Buy PNB Housing Ltd for the Target Rs.1,260 by Motilal Oswal Financial Services Ltd

Disbursement momentum accelerates; retail loan growth healthy

NIM expands ~6bp QoQ; benign credit costs lead to big earnings beat

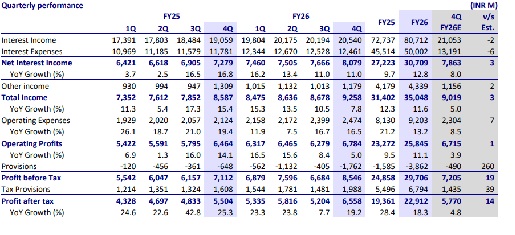

* PNB Housing’s (PNBHF) 4QFY26 PAT grew ~19% YoY to ~INR6.6b (14% beat). FY26 PAT grew 18% YoY to INR22.9b. 4Q NII rose ~11% YoY to ~INR8.1b (in line). Other income declined ~10% YoY to ~INR1.2b. Opex rose ~17% YoY to ~INR2.5b (~7% higher than MOFSLe).

* 4Q PPoP grew ~5% YoY to INR6.8b (in line) and FY26 PPoP grew ~11% YoY to INR25.8b. Credit costs (net of recoveries) resulted in a provision write-back of ~INR1.8b (vs. est. ~INR490m). This resulted in net credit costs of -83bp (PQ: -20bp and PY: -35bp).

* Loan growth for PNBHF is being led by the affordable and emerging market segments, which together are expected to form ~50% (currently ~40%) of the loan mix over the medium term. These segments continue to benefit from strong demand visibility, particularly in Tier-2 and 3 cities, where infrastructure development and economic activity remain supportive.

* Management guided for overall loan book growth of ~18-20%, primarily led by the retail segment. While corporate lending is anticipated to remain selective and limited in scale (not exceeding 3% in FY27 and 5-6% by FY28), it is expected to gradually stabilize and contribute in a calibrated manner, focused on high-quality developers in key urban markets. Digital and distribution enhancements, along with deeper partner engagement, are expected to further support scalable growth.

* Margins are expected to remain stable, supported by a shift toward higheryielding segments and continued improvement in funding costs. Yields have likely bottomed out following earlier rate-driven moderation and are expected to gradually improve with a higher share of affordable and emerging segment disbursements. Improvement in CoF, aided by stronger credit positioning and funding diversification, is expected to provide additional support to spreads.

* Asset quality trends remain stable, with delinquency indicators showing no fresh stress build-up despite geopolitical uncertainties. Credit costs are expected to remain contained, aided by sustained recoveries from writtenoff pools and improved portfolio seasoning.

* PNBHF reported a healthy quarter with improvement across key parameters. Disbursement growth saw an uptick, and margins expanded slightly as CoF declined, even though yields moderated. The BT-out rate also declined, aided by the unchanged repo rate environment. Asset quality remains robust, resulting in continued provision write-backs. Overall, 4QFY26 reflected steady progress with improving underlying operational metrics.

* We increase our EPS estimates for FY27/FY28 by 5%/4% to factor in higher other income, lower credit costs and slightly higher loan growth. We estimate PNBHF to deliver a CAGR of 19%/13% in loans/PAT over FY26-28E and RoA/RoE of ~2.4%/12.8% in FY28E. Reiterate BUY with a revised TP of INR1,260 (based on 1.4x FY28E BVPS).

Highlights from the management commentary

* PNBHF commenced corporate lending with wholesale disbursements at ~INR3.4b in 4QFY26, with a deliberate focus on quality developers and select geographies such as Mumbai, Pune, Hyderabad, Delhi, Chennai and Bangalore.

* About ~35 branches were added during the year, taking the total network to 393 branches. Affordable and emerging segments now account for ~80% of the branch network, reinforcing its strategic focus on high-growth geographies.

Valuation and view

* PNBHF is expected to sustain healthy loan growth going forward, supported by a strategic shift toward affordable and emerging segments, along with continued focus on disciplined margin management. The resumption of corporate segment is expected to provide incremental support to margins, although it will remain a relatively small part of the overall portfolio. Additionally, ongoing enhancements in digital capabilities and distribution are likely to further support efficient growth. Credit costs are expected to remain benign, with provision write-backs and recoveries likely to sustain in FY27 as well.

* The company’s operating trajectory reflects improving growth visibility and stable profitability drivers. PNBHF currently trades at 1.2x FY27E P/BV. We expect PNBHF to post a CAGR of 19%/13% in loans/PAT over FY26-28E and RoA/RoE of ~2.4%/12.8% in FY28E. Reiterate BUY with a revised TP of INR1,260 (based on 1.4x FY28E BVPS).

* Key risks: (a) limited NIM expansion in FY27 due to high competitive intensity in the mortgage segment; and (b) asset quality deterioration and elevated credit costs arising from seasoning in the affordable, emerging, and corporate portfolios.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412