Add The Leela Ltd for Target Rs. 490 by Choice Institutional Equities

Domestic Bookings and ARR Improvement Softens Conflict Impact

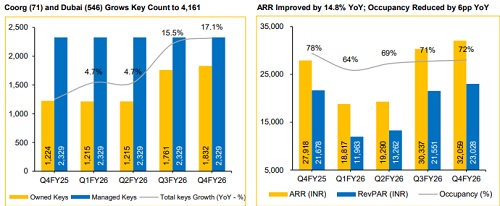

THELEELA’s occupancy for Q4FY26 dropped by 6pp to 71.8%, whereas ARR improved by 14.8%. This resulted in a RevPAR of INR 23,028 for the quarter (+ 6.2%). We project occupancy to remain subdued in Q1FY27E, the impact of which will be softened owing to a surge in domestic visitors and a cyclically muted quarter. Usually, 50% of visitors of THELEELA are FTAs, who stay for longer duration as compared to domestic tourists.

View and Valuation

We reduce our revenue estimate for FY27E and FY28E by 2.7% and 5.3% respectively, on the back of delays in execution of three assets. Consequently, we also revise our EBITDA estimate lower by 1.6% and 3.9%, respectively, for FY27E and FY28E. We value the company at 18.0x EV/Adj. EBITDA on FY28E, arriving at a Target Price of INR 490 (vs. 510). Our DCF valuation of INR 500/share provides a sanity check. We, therefore, downgrade our rating to “ADD”, given an upside of 16.7%.

Key Risk to Our Valuation

Possibly prolonged conflict risks a 10–15% decline in inbound guests for FY27E. Capital cost inflation may cause cost overruns. Execution delays could postpone revenue recognition.

EBITDA Margin Improves by 160 bps for FY26

* RevPAR for FY26 came in at INR 17,460 (+14% YoY), driven by a strong ARR growth of 12.6%

* Revenue came in at INR 4.8 Bn for Q4FY26, an improvement of 14% YoY. Revenue for FY26 grew by 17.4% to INR 15.27 Bn ? EBIDTA stood at INR 2.6 Bn, an increase of 17.3% YoY. EBITDA margin for the full year FY26 improved by 160 bps to 48.6%

* PAT came in at INR 1.7 Bn, rising by 46.3% YoY. PAT margin for FY26 stands at 26.4%

* ROE and ROCE for FY26 stood at 8.1% and 8.2%, respectively, vs ROCE of 10.2% in FY25

Revenue Visibility from ARQ Club, Stabilisation and New Keys

Revenue visibility is supported by incremental contribution from ARQ membership-led clubs (INR 4.5 Mn per membership) with further optionality of run-rate-based membership cost. ARQ is an invite-only exclusive club, currently operational in Bengaluru, with further additions planned in Mumbai, Chennai, and Delhi. The company is targeting 2,000+ members over the longterm. FY26 saw a 50% boost in key count supported by Dubai (546 keys) and Coorg (71 keys) acquisitions. The Dubai property is expected to be consolidated from FY28E, while Coorg is already operational. Additionally, a pipeline of 1,008 keys provides medium-term growth visibility.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131