Buy JK Cement Ltd for the Target Rs.6,040 by Motilal Oswal Financial Services Ltd

Volume momentum strong; cost headwinds ahead

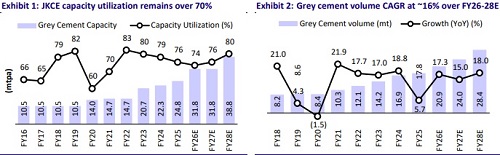

Healthy domestic demand intact; cost pressures rise, capex accelerates We interacted with management of JK Cement (JKCE) to understand current industry trends in terms of cement demand, costs and pricing, the company’s key initiatives towards cost saving and capacity expansion. JKCE management highlighted a healthy domestic demand trend in 4QFY26 led by broad based demand across key segments. The pricing environment remains mixed, with stronger traction in non - trade segment relative to trade. Input cost pressure remain elevated due to ~USD20/t rise in petcoke price, implying an incremental cost impact of INR75-80/t. Further, higher packaging cost will also lead to rise in overall opex/t in 1QFY27. However, ongoing cost - saving initiatives such as higher green power share and logistics optimization to partly offset those impact. It has outlined an aggressive capex - led expansion strategy, targeting capacity of > 50mtpa over the medium term, with a phased ramp-up to ~40mtpa by 1HFY28 and ~45mtpa by FY29, driven by key projects like Jaisalmer, Mudappur and Panna. Capex pegged at INR90b over FY26-28 across key projects, leading to increase in net debt to INR79b by FY28. The net-debt to EBITDA ratio likely to surge to 2.5x (vs. earlier target of 2.0x) by FY28. We cut our EBITDA estimates by ~8% for FY27/FY28 (each) mainly due to rising cost pressure. We value JKCE at 17x FY28E EV/EBITDA to arrive at our revised TP of INR6,040 (earlier 6,780). Reiterate BUY.

JKCE’s aggressive capacity build-out targets ~50mtpa by FY30-31

* JKCE is targeting ~50mtpa grinding capacity by FY30 - 31, which includes expansions in North, South and Central regions. Recently, it has completed a clinker/grinding capacity expansion of 0.5mtpa/1.0mtpa at its Mudappur, Karnataka plant with an estimated capex of INR1.3 - 1.5b. The company’s Panna unit clinker capacity is currently stood at 6.6mtpa, which is expected to be ramped up to 7.3mtpa in the six months, for which it has ~12.0mtpa grinding capacity operational across central and Bihar.

* It is increasing clinker backed grinding capacity to ~40.0mtpa by 1HFY28 with ongoing expansion in the north region. This includes 7.0mtpa greenfield griding capacity addition spread across Rajasthan and Punjab at a capex of INR45.0b over FY26 - 28 and ~1.0mtpa through debottlenecking in Mangrol, Rajasthan. Moreover, it is targeting to increase grinding capacity to ~45mtpa by FY29E, led by expansion at Mudappur, Karnataka. This will include a 3.3mtpa brownfield clinker capacity and 5.0mtpa grinding capacity at an estimated capex of INR30.0b over FY28 - 29E. It plans to cross 50mtpa of grinding capacity target by FY30-31 by adding 3rd clinker line at Panna.

* It has recently acquired a small grinding unit (capacity of 0.24mtpa) and 34 acres land in Andhra Pradesh, under asset purchase agreement at a consideration of INR288m, subject to certain conditions. The assets have been non-operational since Apr’25, and it may decide next course of action post transaction consummated.

* The next phase of expansion is likely to be focused on Chhattisgarh, Gujarat, and Odisha. It is looking for capacity growth beyond 50mtpa in long term and participating in limestone block auctions to establish presence in new markets.

Broad-based demand drives double-digit volume growth in 4QFY26

* The company is witnessing a healthy volume trajectory, with ~12 - 13% YoY growth, driven by broad-based demand across segments. While trade sales were temporarily impacted in the 3QFY26 due to the commissioning of the Panna plant, momentum has since revived, indicating a recovery in the Individual House Building (IHB) segment as well. Demand visibility remains strong and sustainable, led by Government - led demand continues to be robust, particularly towards the quarter - end, and infrastructure projects are witnessing steady execution. In the North region, clinker utilisation currently stands at ~85%, which could drop to ~75% as new capacities commissioned, aligning with utilisation levels seen in other regions.

* The pricing environment remains mixed, with stronger traction in the non-trade segment relative to trade. Trade prices have seen a modest increase of INR2- 3/bag across North and Central regions, while non-trade prices have improved more meaningfully by INR10 - 15/bag in Jan - Feb’26. Similar pricing trends are observed in key markets such as Karnataka and Maharashtra. On a blended basis, ~65% of volumes have seen realisation improvement of INR35 - 40/t, while the remaining ~35 - 40% has seen a sharper increase of INR150 - 200/t. However, price corrections in Mar’26 could moderate the overall benefit, leading to an estimated net realisation increase of ~INR50/t for 4QFY26.

* The company continues to benefit from government incentives, with ~INR2.6b expected in FY26 (vs. earlier ~INR3.0b), increasing to ~INR2.70-2.75b in FY27 and ~INR3.0b+ in FY28. Nimbahera incentives are nearing completion (2 years remaining), but this will be offset by new incentives from Jaisalmer. Additionally, auctioned mines are being utilized to support existing operations, ensuring raw material security and cost stability.

Fuel cost spike drive costs, key cost initiatives offset the impact partially

* On the cost front, input pressures persist, primarily led by a ~USD20/t increase in pet coke prices, translating to an incremental cost impact of ~INR75–80/t. However, it continues to focus on structural cost reduction initiatives. Increased adoption of green power (targeting ~5% incremental usage annually) has already delivered ~INR100/t savings, with an additional ~INR50/t savings potential. Logistics optimization remains another key lever, driven by higher direct dispatches (currently ~20%) and improved plant-market linkages. The commissioning of the Bihar grinding unit is expected to reduce lead distances and freight costs, especially in high-cost markets like Central and Bihar. It is also scaling up volumes in Bihar from 0.01mt/month to 0.02mt/month by FY27, supported by clinker supply from Panna.

* At J&K assets, the company is currently incurring investments to establish and scale the JK brand in this market. At efficient capacity utilization it has potential to produce 1.0-1.15mtpa, and of cost reduction of INR300-400/t.

* The Jaisalmer unit is expected to be a key cost leader, supported by multiple structural advantages. It will cater to markets such as Bikaner, Bathinda, and Gujarat, either through clinker transfers or direct sales. The plant is expected to operate with ~80 - 90% green power usage, supplemented by low-cost lignite fuel (~INR 1/GCV vs. INR 1.3 - 1.4/GCV for alternatives), leading to 40 - 50% fuel cost savings. Additionally, access to high-grade limestone (without sweeteners),efficient rail logistics, and superior incentives (first-mover advantage) further strengthen cost competitiveness. The company is currently investing in brandbuilding in these newer markets to support long-term scale - up.

* The Fujairah operations are currently witnessing disruption as exports is closed. The last clinker consignment of ~50k tonne sent to Australia in Feb’26. Its sales predominantly to GCC markets, currently.

View and valuation

* We estimate JKCE’s consolidated revenue/EBITDA/PAT CAGR at 15%/15%/13% over FY26 - 28. We anticipate the company’s consolidated volumes to post ~15% CAGR over FY26-28, and OPM at ~17% by FY28 (similar to FY26). We estimate its EBITDA/t at INR992/ INR1,007 in FY27/FY28 vs. INR1,015 in FY26E.

* We estimate JKCE to generate a cumulative OCF of INR72.7b during FY26-28, with cumulative capex estimated at INR90.0b (considering Karnataka expansion to begin in FY28) over the same period. Given the heavy capex cycle, its net debt is estimated to surge to INR79b by FY28E vs. INR54b in FY26E. The company’s net debt to EBITDA ratio is estimated to increase upto 2.5x by FY28 vs. 2.3x by FY26E. We anticipate its RoE/RoCE (post tax) to be stable at ~15%/10% by FY28 given the higher capex funded by debt, and flat margins.

* We cut our EBITDA estimates by ~8% for FY27/FY28 (each) mainly due to rising cost pressure. It is currently trading at 17x/15x FY27/FY28E EV/EBITDA. We value JKCE at 17x FY28E EV/EBITDA to arrive at our revised TP of INR6,040 (earlier 6,780). We maintain our BUY rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041