% vs. our est. of 2.7%.

* Instamart’s GOV was INR70.2b (up 107% YoY) vs. our estimate of INR 69.7b. The contribution margin expanded 200bp QoQ to -2.6%. Adjusted EBITDA as a % of GOV was -12.1% (-15.8% in 1Q), above our estimate of -13.8%.

* Overall, Swiggy posted a net loss of INR11b, marking an increase of 75% YoY.

* For 1HFY26, revenue/adj. EBITDA loss grew 54%/118% YoY. For 2HFY26, we expect revenue to grow 48%, while the adjusted EBITDA loss is expected to decline 15% YoY. The combination of steady FD growth, rising Instamart AOV, and easing fixed-cost drag enhances the visibility of positive unit economics. We value the FD business at 30x FY27E adjusted EBITDA and QC using DCF. We reiterate our BUY rating on Swiggy with a TP of INR550, implying a potential upside of 31%.

Our view: Competition to pick up, but decent operating leverage as new dark stores ramp up

* Cash burn reduces in Qcommerce, breakeven expected by 1QFY27: Both CM and adj. EBITDA for the quick commerce business improved QoQ (CM improved 200bp, and adj. EBITDA margin expanded 370bp). This, coupled with lower capex, reduced the absolute cash burn in Instamart by 50% QoQ.

* Competitive intensity high, again: Contrary to last quarter, when most players alluded to reducing competitive intensity, both Eternal and Swiggy now expect heightened competition going forward. We believe this period will be similar to the one we saw last year (2HFY25) in terms of marketing/branding costs. However, one key difference is that the dark store investment pace for most players (especially Swiggy) will be far lower than last year, which saw heightened capex as well as opex (in partner stores). Hence, there is still room for margins to expand. We expect Instamart to reach contribution breakeven by 1QFY27 (in line with company guidance).

* FD growth in line, but QoQ growth indicates some market share loss: Swiggy's GOV grew by 5.6% QoQ, a tad slower than Eternal, indicating some market share loss. The company has managed to increase marketing expenses in response to Eternal as both players fight in a slowing FD market. Adj. EBITDA margin, however, improved sequentially, and we expect linear improvement (5% of GOV in the next three years).

* INR100b QIP fundraise to shore up defenses: Swiggy plans to raise INR100bn. Its current cash balance is INR46b, and its current burn rate, albeit reducing, gives it a runway of 6-7 quarters, in our opinion. It also expects to net INR25b from its Rapido stake sale. Thus, the fundraise is to shore up its defenses in an intense Qcommerce battle amongst the top 3 players as well as new entrants.

Valuation and view

* We believe Swiggy is entering a phase of profitability, supported by operating discipline and improving network efficiency. The combination of steady FD growth, rising Instamart AOV, and easing fixed-cost drag enhances the visibility of positive unit economics.

* Steady improvements in AOV, dark store throughput, and take rates could lead to a material re-rating in profitability, prompting a more constructive stance on the stock.

* We value the FD business at 30x FY27E adjusted EBITDA and QC using DCF. We have brought forward our profitability assumptions for Instamart. We reiterate our BUY rating with a TP of INR550, implying a potential upside of 31%.

In-line FD GOV growth and beat on Instamart’s adj. EBITDA margin

* Swiggy reported a 2QFY26 net revenue of INR55.6b (+12.1% /54.4% QoQ /YoY) vs. our estimate of INR 54b.

* FD GOV was INR85.4b (up 5.6%/18.7% QoQ/YoY) vs. our estimate of INR86.5b.

* Instamart GOV came in at INR70.2b (up 107% YoY) vs. our estimate of INR 69.7b. Dark store rollouts with 40 new active Dark stores in 2Q. Half of the dark stores were megapods.

* For food delivery, adjusted EBITDA as a % of GOV margin was up 40bp QoQ at 2.8% vs. our estimate of 2.7%.

* Instamart’s adjusted EBITDA as a % of GOV was -12.1% (-15.8% in 1Q) vs. our estimate of -13.8%.

* Consol. Adj. EBITDA came in at negative INR6.9b.

* Instamart reported a contribution margin of -2.6% (-4.6% in 1Q) vs. our estimate of -3.3%. This was aided by higher advertising, optimization of customer incentives, increased capacity utilization, and operating leverage.

* Swiggy reported a net loss of INR11b (est. INR11.2b), an increase of 75% YoY.

* Swiggy to consider a fundraise of INR100b through the QIP route.

Key highlights from the management commentary

* FD: General softness in discretionary consumption was offset by benign food and fuel inflation and supportive income-tax cuts, which aided spending.

* 10-minute delivery through Swiggy Bolt is now live across 700+ cities, contributing over 10% of total orders.

* The quarter witnessed heightened competitive intensity with lower subscription fees and reduced minimum order values. Swiggy responded by further subsidizing Swiggy One deliveries, balanced by a higher platform fee.

* Growth remains the overarching priority, even as the company continues to progress toward a steady-state margin of 5% of GOV.

* The resilient GOV performance was driven by a growing MTU base, enabled by better execution—particularly in Tier-2 cities—and improved consumer propositions, which also helped expand GOV per MTU.

* ‘Bolt’ now contributes over 10-12% of total orders. It has a minimal impact on AOV and is not dilutive at the platform level. Its economics are close to the platform average, despite no incremental monetization.

* Instamart: Its GOV stood at INR70.2b, up 107% YoY and ~15% QoQ. The company added 40 new dark stores during the quarter, half of which were megapods. It aims to meet or exceed industry growth.

* Sufficient capacity has been built in the dark-store network, capable of handling up to 2x the current business levels.

* AOV rose ~40% YoY to INR 697, led by expansion in non-grocery categories and higher-value basket behavior. Management sees further headroom for AOV expansion as penetration in non-grocery remains low.

* Non-grocery categories contributed 26.2% of GOV (vs. 8.7% YoY), driven by Electronics, Small Appliances, Home & Kitchen, and Toys — each doubling in share over the past two quarters. Pharmacy adoption has also grown faster than other segments.

* Swiggy would consider a fundraise of INR100b through the QIP route. This fundraise aims to bolster growth capital and strategic reserves.

* The company acknowledged that an eventual shift to a partial inventory-led model is possible. Domestic investor shareholding now stands at 43%.

Valuation and view

* We believe Swiggy is entering a phase of profitability, supported by operating discipline and improving network efficiency. The combination of steady FD growth, rising Instamart AOV, and easing fixed-cost drag enhances the visibility of positive unit economics.

* Steady improvements in AOV, dark store throughput, and take rates could lead to a material re-rating in profitability, prompting a more constructive stance on the stock.

* We value the FD business at 30x FY27E adjusted EBITDA and QC using DCF. We have brought forward our profitability assumptions for Instamart. We reiterate our BUY rating with a TP of INR550, implying a potential upside of 31%.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412