Buy Petronet LNG Ltd for the Target Rs. 365 by Motilal Oswal Financial Services Ltd

Capacity tie-ups and volume recovery remain key catalysts

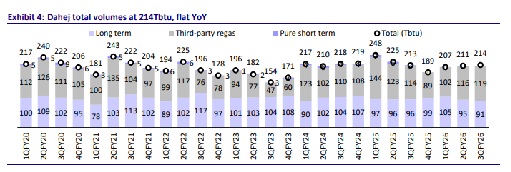

? PLNG’s 3QFY26 EBITDA (adjusted for labor codes impact of INR254m) came in 7% above estimate at INR12.2b (flat YoY). EBITDA adjusted for UoP provisioning and waiver stood 21% above our estimate. PAT adjusted for UoP provisioning, waiver, and labor code impact stood 25% above our estimate. Total volumes came 3% above our estimate at 233tbtu. Dahej utilization was also 3% above our estimates, while Kochi utilization stood in line with our estimates.

? Key things we liked about the result: 1) Capacity utilization remained robust at the Dahej LNG Terminal and Kochi LNG Terminal at 97% and 30%, respectively, with spot volumes witnessing a recovery to 4tbtu during the quarter. 2) Management has guided that it intends to maintain a healthy dividend payout of ~40% over the coming years, despite an increase in the capex. 3) Kochi-Mangalore-Bangalore PL is expected to be connected to the National Gas Grid by end-Jun’26. Lower LNG prices, along with enhanced pipeline connectivity, are likely to support higher terminal utilization at Kochi in FY27.

? Key investor concerns: 1) The company booked additional provisions of INR0.8b against UoP dues during the quarter. UoP trade receivables of INR0.8b were waived off during 3Q. UoP write-offs and waivers continue to weigh on PLNG's performance. 2) The 5 mmtpa capacity expansion at the Dahej LNG Terminal is now expected to be mechanically completed by endMar’26, and will take a few months to become operational (delayed vs. the previous timeline of becoming operational by end-Mar’26). Further, the absence of long-term contracts to cover a meaningful portion of the incremental capacity raises concerns over potential under-utilization.

? Key changes to earnings estimates: Considering the delay in commissioning of expanded capacity at Dahej and the recent softness in spot and service volumes, we lower our FY27/28 volume assumption for the Dahej terminal to 18/18.7mmtpa (from 18.3/18.9mmtpa earlier), leading to a 11%/8% reduction in our FY27/28 EBITDA estimate.

? Valuation and view: According to our DCF analysis (WACC: 10.5%), at CMP, PLNG is pricing in an unrealistic scenario of a 20% decline in tariffs at the Dahej and Kochi terminals in FY28, with no tariff hike thereafter and 0% terminal growth. At 10.3x FY27E P/E and a ~3.7% dividend yield, we believe valuations are inexpensive. We reiterate our BUY rating with a DCF-based TP of INR365.

Highlights from the management commentary

? Update on the Dahej petchem expansion: The mechanical completion is expected to be completed by Mar’26.

? Gopalpur terminal: Land has been acquired, and revised Environmental Clearance (EC) has been resubmitted. The company is expecting the clearance soon (no timeline shared). Major capex will start in FY28 (total capex INR60b)

? In 3Q, inventory gain stood at INR270m.

? CY22 UoP charges are expected to be paid by Mar’26.

Stable 3Q performance

? PLNG’s 3QFY26 revenue came in below our estimate by 11% at INR112b.

? EBITDA (adjusted for labor codes impact of INR254m) came in 7% above estimate at INR12.2b (flat YoY).

? The company booked additional provisions of INR0.8b against UoP dues during the quarter. UoP trade receivables of INR0.8b were waived off during 3Q. EBITDA adjusted for UoP provisioning and waiver stood 21% above our estimate.

? Adj. PAT was 10% above our estimate at INR8.7b (flat YoY).

? PAT adjusted for UoP provisioning, waiver, and labor code impact stood 25% above our estimate.

? Operational performance:

? Total volumes came 3% above our estimate at 233tbtu.

? Dahej utilization was also 3% above our estimates, while Kochi utilization stood in-line with our estimates.

? As of Dec'25, provisions on UoP dues stood at INR8.2b.

? UoP dues of INR13.1b (net of provision: INR5b) were included in trade receivables as of Dec'25. PLNG has obtained bank guarantees from some customers to recover UoP charges. While some customers have not given balance confirmations toward these dues, management is confident of recovering such charges.

? Spot LNG prices fell QoQ in 3Q, averaging USD10.9/mmbtu (USD11.8/mmbtu in 2Q).

Valuation and view

? As per our DCF analysis (WACC: 10.5%), at CMP, PLNG is pricing in an unrealistic scenario of a 20% decline in tariffs at the Dahej and Kochi terminals in FY28, with no tariff hike thereafter and 0% terminal growth. At 10.3x FY27E P/E and a ~3.7% dividend yield, we believe valuations are inexpensive.

? Our DCF-based TP of INR365 (WACC: 10.5%, TG = 2%) assumes a 10% tariff cut in FY28, followed by a 4% rise for both the terminals. While we have incorporated the full capex for the petchem plant, we value it conservatively at 0.5x FY29E P/B and discount this back to FY27.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

600-400.jpg)